Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

First Time Home Buyer Mortgage Ontario: The Complete 2026 Strategic Guide

- Home

- First Time Home Buyer Mortgage Ontario: The Complete 2026 Strategic Guide

Buying your first home in Ontario is no longer about just saving; it’s about stacking. In 2026, the secret to a successful first time home buyer mortgage Ontario isn’t just a high credit score. It’s the strategic combination of new 30-year amortizations, expanded HST rebates, and the maximum C$60,000 RRSP withdrawal. You need a tactical edge to win in the GTA bidding wars. High down payment requirements and interest rate shifts make the process feel like a moving target. It’s stressful. It’s complex. We understand the frustration of watching prices climb while you try to realize your dream of ownership.

This guide ensures you master the 2026 landscape with expert insights on every incentive and the fastest path to homeownership. You’ll learn how to secure a low interest rate while maximizing every provincial and federal tax rebate available today. We’ll break down the new GST rules for homes up to C$1 million, the C$8,000 annual FHSA limit, and the 15-year HBP repayment plan. You’re about to get the full 2026 roadmap for a clear, stress-free closing. Let’s get you moved in.

Key Takeaways

- Navigate 2026 GDS/TDS ratios to qualify for high-value GTA properties with total confidence.

- Stack the C$60,000 RRSP withdrawal with the FHSA to build a powerful, tax-free down payment quickly.

- Claim up to C$4,000 in provincial rebates by optimizing your first time home buyer mortgage Ontario application.

- Lock in your interest rate for 120 days and follow a proven, step-by-step path to a stress-free closing.

- Access over 50 lenders and specialized programs for self-employed or newcomers to outperform standard bank offers.

Understanding the 2026 Ontario First Time Home Buyer Landscape

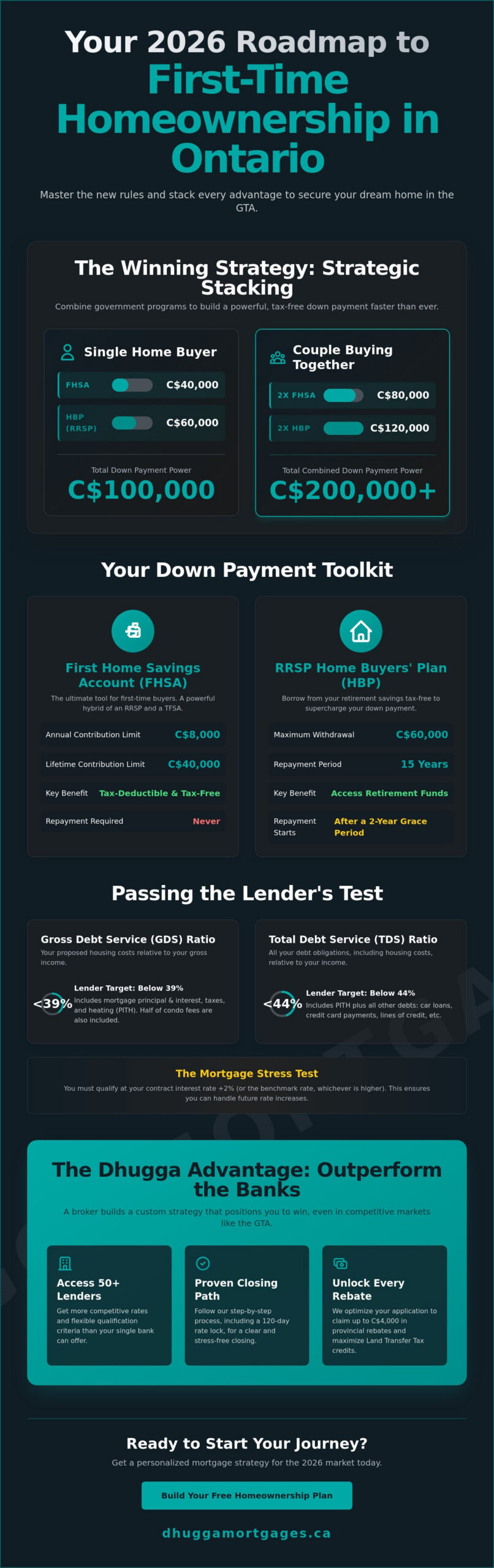

Securing a first time home buyer mortgage Ontario starts with knowing exactly where you stand. In 2026, the definition of a first-time buyer is twofold. Federally, you’re a first-time buyer if you haven’t lived in a home you or your partner owned in the last four years. However, for Ontario land transfer tax rebates, the rule is stricter; you must have never owned a home anywhere in the world. This distinction is vital when calculating your closing costs. You also need to clear the GDS and TDS hurdles. Lenders look for a Gross Debt Service ratio under 39% and a Total Debt Service ratio under 44%. With Brampton salaries facing GTA price tags, these numbers require precision planning. We provide the speed and local reliability to make these calculations work for you immediately.

The 2026 market is defined by a persistent supply lag. Competition remains high across the Greater Toronto Area. You aren’t just fighting other buyers; you’re fighting time and inventory shortages. The Dhugga Advantage means having a proactive partner who moves as fast as the market. We don’t just find a rate; we build a strategy that positions you as a serious buyer the moment you walk into an open house. Our team understands the local nuances of the Brampton and Mississauga markets, ensuring your application is robust enough to win in a competitive bidding environment.

The Reality of the Mortgage Stress Test in 2026

Qualifying isn’t just about your contract rate. The mortgage stress test requires you to prove you can handle payments at your contract rate plus 2%, or the benchmark rate, whichever is higher. This protects your equity if rates climb later. The Canada Mortgage and Housing Corporation (CMHC) uses these standards to ensure long-term stability in the Canadian housing market. A broker helps you navigate these strict bank requirements by accessing a wider range of lenders. If your ratios are tight, we can explore alternative lenders who offer more flexibility than the major banks.

Setting Realistic Goals in Brampton, Mississauga, and Toronto

Don’t start with listings. Start with your numbers. A detached home in Brampton has different down payment requirements than a condo in Mississauga or a townhouse in Toronto. For homes priced at C$1.5 million or more, you’ll need a full 20% down payment. For anything under that, you can leverage the 30-year amortization rules for insured mortgages that were expanded in late 2024. Realize your budget before you browse. A mortgage-first approach prevents the heartbreak of falling for a home you can’t carry. We help you set realistic targets based on your specific financial profile and the current 2026 market conditions.

Maximizing Your Down Payment: FHSA and RRSP Strategies

Building a first time home buyer mortgage Ontario strategy requires more than a simple savings account. You need to stack government programs to reach the minimum down payment for a GTA home. In 2026, the combination of the First Home Savings Account (FHSA) and the RRSP Home Buyers’ Plan (HBP) creates a massive advantage. These aren’t just places to store cash; they’re tax-efficient engines designed to accelerate your purchase timeline. The Financial Consumer Agency of Canada offers general guidance on these tools, but winning in a market like Brampton or Toronto requires a tactical approach to every dollar.

Couples buying together have a unique opportunity to double their impact. By stacking their contributions, a pair of buyers can leverage over C$200,000 in combined savings. This includes C$40,000 each in lifetime FHSA contributions plus C$60,000 each from their RRSPs. This level of capital can turn a high-ratio mortgage into a conventional one, potentially saving you thousands in insurance premiums. If you’re short on personal savings, gifted down payments remain a staple of the Ontario market. Lenders accept funds from immediate family members, provided you have a signed gift letter and proof of the wire transfer. It’s a fast, reliable way to boost your deposit without taking on additional debt.

The FHSA Advantage: Why It Is a Game-Changer

The FHSA is the primary 2026 savings tool for any serious buyer. Contributions are tax-deductible, which lowers your taxable income and puts more money back in your pocket during tax season. Unlike the HBP, you never have to pay this money back to the account. It’s tax-free going in and tax-free coming out, provided the funds go toward your first home. High earners should prioritize this account first to maximize their annual C$8,000 contribution limit.

Using the RRSP Home Buyers’ Plan Effectively

The HBP withdrawal limit is now C$60,000 per person. You have 15 years to repay the funds to your RRSP, with a two-year grace period after the withdrawal. Remember the 90-day rule; your funds must be in the RRSP for at least three months before you pull them out for a down payment. Combining the HBP with your FHSA is the fastest way to build a robust initial deposit. To see how these accounts impact your specific qualifying power, you can calculate your total down payment potential with our team today.

Speed is essential when managing these accounts. Moving money between institutions can take days or weeks. Ensure your funds are liquid and ready for withdrawal before you start making offers. A proactive approach to your savings ensures that when the right first time home buyer mortgage Ontario opportunity appears, you have the capital ready to move immediately. Don’t let administrative delays cost you a home. Plan your withdrawals now to ensure a smooth closing later.

Calculating Closing Costs and Land Transfer Tax Rebates

Closing costs often catch buyers off guard. You’ve saved your down payment, but the final bill includes more than just the purchase price. In Ontario, the largest hurdle is the Land Transfer Tax (LTT). This tax is calculated on a sliding scale based on your home’s value. However, as a first-time buyer, you have a significant advantage. The Ontario Land Transfer Tax Rebate can reduce your provincial tax burden by up to C$4,000. To qualify for your first time home buyer mortgage Ontario, you must be at least 18 years old and intend to occupy the home as your principal residence within nine months of closing. We ensure these rebates are factored into your initial budget so there are no surprises on closing day.

Don’t forget the “hidden” costs that banks often overlook. These are essential for a stress-free transition. Budget for these items immediately:

- Legal Fees: Typically C$1,500 to C$2,500 for title searches and registration.

- Title Insurance: Protects you against property ownership disputes.

- Appraisal Fees: Usually C$300 to C$500 to verify the home’s value for the lender.

- Home Inspection: A critical step to identify potential structural issues.

Aim to set aside 1.5% to 4% of your purchase price for these expenses. Having this cash ready prevents last-minute scrambles for high-interest loans.

Ontario vs. Toronto: The Rebate Difference

Location dictates your tax bill. On a C$800,000 home in Brampton, you only pay the provincial LTT. In Toronto, you face the “Double Tax” due to the Municipal Land Transfer Tax. For that same C$800,000 Toronto property, your total tax bill would be nearly double. Fortunately, Toronto offers an additional rebate of up to C$4,475 for first-time buyers. Combined with the provincial C$4,000, your total savings can reach C$8,475. We help you compare these costs across the GTA to find the most efficient path to ownership.

GST/HST New Housing Rebates

New construction offers unique savings in 2026. Under Bill C-4, the federal government removed the 5% GST on new homes valued up to C$1 million. Additionally, the temporary Ontario HST rebate removes the full 13% HST on eligible new builds until March 31, 2027. On a C$1 million new build, these combined rebates represent massive savings. This shift makes new construction a strategic choice for many first-time buyers. We track these legislative updates to ensure you maximize every available dollar. Speed matters here; these temporary rebates have strict windows for eligibility.

The Step-by-Step Path to Your First Mortgage

Speed is your currency in the Ontario market. You need a process that cuts through the noise and eliminates friction. Securing a first time home buyer mortgage Ontario requires a methodical approach that starts long before you visit a property. We’ve refined this path to ensure you move with maximum confidence and zero delays. The 2026 market doesn’t wait for paperwork; you must be ready to act the moment a listing hits the wire.

The journey follows five critical milestones:

- Step 1: The Pre-Approval. We lock in your interest rate for 120 days. This protects you from market volatility while you shop.

- Step 2: Document Collection. Gather your pay stubs, NOAs, and down payment history immediately. Total transparency with your lender is the only way to ensure a fast approval.

- Step 3: The Search. Align your pre-approved budget with the reality of the GTA market. Focus on properties where your 39%/44% ratios remain healthy.

- Step 4: The Offer. Work with your realtor to include a financing condition. Even with a pre-approval, the lender must approve the specific property you’ve chosen.

- Step 5: Closing. Your broker and lawyer coordinate to fund the deal. This is where your land transfer tax rebates are applied to the final statement of adjustments.

Why Pre-Approval Is Non-Negotiable in 2026

Pre-qualification is just a conversation; a full pre-approval is a commitment. It involves a deep dive into your credit score and income to determine exactly what a lender will provide. In a high-velocity market, sellers often ignore offers that don’t have a solid pre-approval attached. This document protects you from mid-search rate hikes and gives you the “green light” to bid aggressively. Get your mortgage pre-approval started today to establish your maximum purchase price.

Documentation: The “Dhugga Speed” Checklist

Lenders require a clear paper trail to satisfy Anti-Money Laundering (AML) rules. You must provide a 90-day history for all down payment funds, whether they are in an FHSA, RRSP, or a standard savings account. If you’re a salaried employee, have your most recent letter of employment and two pay stubs ready. Self-employed buyers need two years of T1 Generals and the corresponding Notice of Assessment (NOA) from the CRA. The NOA is the single most important document for verifying your income stability. Organizing these files now ensures your first time home buyer mortgage Ontario application moves through the system at high velocity.

The Dhugga Advantage: Why a GTA Broker Beats the Bank

A single bank offers a single product shelf. We offer a marketplace. When you’re seeking a first time home buyer mortgage Ontario, limiting yourself to one institution is a strategic error. We provide access to over 50 lenders, including major banks, credit unions, and trust companies. This scale creates immediate competition. We make lenders fight for your business. You get the edge. This tactical negotiation ensures you aren’t just taking the first rate offered, but the best one available in the 2026 market. We prioritize your time and your bottom line.

Our deep roots in Brampton, Mississauga, and Caledon provide a level of local expertise a national call centre cannot match. We know the neighbourhoods. We understand the property values. We move with the speed the GTA market demands. Reliability matters when your dream home is on the line. We act as your proactive partner, managing every detail from the initial application to the final funding. It’s about removing complexity and delivering results quickly. You need an expert who knows the local landscape and has the authority to deliver.

Tailored Solutions for Complex Profiles

Standard bank criteria often fail modern buyers. We specialize in Self-Employed Mortgages for entrepreneurs who lack traditional income proof. If you’re an independent contractor in Brampton, we know how to present your T1 Generals to secure an approval. We also offer New to Canada Mortgages for those with limited domestic credit history. Even if your profile requires a “B” lender, we have the connections to realize your homeownership goals. Our focus is on finding a path forward where others see a dead end. We solve the problems that stop other lenders.

Efficiency and Results: Your Proactive Partner

Time is your most valuable asset. Our communication style is direct and results-oriented. We don’t waste hours on fluff. We provide high-impact statements and clear instructions. You get peace of mind through a streamlined process that prioritizes your timeline. This is neighbourly expertise backed by professional authority. We are high-energy facilitators who take charge of the process from day one. You need a guide who values speed as much as you do. We remove the friction from the mortgage process.

Don’t settle for a generic bank experience. Secure your first time home buyer mortgage Ontario with a team that understands the local advantage. Reach out today for a high-velocity mortgage experience. Let’s get you approved and into your new home now. Your strategic path to ownership starts with a single proactive step. Move fast. Get results. Start your journey with Dhugga Mortgages today.

Take Charge of Your 2026 Homeownership Strategy

The path to owning your first home in the GTA is a game of strategy and speed. You’ve learned how to stack the FHSA with the C$60,000 HBP limit. You know how to claim the C$4,000 provincial rebate while navigating the 2026 landscape of 30-year amortizations. Securing a first time home buyer mortgage Ontario doesn’t have to be a source of stress. It’s about having the right data and the right partner to execute your plan. We bring the independently owned and operated reliability you deserve. With access to over 50 Canadian lenders, we make the market work for you.

Don’t wait for the market to move first. We provide the local expertise in Brampton and Mississauga needed to win competitive bidding wars. We handle the complexity. We negotiate the rates. You get the keys. It’s time to stop browsing and start owning. Secure Your 2026 First-Time Buyer Advantage with Dhugga Mortgages. Your future home is within reach. Let’s make it happen today.

Frequently Asked Questions

Who qualifies as a first-time home buyer in Ontario for 2026?

You qualify federally if you haven’t owned a principal residence in the last four years. For the Ontario land transfer tax rebate, the rules are stricter; you must have never owned a home anywhere in the world. This applies to both you and your spouse. We verify your status early to ensure you claim every available credit during the application process.

How much down payment do I need for a house in the GTA?

Minimum requirements depend on the purchase price. For a home under C$500,000, you need 5%. For properties between C$500,001 and C$1,499,999, the requirement is 5% on the first C$500,000 and 10% on the remainder. Any home priced at C$1.5 million or more requires a full 20% down payment. Budgeting for these tiers is the first step toward your first time home buyer mortgage Ontario.

Can I use my RRSP and FHSA together for a down payment?

Yes, you can stack these programs to maximize your initial deposit. You can withdraw up to C$60,000 from your RRSP under the Home Buyers’ Plan and combine it with your total FHSA savings. This strategy is essential for buyers in high-value markets like Brampton or Mississauga. It allows you to use pre-tax dollars to build a robust down payment quickly.

What is the maximum Land Transfer Tax rebate in Ontario?

The maximum provincial rebate is C$4,000 for eligible first-time buyers. If you’re purchasing a property within the City of Toronto, you may also qualify for an additional municipal rebate of up to C$4,475. This brings your total potential tax savings to C$8,475. We factor these rebates into your closing cost calculations to ensure your budget is accurate and transparent.

Do I need a lawyer to close a mortgage in Ontario?

Yes, a real estate lawyer is mandatory to complete your home purchase. They perform the title search, coordinate with the lender to receive funds, and register the property in your name. While we secure the financing, your lawyer handles the legal transfer. We recommend choosing a lawyer who specializes in Ontario real estate to ensure a smooth, error-free closing day.

What is the difference between a mortgage broker and a bank?

A bank only offers its own proprietary products and rates. A mortgage broker acts as an independent intermediary with access to over 50 different lenders across Canada. We compare multiple products simultaneously to find the most competitive terms for your specific profile. This variety creates an advantage for you, especially if you’re self-employed or new to the country.

How long does the mortgage pre-approval process take?

We typically deliver a pre-approval within 24 to 48 hours once your documentation is submitted. Speed is critical in the GTA market. Having your Notice of Assessment and pay stubs ready allows us to move at high velocity. A solid pre-approval lets you shop with confidence and shows sellers you’re a serious, qualified buyer ready to act.

Are there specific grants for first-time buyers in Brampton or Mississauga?

There are no municipal-specific grants for Brampton or Mississauga, but residents qualify for all provincial and federal programs. This includes the First-Time Home Buyers’ Tax Credit and the new GST/HST rebates for new construction. Securing a first time home buyer mortgage Ontario means leveraging these broader incentives to reduce your overall cost of ownership in Peel Region.