Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

How to Use a Home Equity Loan for Debt Consolidation: An Ontario Homeowner’s Guide

- Home

- How to Use a Home Equity Loan for Debt Consolidation: An Ontario Homeowner’s Guide

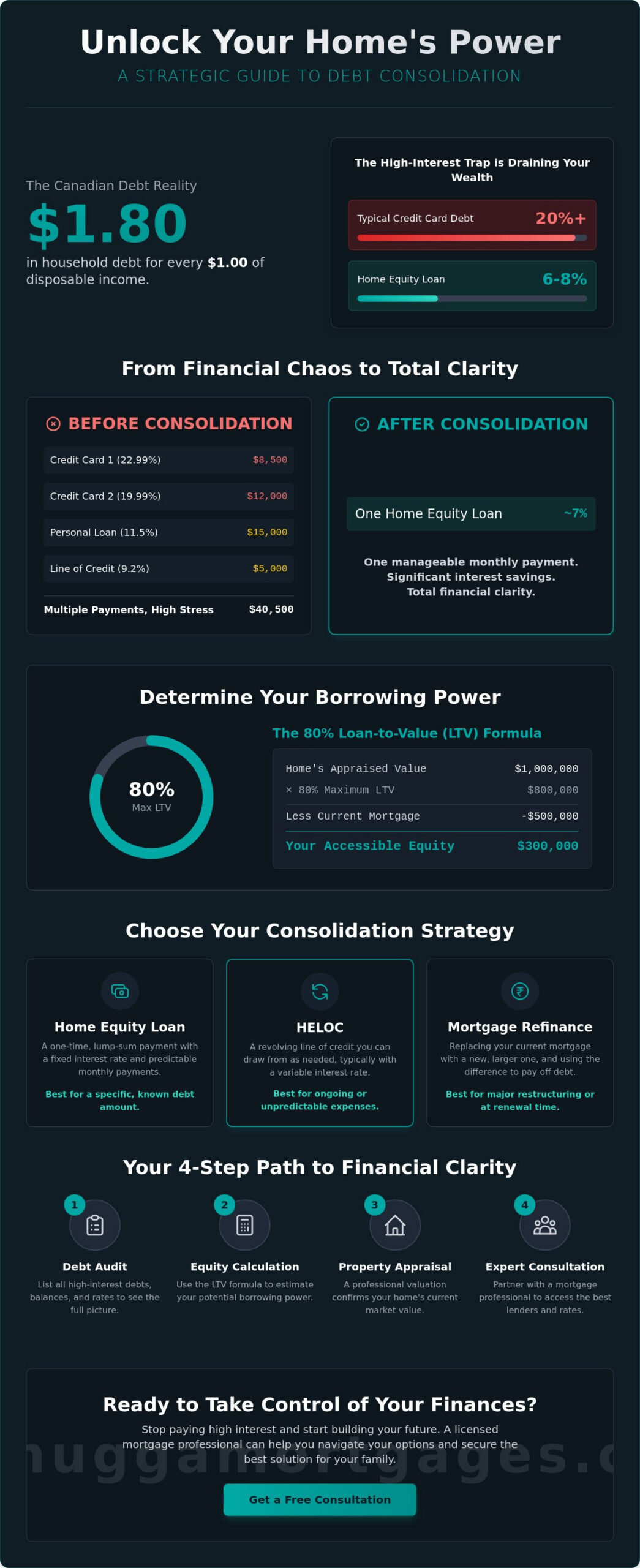

Canadian households now owe $1.80 in debt for every dollar of disposable income. It’s a staggering figure that translates to sleepless nights and constant financial stress for many Ontario families. If you’re currently trapped in a cycle of 20% interest rates on credit cards, your property is likely your most powerful untapped asset. Choosing a home equity loan for debt consolidation isn’t just a way to move numbers around. It’s a strategic cash-flow restructure designed to put money back in your pocket every single month.

You already know that those high-interest payments are draining your bank account and stalling your progress. It feels like you’re running in place while debt continues to grow. We’re here to change that. This guide helps you master the step-by-step process of leveraging your home’s value to wipe out high-interest debt and streamline your monthly obligations. One loan. One payment. Total clarity. We will preview the latest 2026 borrowing limits, explain how to calculate your loan-to-value ratio, and show you how to navigate Ontario’s lending rules with total confidence. It’s time to take control of your equity and realize your financial goals today.

Key Takeaways

- Learn how to slash interest costs by swapping 20% credit card rates for a much lower-interest home equity loan for debt consolidation.

- Understand the “magic number” of lending and how the 80% Loan-to-Value (LTV) rule determines exactly how much equity you can access.

- Discover whether a lump-sum home equity loan, a revolving HELOC, or a full mortgage refinance is the fastest path to your financial freedom.

- Follow our step-by-step audit to organize your balances and prepare your property for a professional appraisal.

- Find out why a local Brampton mortgage broker provides a strategic edge by accessing over 50 lenders that major banks often ignore.

Understanding Home Equity Loans for Debt Consolidation in Ontario

A home equity loan is a powerful financial tool. It provides a one-time, lump-sum payment based on your property’s current appraised value. To understand what is a home equity loan, think of it as converting your home’s paper wealth into liquid cash. This money is then used to wipe out high-interest liabilities immediately. For many GTA families, using a home equity loan for debt consolidation is the fastest way to escape the trap of 20% interest rates on retail credit cards. By replacing that high-cost debt with a loan typically ranging from 6% to 8%, you realize significant savings. This isn’t just about lower rates; it’s about restructuring your entire financial life for better monthly cash flow. One payment. Total clarity.

The immediate impact on your bank account is often dramatic. When you consolidate, you stop the bleeding caused by compounding interest. Instead of sending hundreds of dollars to bank executives in Toronto, that money stays in your pocket. However, this strategy requires a professional eye. Without expert guidance, homeowners can fall into equity-stripping traps where they borrow without a clear repayment plan. We help you organize your finances to ensure this move is a permanent fix, not a temporary band-aid.

Why Ontario Homeowners are Consolidating in 2026

As of June 12, 2026, Canadian households owe approximately $1.80 for every dollar of disposable income. Total household credit market debt has reached a staggering $3.25 trillion. This pressure is felt acutely in Brampton and Mississauga, where the cost of living remains high. While the Bank of Canada held the overnight rate at 2.25% recently, consumer debt interest remains punishing. Fortunately, the significant equity growth in the GTA provides a massive buffer. Leveraging this equity allows you to move from juggling five different creditors to managing one simple payment. The psychological relief is immense. It provides the peace of mind needed to focus on long-term wealth building rather than just surviving the month.

The Difference Between Good and Bad Debt

Not all debt is created equal. Credit card debt is toxic. It carries compounding interest that can double your balance before you even realize what happened. It’s a weight that keeps you stationary. In contrast, a home equity loan is strategic debt. You’re using a low-cost asset to eliminate a high-cost liability. This move allows you to consolidate credit card debt with mortgage products effectively. Don’t just pay interest; build your future. By treating your home as a strategic financial partner, you turn “bad” debt into a manageable, low-cost solution that protects your family’s financial health.

Calculating Your Borrowing Power: LTV and Equity Basics

Your Loan-to-Value (LTV) ratio is the only number that truly matters when you apply for a home equity loan for debt consolidation. It represents the percentage of your home’s value that is currently tied up in debt. In the current Toronto and Caledon markets, lenders use this metric to gauge their risk level. If your home is worth $1 million and you owe $500,000, your LTV is 50%. It’s that simple. Lenders view lower LTV ratios as safer bets, which often results in faster approvals and better interest rates for you.

The 80% rule is the gold standard for traditional refinancing in Canada. Most major lenders won’t let your total debt exceed 80% of the home’s appraised value. To find your usable equity, use this simple formula: (Current Market Value x 0.80) minus your Existing Mortgage Balance. This result is the maximum amount you can potentially pull out to pay off high-interest credit cards or loans. If you aren’t sure where your property stands in today’s market, we can help you estimate your current equity before you commit to a formal appraisal.

Appraisals are a critical part of the process. In fast-moving GTA markets, property values fluctuate monthly. A professional appraiser looks at recent sales in your specific neighbourhood to determine a precise value. This ensures your consolidation plan is based on hard data, not guesswork. It’s the foundation of a successful debt restructuring strategy.

Maximum Borrowing Limits in Ontario

Traditional “A” lenders strictly enforce the 80% LTV cap for refinancing. However, private lenders often provide more flexibility for homeowners in high-demand areas. In the 2026 regulatory environment, LTV remains the primary tool used by OSFI to manage household debt levels across Ontario. If you’re exploring Canadian debt consolidation strategies, knowing your limit is the first step toward a successful application. We specialize in finding the right lender for your specific LTV situation.

The Role of Your Credit Score

Your credit score dictates your interest rate and your lender options. A score of 680 or higher generally unlocks the most competitive rates in Ontario. If your score sits between 600 and 680, you can still qualify, though the terms may vary. For those struggling with a score below 600, don’t panic. There are specialized solutions available. You can still find a bad credit debt consolidation mortgage that fits your needs. We focus on your equity, not just your past credit history, to get you the funds you need quickly. Lenders also review your Debt-to-Income (DTI) ratio, typically looking for a range between 40% and 50% to ensure you can comfortably manage the new payment structure.

Choosing Your Strategy: Home Equity Loan vs. HELOC vs. Refinancing

Selecting the right financial vehicle is just as important as the decision to consolidate. You have three primary paths: a standalone home equity loan, a Home Equity Line of Credit (HELOC), or a full mortgage refinance. Each has a specific impact on your monthly budget and long-term interest costs. If you’re currently locked into a low-rate first mortgage, a full refinance might not be your best move. Breaking that contract often triggers substantial “break fees” or prepayment penalties that can cost thousands of dollars. In these cases, a second mortgage or a home equity loan for debt consolidation allows you to access cash without disturbing your primary low-interest rate.

Speed is often a deciding factor for Ontario families facing aggressive collection calls or looming deadlines. A second mortgage can typically be secured much faster than a traditional bank refinance. It sits behind your existing mortgage, acting as a separate piece of debt with its own terms. While the interest rate might be slightly higher than a first mortgage, the lack of break fees and the rapid approval process often make it the most cost-effective choice for urgent debt relief. We help you run the numbers to see which path leaves more money in your pocket after all fees are considered.

Lump-Sum Home Equity Loans

A lump-sum loan is the gold standard for discipline. It’s best for homeowners who have a specific, fixed amount of debt to eliminate. You receive the funds all at once, pay off your creditors, and then focus on a single, predictable monthly payment. The pros are clear: you get a fixed interest rate and a defined “pay-off” date. There’s no guesswork. The only real con is a lack of future flexibility. If you need more capital six months from now, you’ll have to start a new application. For those who want to kill their debt and never look back, this structure provides the necessary guardrails.

HELOCs: The Flexible Option

A HELOC works like a giant credit card secured by your home. It’s a revolving line of credit that lets you borrow only what you need, when you need it. You only pay interest on the amount you actually use. This is ideal for families who want a safety net or have ongoing expenses. However, flexibility comes with a trade-off. HELOCs in Ontario typically feature variable rates, often starting around Prime plus 0.50%. As of June 2026, with the prime rate at 4.45%, your borrowing cost would be roughly 4.95%. The risk here is “payment shock.” If the Bank of Canada raises rates, your monthly interest costs will climb, which can be dangerous if your budget is already tight.

How to Consolidate Debt Using Your Home Equity: A Step-by-Step Guide

Executing a successful home equity loan for debt consolidation requires a methodical approach. You aren’t just moving debt; you’re restructuring your entire financial profile. Speed and accuracy are your best allies here. Follow this chronological checklist to move from high-interest stress to a single, manageable monthly payment.

- Step 1: Audit your debt. Create a clinical list of every balance. Include credit cards, retail store cards, and high-interest personal loans. Note the exact interest rate for each. This provides the “target” for your new loan.

- Step 2: Determine your home’s current market value. GTA property values move fast. Don’t rely on online estimates. We help you secure a professional appraisal, which typically costs between $400 and $500 in Ontario. This confirms your available equity.

- Step 3: Consult a mortgage broker. Don’t settle for a single bank’s offer. We compare options across 50+ lenders, including private and alternative institutions that specialize in debt restructuring.

- Step 4: Gather your documentation. Speed up the process by having your paperwork ready. Lenders want to see your income stability and current property obligations.

- Step 5: Finalize and payout. Once approved, an Ontario real estate lawyer handles the transaction. They ensure your creditors are paid directly from the loan proceeds, guaranteeing the debt is actually cleared.

Ready to see how much you can save? Contact our team today to start your equity assessment and take the first step toward financial freedom.

Documentation You Will Need

Lenders require a clear picture of your financial health to offer the best rates. Even if you’re self-employed, we have paths to approval. Prepare these items early to avoid delays:

- Your most recent Notice of Assessment (NOA) from the CRA.

- Recent pay stubs or proof of business income.

- Your current mortgage statement and most recent property tax bill.

- A detailed list of the debts you intend to consolidate, including account numbers.

The Closing Process and Legal Fees

In Ontario, a real estate lawyer is required to register the new loan against your property title. This ensures the transaction is legally binding and protects your interests. Legal fees for this process generally range from $2,000 to $3,000 on average. The timeline from your initial application to having funds in hand is often faster than a traditional bank refinance. Once the lawyer receives the funds, they distribute payments directly to your creditors. This “direct payout” method is the most efficient way to ensure your high-interest accounts are closed immediately, preventing the temptation to spend the funds elsewhere.

Why a Brampton Mortgage Broker is Your Best Asset for Debt Restructuring

Walking into a big bank gives you exactly one option. A Brampton mortgage broker changes the game by opening doors to 50+ different lenders. This competition works directly in your favour. We don’t just find a home equity loan for debt consolidation; we find the one lender that fits your specific financial story. Self-employed GTA professionals often face rejection at traditional branches due to complex income structures or unstated earnings. We know how to package your file to highlight your true borrowing power. Our deep roots in Brampton, Mississauga, and Toronto mean we understand local appraisal trends better than a distant corporate office. We take charge of the process so you can focus on your future.

Banks often decline files that seem even slightly complex. We do the opposite. We specialize in navigating the “grey areas” that traditional institutions ignore. Whether you’re dealing with a recent credit dip or a unique property type, we have the lender relationships to get the deal done. Speed is our priority. We move your application through the system with high-velocity efficiency, ensuring you get the funds needed to stop the cycle of high-interest payments immediately. You deserve an advocate who values your time and possesses the expertise to deliver results.

Access to Private and Alternative Lenders

Traditional lenders often hesitate if your credit score has taken a hit from high debt utilization. This is where private mortgage lenders Ontario become your best strategic asset. These loans act as a high-velocity bridge to financial health. They provide the cash you need now to kill 20% interest rates and stop the collection calls. We don’t leave you there. Every private loan we facilitate comes with a clear exit strategy. We help you repair your credit and move back to a prime lender as quickly as possible. It’s a calculated move designed to restore your financial edge and protect your home’s value.

Strategic Debt Management for the Long Term

True debt restructuring isn’t a one-time transaction. It’s the start of a long-term wealth strategy. We partner with you to build a 5-year plan that protects your equity and keeps your cash flow positive. This commitment to your success is a core part of our Debt Consolidation Mortgage Canada pillar guide. Use it as your blueprint for permanent financial change. Don’t settle for a band-aid solution when you can have a total restructure that sets you up for future property investments. Book a strategy session with Jaspreet Dhugga today and let’s put your home equity to work. It’s time to realize your financial potential.

Take Command of Your Financial Future Today

You now have the strategic roadmap to turn your home’s value into your greatest financial advantage. By mastering your LTV ratio and selecting the right home equity loan for debt consolidation, you can effectively silence high-interest creditors for good. Navigating Ontario’s 2026 lending landscape doesn’t have to be a solo journey. We provide the deep local expertise across Brampton, Mississauga, and Toronto to ensure your application is processed with high-velocity efficiency. As an independently owned and operated firm, we offer a personalized touch that large institutional banks simply can’t match. We specialize in finding aggressive solutions for self-employed professionals and those requiring private mortgage bridges. Stop the cycle of overwhelming monthly payments and start building real equity that belongs to you. It’s time to realize your potential and secure the peace of mind your family deserves.

Take control of your debt—get a custom consolidation quote from Dhugga Mortgages

Your path to financial freedom starts with a single, confident decision. We’re ready to take charge of the process and deliver the results you need. Let’s get started.

Frequently Asked Questions

Is it a good idea to use a home equity loan to pay off credit card debt?

Yes, it’s a strategic move when you’re facing 20% interest rates on revolving balances. By using a home equity loan for debt consolidation, you replace toxic, high-interest debt with a lower-interest alternative. This restructure immediately improves your monthly cash flow and helps you pay down the principal balance much faster. It turns unmanageable debt into a structured, predictable repayment plan.

Can I get a home equity loan for debt consolidation with bad credit in Ontario?

Yes, your credit score isn’t the only factor lenders consider in the Ontario market. Many alternative and private lenders prioritize your home’s equity and the property’s location over your credit history. If you have 20% equity or more, we can often secure financing even with a score below 600. We focus on your property’s value to get you approved quickly.

What are the typical interest rates for a second mortgage in the GTA for 2026?

Interest rates vary based on your loan-to-value ratio and overall credit profile. As of June 2026, the Bank of Canada prime rate sits at 4.45%. While HELOCs often start around 4.95%, standalone home equity loans or second mortgages typically carry higher rates than a first mortgage. These rates reflect the lender’s secondary position on your property title and specific risk assessment.

How much equity do I need to qualify for a consolidation loan?

You generally need a minimum of 20% equity in your property to qualify. Canadian regulations cap total borrowing at 80% of your home’s appraised value for a refinance or home equity loan. For a HELOC specifically, you can only borrow up to 65% of the value. However, the combined total of your mortgage and HELOC can still reach that 80% maximum limit.

Will a home equity loan hurt my credit score?

The initial application involves a hard credit inquiry, which might cause a temporary, minor dip in your score. However, using the funds to pay off high-utilization credit cards usually results in a significant score increase within a few months. Reducing your credit utilization ratio is one of the fastest ways to improve your credit standing and demonstrate financial responsibility to future lenders.

Are the fees for a debt consolidation mortgage tax-deductible in Canada?

No, interest and fees for a home equity loan for debt consolidation are not tax-deductible when the debt is for personal use. In Canada, interest is only deductible when the borrowed funds are used to earn income from a business or investment property. You should always consult with a qualified tax professional to understand how these rules apply to your specific financial situation.

How long does it take to get funds from a home equity loan?

The process typically takes between two and four weeks from start to finish. This timeline accounts for the mandatory property appraisal, lender underwriting, and the legal title search conducted by your lawyer. Private lenders can often move much faster, sometimes providing funds in as little as five to seven business days if the appraisal and documentation are prepared in advance.

What happens if I can’t make the payments on my home equity loan?

Your home serves as the primary collateral for the loan. If you default on your payments, the lender has the legal right to initiate a power of sale or foreclosure process to recover their funds. It’s critical to ensure the new monthly payment fits comfortably within your household budget. We help you run the numbers to ensure the new structure is sustainable long term.