Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Mortgage for Permanent Residents in Brampton: 2026 Homebuyer Guide

- Home

- Mortgage for Permanent Residents in Brampton: 2026 Homebuyer Guide

Your Permanent Resident status is your most powerful asset in the Brampton real estate market, yet most newcomers leave money on the table by following outdated bank advice. You’ve worked hard to call Canada home. Now, it’s time to own a piece of it. Securing a mortgage for permanent residents Brampton shouldn’t feel like an uphill battle against a median home price of $895,582. We know the hurdles. Anxiety about a short credit history. Uncertainty about the February 2026 CMHC insurance premium hikes. It’s time for a better approach.

You deserve the same low-interest rates and terms as any other Canadian. This guide simplifies the entire process. Discover how to leverage your PR status for maximum benefit. Learn the secrets to navigating the current 2.25% Bank of Canada overnight rate environment like a pro. We’re going to walk you through the specific CMHC benefits available to you and show you how to land a home in a family-friendly Brampton neighbourhood. Expert guidance. Real results. Let’s get you the keys faster.

Key Takeaways

- Leverage your PR status to access the same high-quality mortgage products and competitive rates as Canadian citizens.

- Qualify for a mortgage for permanent residents Brampton with as little as a 5% down payment through specialized newcomer programs.

- Bypass bank bureaucracy by working with a broker who can access a broader network of alternative lenders for non-traditional income.

- Fast-track your home search by organizing your employment letters and PR documentation before your first professional pre-approval.

- Secure a strategic edge in the Brampton market with a streamlined process tailored to your specific residency and credit profile.

Understanding Your Advantage: Mortgages for Permanent Residents in Brampton

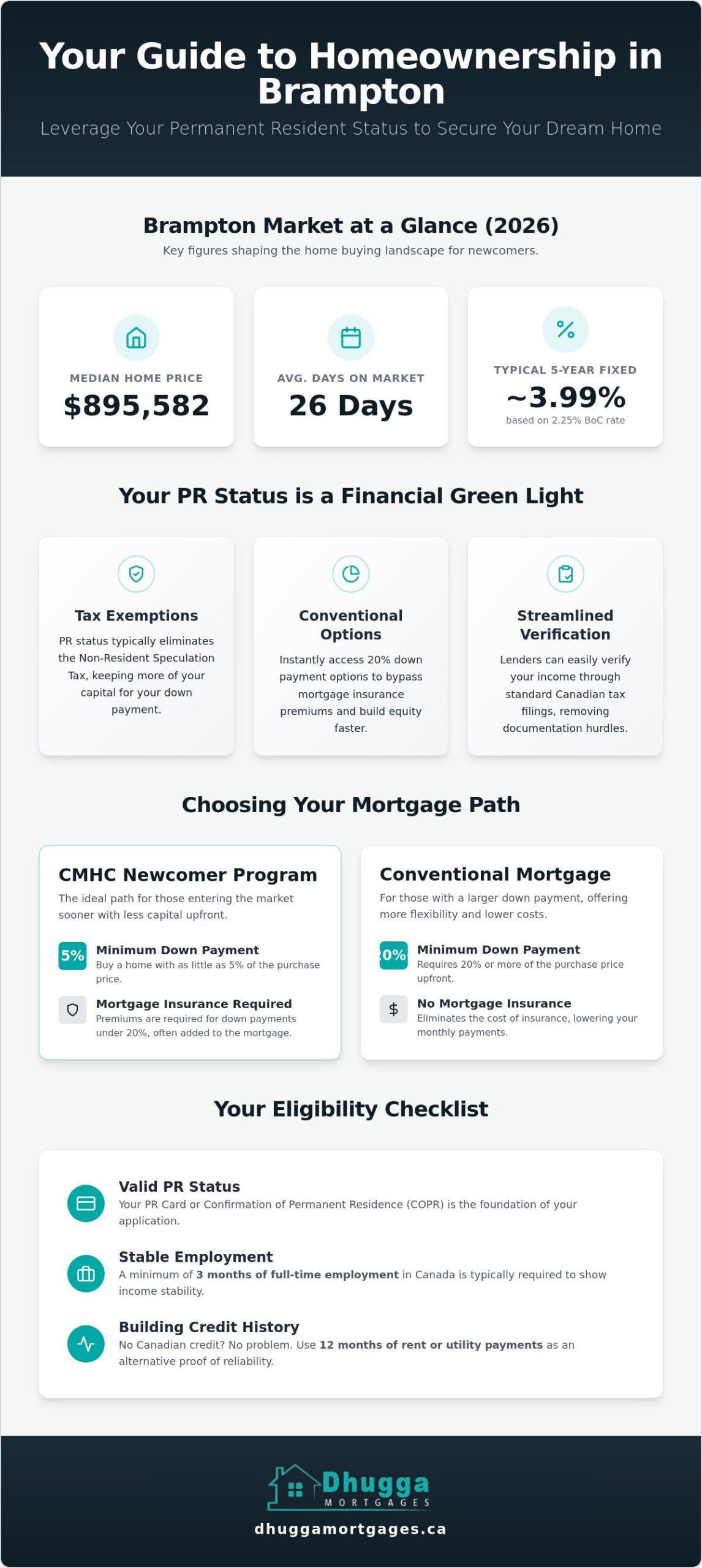

Your Permanent Resident card is more than just an ID. It is a financial green light for Canadian lenders. In the eyes of a bank, PR status signals long-term stability and a commitment to the Ontario economy. This makes a mortgage for permanent residents Brampton one of the most accessible paths to homeownership. You aren’t treated as a high-risk newcomer. You’re treated as a future pillar of the community. In 2026, the Brampton market is moving at a high velocity. With a median home price of $895,582 and properties moving in an average of 26 days, you need to understand your leverage now.

Brampton remains a top choice for PRs because it offers more than just houses. It offers a diverse community and unmatched transit links to the rest of the GTA. Lenders are eager to fund homes here because they recognize the area’s consistent growth. By working with the Canada Mortgage and Housing Corporation (CMHC), many PRs find they can enter the market much sooner than they expected. Don’t let the big banks tell you that you need a decade of history. Your status is your advantage.

Why PR Status Simplifies Your Home Search

- Tax Exemptions: Having PR status typically eliminates concerns regarding the Non-Resident Speculation Tax. This keeps more money in your pocket for your down payment.

- Conventional Options: You can access 20% down payment options immediately. This allows you to bypass mortgage insurance premiums if you have the capital.

- Streamlined Verification: Lenders can verify your income easily through standard Canadian tax filings. This removes the “non-traditional” documentation hurdles that temporary residents often face.

Brampton Market Trends for New Homeowners in 2026

The 2026 market is defined by specific high-growth pockets. Areas like Mount Pleasant and Castlemore are seeing intense interest from families. Brampton is unique because of the massive demand for multi-generational homes. This trend keeps the detached and semi-detached segments competitive. With the Bank of Canada holding the overnight rate at 2.25%, 5-year fixed rates are hovering around 3.99%. This stability is a gift for PRs looking to lock in a predictable monthly payment. Semi-detached homes are currently the “sweet spot” for many first-time PR buyers. They offer the space needed for growing families without the higher price tag of fully detached estates in older neighbourhoods.

Eligibility Criteria and Newcomer Programs You Need to Know

Your Permanent Resident card or Confirmation of Permanent Residence (COPR) is the foundation of your application. Lenders in 2026 generally require you to show at least three months of full-time employment in Canada. This timeline proves you have a stable income stream to support your housing costs. While the big banks might seem rigid, a mortgage for permanent residents Brampton is highly attainable when you meet these core benchmarks. It’s not just about having a job; it’s about showing that your financial life in Canada has officially started. Consistency is what lenders crave.

Passing the numbers test is the next hurdle. Lenders use two specific calculations: Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. These ratios compare your income against your housing costs and existing debts. In a high-value market like Brampton, these figures often determine your maximum purchase price. To get a head start on your budget, use the Mortgage Qualifier Tool to see how your current income aligns with your homeownership goals. Knowing your limit before you visit an open house in Mount Pleasant saves time and prevents heartbreak.

CMHC Newcomer Program vs. Conventional Lending

If you have less than a 20% down payment, you’ll likely use the CMHC Newcomer program. This allows you to buy a home with as little as 5% down. You will need to pay mortgage insurance premiums, which are often rolled into your total loan. Conventional lending requires 20% or more upfront. This path eliminates insurance costs and offers more flexibility through alternative “B-lenders” who might be more lenient with non-traditional income sources. Choosing between these depends on your 2026 cash flow and how quickly you want to build equity in the GTA.

Credit History Requirements: No Credit? No Problem

A thin Canadian credit file doesn’t have to be a dealbreaker. Many newcomer programs allow for alternative credit verification. You can provide 12 months of consistent rent receipts or utility bill payments to prove your reliability. Some lenders will even consider international credit reports from your previous country of residence. We often recommend that PRs open a secured credit card immediately to start building a domestic score. Most clients can establish a strong enough rating within their first year. If you’re unsure how your current history stacks up, you can connect with our team for a quick file review.

Big Banks vs. Mortgage Brokers: Securing the Best Rate

Walking into a big bank branch feels like the logical first step. For many, it’s a mistake. Banks are retailers. They only sell their own products. If you don’t fit their specific, rigid criteria, the answer is a simple “no.” A mortgage for permanent residents Brampton requires a more flexible approach. Brokers don’t work for one bank. We work for you. We shop dozens of lenders simultaneously to find the exact match for your financial profile. This includes major banks, credit unions, and specialized monoline lenders who offer wholesale rates you won’t find on a public website.

Speed is your greatest asset in the 2026 Brampton market. Properties move fast. You can’t afford to wait two weeks for a bank appointment only to be told your file is “complex.” Brokers operate with a sense of urgency. We secure pre-approvals quickly. We handle the heavy lifting. Our goal is to give you a competitive edge before you ever step foot in a Castlemore open house. We negotiate on your behalf to ensure the terms reflect your true earning potential, not just what a computer algorithm says about your T4.

Why Brampton PRs Often Get Rejected by Banks

- The Two-Year Rule: Most big banks demand a strict two-year Canadian work history. This often ignores your professional success before moving to Ontario.

- Foreign Asset Confusion: Banks frequently struggle to verify down payment funds coming from international accounts or family gifts from abroad.

- Lack of Personal Service: You are often just a number in a centralized call centre. There is no local expert to advocate for your unique situation or explain the nuances of your residency status.

The Broker Advantage: Accessing Alternative Lenders

Lenders come in many forms. When a traditional bank says no, alternative lenders often say yes. These institutions specialize in “non-traditional” income and “thin” credit files. They understand that a new Permanent Resident is a high-value client, even without a decade of Canadian data. For those with significant equity but short work histories, private options provide a vital bridge to homeownership. Learn more about private mortgage lenders in Ontario to understand how these strategic partnerships can bypass traditional bank bureaucracy. It’s about finding a lender that sees your future, not just your past.

Step-by-Step: Getting Approved for Your Brampton Mortgage

Don’t start your home search at an open house. Start it with a strategy. A professional pre-approval is the only way to define your Brampton budget with certainty. In a market where the median price sits at $895,582, guessing is not an option. You need to know your maximum purchase price before the bidding wars begin. This is about speed. This is about confidence. Securing a mortgage for permanent residents Brampton requires a proactive stance. We verify your numbers upfront so you can make firm, competitive offers that sellers take seriously.

Down payment verification is often where PR files stall. Lenders require a clear 90-day history for all funds. No exceptions. If you’ve moved money from international accounts, ensure it’s sitting in a Canadian bank well before you apply. Anti-money laundering rules are non-negotiable. If a family member is helping with the purchase, a signed gift letter is mandatory. We help you organize this paper trail early to prevent last-minute delays at the lawyer’s office. Efficiency today means keys in your hand tomorrow.

Documents You Must Organize Before Applying

- Residency Proof: A valid PR Card or your Confirmation of Permanent Residence (COPR).

- Income Verification: A current letter of employment and your two most recent pay stubs from your Canadian employer.

- Credit Data: An international credit report if you’ve been in Canada for less than three years and have a thin domestic file.

- Bank Statements: Three full months of history for every account used to fund your down payment.

Saving for Your Down Payment in Ontario

Maximize your savings using the First Home Savings Account (FHSA). It offers tax-free growth and tax-deductible contributions. It’s the most efficient way to build your capital for the Ontario market. For a deeper dive into these programs, check out our complete guide to first-time home buyer mortgages in Ontario. Remember, in Brampton, your deposit and down payment are different. The deposit is the “good faith” money provided immediately with your offer. In high-demand neighbourhoods, a substantial deposit often signals a serious buyer and can win you the house.

Local expertise matters. Brampton property taxes and closing costs differ from other GTA municipalities. They can be higher than you expect. Don’t get caught off guard by hidden fees on closing day. Contact us to start your pre-approval strategy session today.

Start Your Journey with Dhugga Mortgages in Brampton

The Brampton market doesn’t wait for anyone. To win here, you need more than a pre-approval; you need an edge. Dhugga Mortgages provides that strategic advantage. We don’t just process applications. We build winning files for the local GTA landscape. Securing a mortgage for permanent residents Brampton requires a team that understands the nuances of your residency status and the velocity of our local neighbourhoods. We’re located right here in Brampton. We know the streets, the property tax shifts, and the lenders who actually want your business.

Our process is built for speed. We value your time above all else. No endless waiting for bank appointments. No confusing jargon. We offer a transparent, results-oriented path to homeownership. Whether you are a newcomer or a self-employed professional, we specialize in the complex files that big banks often ignore. We’ve seen the hurdles. We know how to clear them. It’s about moving from “application” to “approved” with zero friction.

Tailored Solutions for New Permanent Residents

Your financial journey in Canada is just beginning. Your mortgage should reflect your future potential, not just your first three months of pay stubs. We design customized mortgage plans that grow alongside your career. Our deep expertise in the New to Canada Mortgage Program ensures you aren’t leaving money on the table. We handle the proactive communication with lenders so you can focus on finding the right home. Stress removed. Confidence restored.

Expert Guidance from Jaspreet Dhugga’s Team

When you work with us, you get direct access to seasoned professionals. You won’t deal with a revolving door of bank staff or centralized call centres. Jaspreet Dhugga’s team acts as your proactive partner throughout the entire process. We have a proven track record of securing approvals where traditional institutions failed. We understand that every PR file is unique. We fight for the rates and terms you deserve. Don’t let a “no” from a bank branch stop your progress. We find the “yes.”

Ready to take the next step? The 2026 market is active, and the best opportunities go to those who are prepared. Get the professional representation you need to succeed in Brampton. Apply now for your Brampton mortgage pre-approval and let’s get your homebuying journey started today. Fast results. Local expertise. Proven success.

Secure Your Future in Brampton Today

Your homeownership goals are within reach. You’ve seen how Permanent Resident status opens doors to the best rates and terms in Ontario. Don’t let bank bureaucracy or a short credit history slow your momentum. You now have the strategic roadmap to navigate the 2026 market with total confidence. By choosing a broker-led path, you gain access to 50+ lenders across Ontario that big banks simply can’t match. It’s about working smarter, not harder.

Speed and precision are critical in the GTA. Organize your documents. Verify your down payment. Partner with a Brampton-based expert who understands the local landscape. Securing a mortgage for permanent residents Brampton is a streamlined process when you have the right guide. We handle the heavy lifting and the complex paperwork so you can focus on finding the perfect home in a neighbourhood you love. We’re here to ensure your transition to Canadian homeownership is seamless and successful.

Take the first step toward your new life now. Experience the peace of mind that comes with fast, efficient approvals for PR holders from Brampton’s trusted newcomer mortgage specialist. Get your Brampton mortgage pre-approval today with Dhugga Mortgages. Your new front door is waiting.

Frequently Asked Questions

Can I get a mortgage in Brampton if I just received my Permanent Residency?

Yes, you can apply for a mortgage the moment you receive your PR status. Lenders view Permanent Residency as a sign of long-term stability. You are eligible for the same mortgage products as Canadian citizens immediately. There is no mandatory waiting period to start your homeownership journey in the GTA.

What is the minimum down payment for a PR buying a home in Ontario?

The minimum down payment is 5% for the first $500,000 of the home’s purchase price and 10% for the portion above that amount. For a typical Brampton home at the median price of $895,582, your minimum down payment would be approximately $64,558. If the purchase price exceeds $1 million, a full 20% down payment is required.

Do I need a Canadian credit score to qualify for a mortgage as a PR?

Not necessarily. While a strong Canadian credit score is helpful, many newcomer programs accept alternative credit history. We can often use 12 months of consistent rent receipts, utility bills, or even international credit reports to secure an approval. We help you build a domestic credit profile quickly while utilizing your existing financial reputation.

Are mortgage rates higher for Permanent Residents than for citizens?

No, mortgage rates are not higher for PR holders. You have access to the same competitive interest rates as any other Canadian resident. Your specific rate is determined by your credit score, down payment size, and total income. PR status ensures you aren’t penalized with “non-resident” surcharges or higher interest tiers.

How long do I need to be employed in Canada before I can apply for a mortgage?

Most lenders require a minimum of three months of full-time employment. You must be past the standard probationary period with your Canadian employer. If you have been transferred to Canada by the same employer you worked for abroad, we can often waive this three-month requirement to get you approved even faster.

Can I use a gift from family abroad for my down payment in Brampton?

Yes, gifted funds from immediate family members are perfectly acceptable. You will need a signed gift letter and a clear 90-day paper trail showing the funds moving from their account to yours. We ensure all international transfers comply with Canadian anti-money laundering regulations to avoid any delays during the closing process.

What is the CMHC Newcomer program and do I qualify as a PR?

The CMHC Newcomer program provides mortgage insurance for residents who have immigrated to Canada within the last five years. It allows you to purchase a home with a lower down payment even with limited Canadian credit history. As a Permanent Resident, you qualify for this program provided you have stable income and meet basic debt-to-income requirements.

Why should I use a mortgage broker instead of my bank in Brampton?

Brokers provide choice and competition that a single bank cannot offer. We shop over 50 different lenders to find the best mortgage for permanent residents Brampton, including wholesale rates and specialized newcomer terms. While a bank branch only sells its own products, we negotiate on your behalf to find the most flexible terms for your specific residency situation.