Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

How Much Mortgage Can I Afford? Your 2026 Ontario Affordability Guide

- Home

- How Much Mortgage Can I Afford? Your 2026 Ontario Affordability Guide

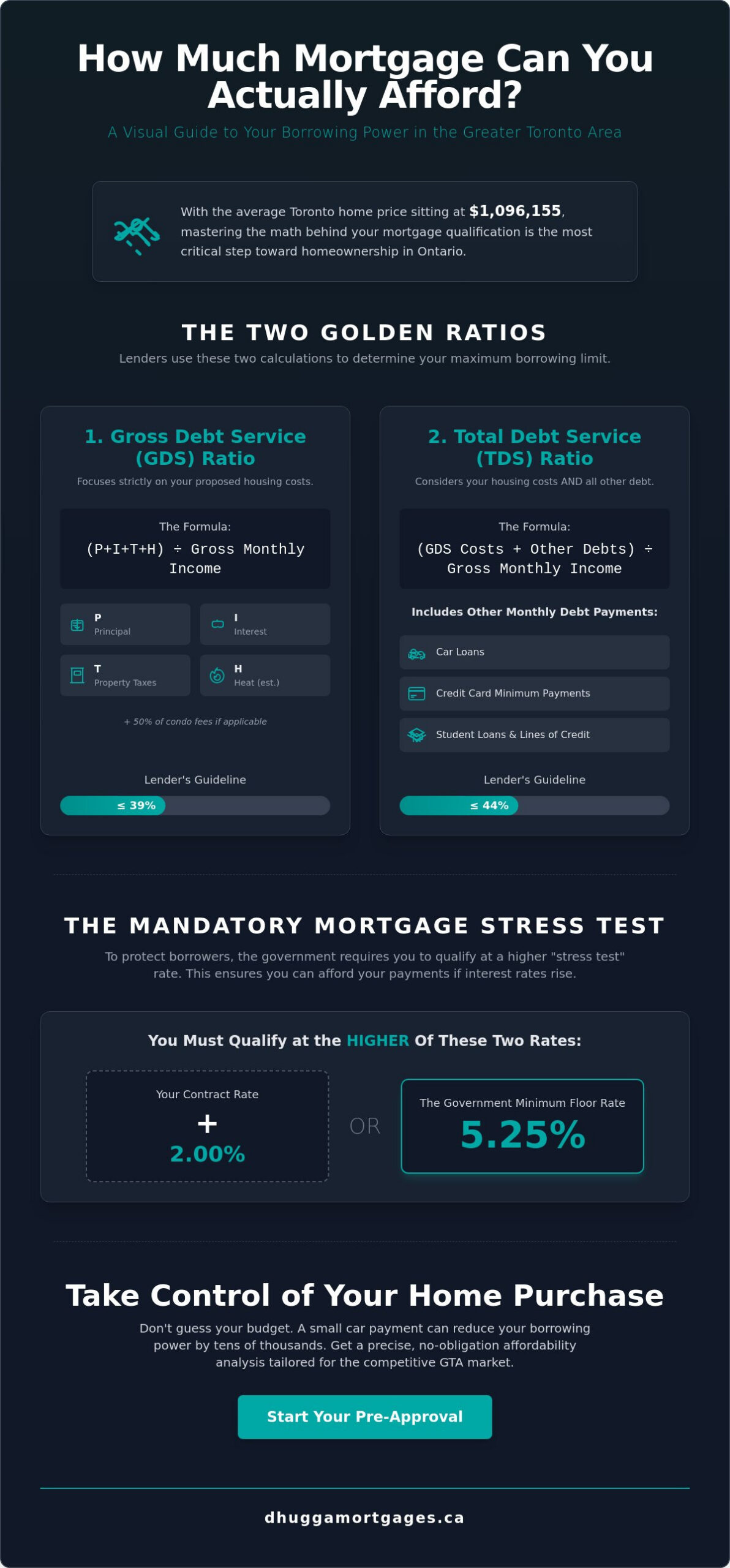

Your borrowing power is a variable you can control, not a fixed limit set by the bank. In a market where the average Toronto home price sits at $1,096,155, asking how much mortgage can I afford is the most critical step toward homeownership. You’ve likely felt the pressure of rising living costs in Brampton or felt intimidated by the complexity of the mortgage stress test. It’s a common fear, but you don’t have to guess your way through the competitive GTA housing market.

Master the math behind your qualification today. We’ll show you exactly how lenders use GDS and TDS ratios to set your limit and how the current 5.30% stress test floor impacts your bottom line. This guide provides a clear dollar figure for your budget and actionable ways to boost your borrowing power immediately. Stop worrying about the “what ifs” and start your house hunt with total confidence. Get the facts, secure your edge, and realize your goal of owning a home in Ontario.

Key Takeaways

- Learn the exact math lenders use to determine how much mortgage can I afford in today’s market.

- Identify the difference between a bank’s maximum loan limit and a monthly payment that actually fits your lifestyle.

- Uncover strategic ways to boost your borrowing power through proactive debt management and credit score optimization.

- Navigate the 2026 Ontario market with confidence by understanding how down payments and stress tests impact your budget.

- Gain a competitive edge in the GTA by accessing multiple lending options that go beyond what a single bank can offer.

Understanding Mortgage Affordability in Ontario’s 2026 Market

Affordability is a personal calculation. It isn’t just a number generated by a generic algorithm at a big bank. While a lender looks at your gross income, true affordability balances those limits against your daily reality. In June 2026, with the Bank of Canada policy rate sitting at 2.25%, borrowing power has stabilized. However, high living costs in the GTA mean you need a sharper strategy than a simple online calculator provides. Asking how much mortgage can I afford requires looking at your debt-to-income ratio through two different lenses: what you can borrow and what you should spend.

A pre-qualification is a surface-level glance at your finances. It’s a quick “yes” based on basic numbers. A deep affordability analysis is different. It’s a proactive deep dive that ensures you aren’t house-poor. We look at the current prime rate of 4.45% and stress-test your specific scenario at 5.30%. This ensures you can handle your payments even if the market shifts. You want a home that is an asset, not a financial burden.

The Difference Between Affordability and Qualification

Qualification is the maximum ceiling. It’s the absolute limit a lender allows based on strict mathematical formulas. Affordability includes the “colour” of your life. It includes your travel plans, RRSP contributions, and weekend hobbies. A bank won’t ask if you want to fly to Europe every summer, but your budget should. We recommend a safety buffer. Don’t push your debt service ratios to the absolute limit. Leave room for property tax adjustments or unexpected repairs. Knowing how much mortgage can I afford means knowing you can still enjoy your life after the papers are signed.

Why Local GTA Market Trends Matter

Location dictates your carrying costs. Property taxes in Brampton are higher than in Toronto. A $900,000 mortgage in Peel Region feels heavier than the same loan in Old Toronto because of that tax bill. If you’re eyeing a Mississauga high-rise, condo fees are a massive factor. These fees act as a “phantom mortgage” that eats into your monthly capacity. For those starting out, our first time home buyer mortgage Ontario guide offers deeper local insights to help you plan. Consider these variables before you start your search:

- Municipal Property Tax: Toronto vs. Brampton rates.

- Monthly Maintenance: Condo fees can add hundreds to your carrying costs.

- Utility Estimates: Older homes often cost more to heat and cool.

- Closing Costs: Budget 2% to 4% for land transfer taxes and legal fees.

The Golden Ratios: Calculating Your GDS and TDS

Lenders don’t look at your bank balance to decide your limit. They look at your ratios. To answer how much mortgage can I afford, you must understand the mathematical boundaries set by Canadian financial institutions. These formulas determine your risk level and your maximum loan amount. Lenders use your gross income—your total earnings before taxes are deducted—to run these numbers. While this makes your borrowing power look higher on paper than your actual take-home pay, it’s the standard for all Canadian mortgage qualification rules. You must also pass the stress test, which is calculated using the higher of your contract rate plus 2% or 5.25%.

Gross Debt Service (GDS) Explained

Your GDS ratio focuses strictly on your housing costs. Lenders use the acronym P.I.T.H., which stands for Principal, Interest, Taxes, and Heat. If you’re buying a condo, they also include 50% of the monthly maintenance fees. Most lenders cap this ratio between 32% and 39% of your gross monthly income. To estimate your numbers, look at recent property tax listings in your target GTA neighbourhood. For heating, a standard estimate of $100 to $150 per month is often used for single-family homes. Keeping this ratio lean gives you a better chance of securing a competitive rate.

Total Debt Service (TDS) and Other Obligations

The TDS ratio is the true deal-breaker. It includes your P.I.T.H. costs plus every other monthly debt obligation you carry. This means car loans, credit card minimum payments, and student lines of credit are all factored in. Even a modest $400 monthly car payment can slash your total mortgage capacity by tens of thousands of dollars. Lenders generally want to see a TDS ratio below 44%. If your debts are high, it’s vital to prioritize mortgage pre-approval for first time buyer status by clearing small balances first. This “polishing” of your debt profile directly increases the “how much” in your affordability equation.

Managing these ratios is the fastest way to gain an edge in a high-priced market. If you’re unsure how your current debts impact your numbers, let’s review your statement together to find hidden borrowing power. Knowing your exact GDS and TDS allows you to shop with certainty rather than hope. It’s the difference between a rejected application and a firm “yes” on your dream home. Start tracking these numbers today to realize your full potential as an Ontario homebuyer.

Factors That Shift Your Borrowing Power in the GTA

Income is your foundation. However, several external factors can drastically shift the final answer to how much mortgage can I afford in a competitive market like Toronto or Brampton. Your borrowing power is a moving target. It reacts to your down payment size, your credit history, and even your employment structure. Understanding these shifts allows you to optimize your profile before you ever step into an open house. You want to walk into a deal knowing your maximum limit is based on a strategic advantage, not just a guess.

The Down Payment Leverage

Your down payment does more than just reduce your loan amount. It changes the entire structure of your mortgage. If you put down less than 20%, you must pay for mortgage default insurance. These CMHC premiums are added to your total loan balance. This increases your monthly carrying costs and slightly reduces your maximum purchase price. Crossing that 20% threshold removes this cost and often unlocks longer amortization periods. This can lower your monthly payments and increase your overall budget. Use our first time home buyer checklist Ontario to track your savings progress and see how every extra dollar impacts your leverage.

Credit scores also play a massive role in 2026. A top-tier score doesn’t just get you a “yes.” It gets you the lowest possible interest rate. In a high-price neighbourhood, a difference of even 0.5% in your rate can translate to thousands of dollars in extra borrowing power. High scores signal reliability to lenders. This often leads to more flexible debt-to-income limits. If your score is lagging, focus on polishing it for six months. The payoff in your mortgage limit will be worth the wait. It’s about building a profile that lenders can’t ignore.

Self-Employed and Alternative Income

Business owners in Mississauga and Brampton often face a “paperwork gap.” Traditional banks look at your net income after tax deductions. This often hides your true ability to pay. We specialize in realizing the actual strength of your business. We use bank statement programs to show lenders what you really earn. This is a game-changer for entrepreneurs who want to maximize their budget without being penalized for smart tax planning. Our self-employed mortgage Canada solutions are designed to give you the same edge as a salaried employee. Similarly, “New to Canada” programs allow recent immigrants to use alternative credit history to secure a home faster. Your path to homeownership shouldn’t be blocked just because your income doesn’t fit a standard box.

Strategic Steps to Boost Your Mortgage Qualification

Your current financial snapshot is not a permanent limit. If you aren’t satisfied with the answer to how much mortgage can I afford, you can change the math. Borrowing power is dynamic. Small, intentional moves in the months leading up to your application can add tens of thousands of dollars to your budget. Start by polishing your credit profile at least six months before you plan to buy. This window allows you to correct errors, lower utilization, and prove a consistent history of reliability to A-lenders. It’s about presenting the strongest possible version of your finances to the bank.

Family support is another powerful lever in the Ontario market. A “Gift Letter” allows parents or relatives to provide down payment assistance. This isn’t a loan; it’s a non-repayable gift that immediately lowers your required mortgage amount and improves your ratios. Combining this with a strategy to consolidate high-interest debt into a single, lower payment can dramatically shift your qualification ceiling. Every dollar you save on monthly interest is a dollar that can be redirected toward your mortgage capacity. You need every advantage to compete in the GTA.

Reducing Your TDS Ratio Fast

Target high-impact debts first. Focus on loans with small balances but high monthly payments, like furniture financing or a short-term car loan. Paying these off clears up significant room in your Total Debt Service (TDS) ratio. Be careful with closing old credit lines. While it feels proactive, it can sometimes shorten your credit history and hurt your score. For those who already own property and want to move up, a debt consolidation mortgage Canada strategy can streamline your finances before you re-enter the market. It’s a tactical move to maximize your next purchase.

Income Optimization Strategies

Adding a co-signer is the fastest way to elevate your borrowing ceiling. A parent with strong income and low debt can bridge the gap between what you have and what you need for a GTA home. Beyond co-signers, ensure you document every secondary income source. This includes consistent part-time work, annual bonuses, and even potential rental income if the property has a legal basement suite. A-lenders typically require a stable two-year employment history to count these figures. Proving this stability gives you the edge needed to secure a larger loan. Book a strategy session today to build your custom qualification plan and stop leaving your budget to chance.

Navigating the Path to Homeownership with Dhugga Mortgages

Determining how much mortgage can I afford is a strategic exercise. It requires more than a basic online tool or a generic bank calculator. You need a partner who understands the high-stakes Ontario landscape. Dhugga Mortgages acts as your proactive guide. We remove the complexity of the 2026 market. We don’t just give you a number; we provide a clear path to the keys of your new home. Our process is built for speed and reliability. We value your time and ensure that every interaction moves you closer to your goal. Realize your homeownership dreams with a team that prioritizes your budget and your peace of mind.

Don’t limit your options by walking into a single bank branch. A bank only sells its own products. We provide the “Broker Advantage” by connecting you to dozens of institutional and alternative lenders. This competition works in your favour. It ensures you secure the most competitive rates and terms available today. Whether you are in Brampton, Mississauga, or Toronto, we tailor our search to your specific financial profile. We negotiate on your behalf. We handle the heavy lifting so you can focus on finding the right property. We find the edge that helps you win in a competitive market.

Why a GTA Expert Makes the Difference

Local expertise is non-negotiable in a market where property values shift by the block. We understand the nuances of land transfer taxes and municipal closing costs that vary between Peel Region and the City of Toronto. If your situation is non-traditional, we have access to private mortgage lenders Ontario that can offer solutions when traditional banks hesitate. We prioritize finding the strategic benefit that others miss. Our commitment is to your success in the 2026 market. We know the Brampton and Toronto neighbourhoods inside out. This local familiarity ensures your application is positioned correctly from day one.

Your Next Steps to a Successful Purchase

Confidence starts with a professional affordability assessment. Stop guessing and start planning. Your next steps are clear and actionable. First, gather your recent Notices of Assessment (NOAs), pay stubs, and bank statements. These documents are the fuel for your application. Second, reach out for a comprehensive review of your GDS and TDS ratios. Third, book your consultation to secure a 2026 rate hold. This protects you from market fluctuations for up to 120 days while you shop. Take control of your homebuying journey today. Realize your potential with a team that delivers results quickly and secures your financial future.

Secure Your Future in the Ontario Market

You now have the tools to master the math behind your qualification. Affordability is about more than a bank’s limit; it’s about your lifestyle and strategic planning. We’ve covered the critical GDS and TDS ratios, the impact of the 5.30% stress test, and how to proactively boost your borrowing power through debt management. Knowing exactly how much mortgage can I afford gives you the edge to act fast when the right GTA home appears. Stop guessing and start shopping with total certainty.

As a trusted brokerage partner of Mortgage Alliance, we specialize in Brampton and GTA residential lending. Our team brings deep expertise to self-employed and newcomer mortgage programs. We remove the complexity of the financial process so you can focus on the house hunt. We are your proactive partner in a competitive landscape. Every interaction is designed to get you results quickly and reliably.

Book Your Strategic Mortgage Consultation with Dhugga Mortgages Today. Let’s lock in your 2026 rate hold and turn your budget into a successful purchase. Your new home is within reach; let’s secure it together.

Frequently Asked Questions

What is the mortgage stress test in Canada for 2026?

The stress test requires you to qualify at the higher of 5.25% or your contract rate plus 2%. As of June 15, 2026, the lowest stress test rate for most insured borrowers is 5.30%. This mandatory calculation ensures you can maintain your monthly payments if interest rates rise in the future. It applies to all federally regulated lenders and directly impacts your maximum loan amount.

Can I afford a house in Toronto on a $100,000 salary?

Buying a detached home on a single $100,000 salary is difficult given the June 2026 average Toronto price of $1,096,155. Typically, this income qualifies you for a mortgage between $400,000 and $450,000 depending on your debt levels. You would need a significant down payment or a co-signer to bridge the gap for a house. Condos or properties in the broader GTA may offer more accessible entry points.

How much of my income should go toward my mortgage payment?

Lenders follow the Gross Debt Service (GDS) ratio, which caps your housing costs at 39% of your pre-tax income. This figure includes your principal, interest, property taxes, and heating costs. To maintain a comfortable lifestyle, many financial experts suggest keeping this closer to 30%. Understanding these ratios is the first step when asking how much mortgage can I afford in Ontario’s competitive market.

Does my car loan affect how much mortgage I can afford?

Yes, your car loan has a major impact on your borrowing power. Lenders include the monthly payment in your Total Debt Service (TDS) ratio, which usually cannot exceed 44%. A $500 monthly car payment can slash your total mortgage capacity by nearly $100,000. Paying off or reducing vehicle debt is often the fastest way to increase your home buying budget.

What are the closing costs I should budget for in Ontario?

You should budget between 2% and 4% of the purchase price for closing costs. This includes provincial land transfer tax, legal fees, and title insurance. If you are buying in Toronto, you must also pay a municipal land transfer tax. First-time buyers in Ontario can receive a rebate of up to $4,000 provincially to help offset these immediate expenses.

Can I still get a mortgage if I am self-employed with low reported income?

Yes, you can qualify using alternative programs that look at your gross business revenue rather than just your net tax returns. We use your bank statements to prove your actual cash flow and ability to pay. This is a common solution for GTA business owners who use legal deductions to reduce their taxable income but still have strong earnings. How much mortgage can I afford becomes a much higher number when we use your true business income.

Is it better to have a larger down payment or pay off debt first?

Paying off high-interest debt usually boosts your qualification more than a slightly larger down payment. Eliminating a $400 monthly credit card or loan payment clears more room in your TDS ratio than adding $10,000 to your down payment. However, reaching a 20% down payment is ideal because it eliminates the need for costly mortgage default insurance. We can analyze your specific debts to find the most efficient path.

How do interest rate changes in 2026 affect my borrowing power?

Interest rates and borrowing power have an inverse relationship. When rates rise by 1%, your maximum mortgage amount typically drops by about 10%. With the Bank of Canada policy rate holding at 2.25% in June 2026, the market has seen increased stability. This allows you to plan your budget with more confidence than in previous years of rapid rate hikes.