Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

When to Use a Private Mortgage Lender: A 2026 How-To Guide for Ontario Homeowners

- Home

- When to Use a Private Mortgage Lender: A 2026 How-To Guide for Ontario Homeowners

What if a higher interest rate was actually the smartest financial move you could make this year? Many Ontario homeowners feel defeated when a big bank rejects their application; however, private capital is a strategic tool rather than a last resort. Knowing exactly when to use a private mortgage lender can save your home purchase or clear your debt when traditional doors close. You need a solution that ignores the stress test and prioritizes your home equity to get the job done fast.

We know the pressure of a looming closing date and the confusion surrounding modern lending fees. It is stressful to feel like you are out of options. This guide promises to show you how to use private financing as a short-term bridge to reach your long-term goals. You will discover the current 2026 fee structures, the impact of the 35% APR cap, and how to build a professional exit strategy to return to bank-rate mortgages. It is time to stop worrying and start executing a plan that works.

Key Takeaways

- Identify the four high-impact scenarios where private financing serves as a strategic bridge, from imminent closing dates to rapid debt consolidation.

- Understand exactly when to use a private mortgage lender to bypass the 2026 mortgage stress test and leverage your home equity effectively.

- Learn how to vet lender fees and legal costs while using interest-only payments to maintain your monthly cash flow.

- Execute a professional exit strategy with specific milestones designed to transition you back to traditional bank-rate mortgages quickly.

Evaluating Your Situation: When the Bank Says No

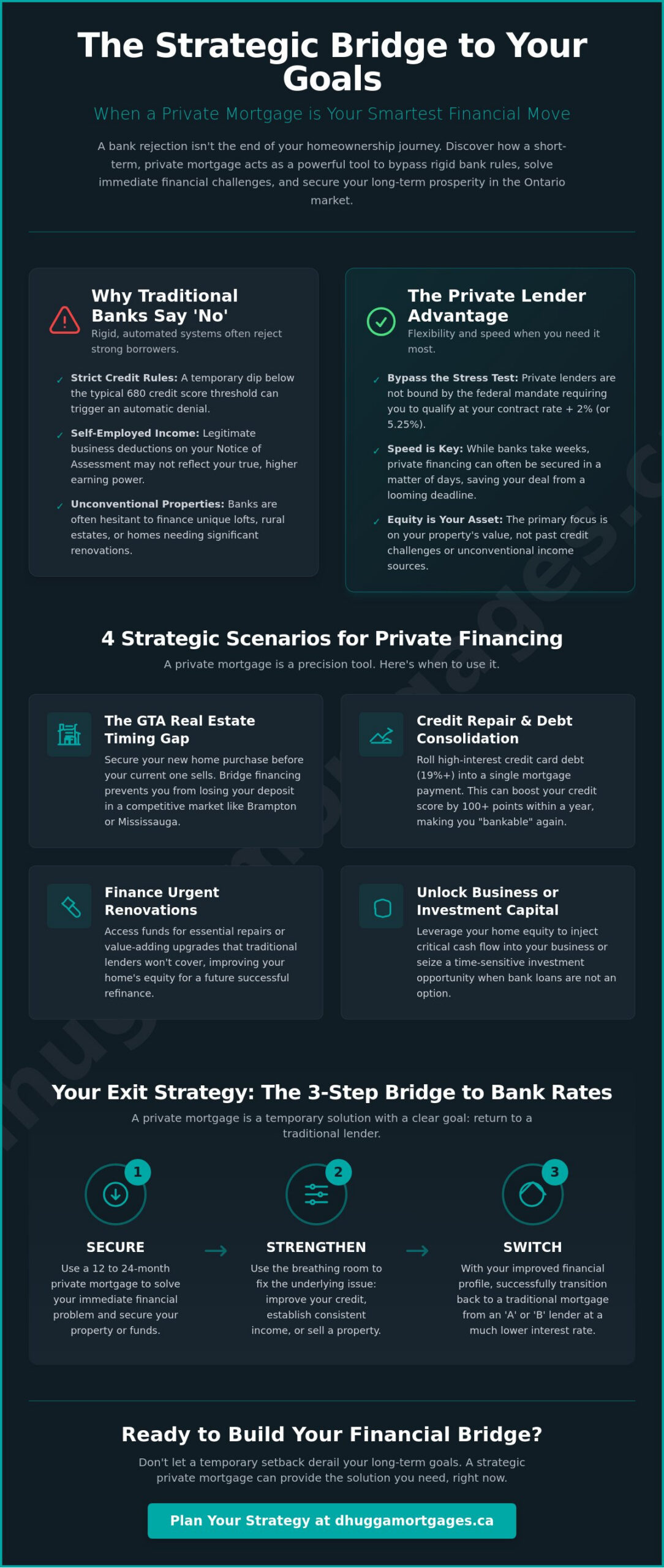

A bank rejection isn’t the end of your homeownership goals. It’s often just a signal to pivot. For many Ontario homeowners, understanding what is a private mortgage helps reframe the situation. These are short-term, equity-based loans provided by individuals or Mortgage Investment Corporations (MICs). Unlike traditional institutions, these lenders care more about the value of your asset than your credit score. They provide the liquidity you need when traditional doors close.

In 2026, the mortgage stress test remains a significant barrier for GTA residents. Borrowers must qualify at a rate that is the higher of 5.25% or their contract rate plus 2%. This rule often disqualifies capable families who simply don’t fit into a rigid box. Private lenders are exempt from this mandate. This is exactly when to use a private mortgage lender to bypass bureaucratic red tape and secure your property before a closing deadline passes.

It is vital to distinguish between ‘B’ lenders and true ‘Private’ lenders. B lenders are typically trust companies or credit unions that still require some income documentation and credit health. True private lenders are the final tier of the lending ladder. They solve temporary hurdles using your property’s equity as the primary security. The goal is simple. Use the equity you have built to solve a specific, time-sensitive financing problem.

Why Traditional Lenders Reject Strong Borrowers

Banks use automated systems that lack flexibility. If you don’t tick every box, your application is denied. Common reasons for rejection in the current market include:

- Credit Score Fluctuations: Life events like a divorce or temporary debt load can drop your score below the bank’s 680 threshold.

- Self-Employed Realities: Your Notice of Assessment might not reflect your true earning power due to legitimate business deductions.

- Unconventional Properties: Banks often shy away from unique lofts, rural estates, or properties needing significant renovation.

The ‘Bridge’ Mindset for Private Financing

Stop looking at the interest rate in isolation. Start looking at the total cost of capital. A private mortgage is a bridge. It gets you from where you are to where you need to be. Knowing when to use a private mortgage lender means recognizing that a one-year term at a higher rate is often cheaper than losing your deposit on a failed home purchase.

Speed is your greatest advantage. While a bank takes weeks to process paperwork, a private lender can often fund in days. This 12 to 24-month period is your time to restructure. Fix your credit. Document your income. Prepare for your return to a traditional bank. Treat this as a strategic move, not a permanent destination. You are buying time to regain your financial edge.

4 Strategic Scenarios for Choosing Private Financing

Private financing is not a one-size-fits-all product. It is a precision tool designed for specific financial gaps. Knowing exactly when to use a private mortgage lender can mean the difference between losing a significant deposit and securing your family’s future. In a fast-moving market like the GTA, certain situations demand the speed and flexibility that only private capital provides. These loans act as a tactical bridge to help you cross over to traditional bank financing once your situation stabilizes.

Scenario 1: The GTA Real Estate Timing Gap

The Greater Toronto Area housing market does not always wait for your paperwork to align. If your new home closes before your current property sells, you face a massive liquidity gap. Private lenders step in to provide rapid bridge financing. This allows you to secure the new property without a “subject to sale” condition, which is often a deal-breaker in competitive Brampton or Mississauga markets. Sometimes, taking out a second mortgage is the best move to keep your existing low-rate first mortgage intact while accessing the cash you need. You can explore how these tools compare in our guide on HELOC vs second mortgage options.

Scenario 2: Credit Repair and Debt Management

High-interest debt is a trap that destroys your borrowing power. If you are carrying credit card balances at 19% or higher, your beacon score will suffer, making bank approval impossible. This is a classic case of when to use a private mortgage lender to reset your finances. By rolling that high-interest debt into a one-year private mortgage, you can often see a credit score boost of 100 points or more within 12 months. This makes you “bankable” again much faster. As noted by a major financial publication, these lenders prioritize the asset’s value over your current credit history. Check out our debt consolidation mortgage Canada guide for a deeper dive into this strategy.

Scenario 3: The ‘Fixer-Upper’ Financing Hurdle

Banks often refuse to fund properties that they deem “uninhabitable” or high-risk. If a kitchen is missing or the roof is failing, traditional lenders will walk away. Private lenders focus on the after-repair value (ARV). They provide the capital to purchase and renovate the home, allowing you to build equity quickly. Once the renovations are complete and the property meets bank standards, you can refinance into a traditional mortgage at a much lower rate.

Scenario 4: Self-Employed Income Realities

Business-for-self (BFS) individuals often have complex tax returns that do not satisfy traditional T1 General requirements. Even with a high net worth, your Notice of Assessment might show a lower income due to legitimate business deductions. Private lenders look at your actual bank statements and the equity in your home instead of just your tax filings. This flexibility is essential for entrepreneurs who need to move quickly on real estate opportunities. If you find yourself in any of these scenarios, speak with our team today to map out your next move.

How to Vet Private Lenders and Avoid Predatory Terms

Speed should never come at the expense of safety. While private financing is a powerful tool, the lack of traditional bank regulation means the burden of due diligence falls on you and your broker. In 2026, the Financial Services Regulatory Authority of Ontario (FSRA) has increased its oversight, but predatory terms still exist in the fine print. Knowing when to use a private mortgage lender involves recognizing a fair deal from a debt trap. You need a transparent partner who prioritizes your successful exit over their own short-term gain.

The total cost of a private mortgage is more than just the interest rate. You must account for the full fee structure. Typical lender fees in Ontario range from 2% to 4% of the loan amount, and brokerage fees usually mirror this range. Additionally, expect legal costs between $1,000 and $3,000, plus appraisal fees. Most private mortgages are structured with interest-only payments. This is a strategic advantage. It keeps your monthly cash flow manageable while you focus on credit repair or property renovations. Accessing capital is fast, but protecting your equity is faster.

Reading the Fine Print in a Private Commitment

Always calculate the effective interest rate. This figure combines the contract rate with all upfront fees to show the true cost of borrowing. A 7.99% rate can quickly become much higher once fees are capitalized. You also need to verify if the term is ‘Open’ or ‘Closed.’ An open mortgage allows you to pay off the balance at any time without a heavy penalty, which is crucial for a smooth exit. In Ontario, independent legal advice (ILA) is a mandatory requirement for private deals. Your lawyer must be a separate professional from the lender’s lawyer to ensure your interests are fully protected.

Watch out for ‘poison pill’ clauses. These include excessive renewal fees that kick in automatically at the end of your 12-month term. Some lenders also bury aggressive pre-payment penalties that make it expensive to return to a traditional bank early. If the Annual Percentage Rate (APR) exceeds the 35% legal limit now enforced in Ontario, walk away immediately. Legitimate lenders stay well below this ceiling.

Why a Broker is Essential for Private Vetting

A professional broker acts as your first line of defence. We provide access to established Mortgage Investment Corporations (MICs) that have proven track records and institutional-grade standards. This is safer than dealing with individual ‘mom and pop’ lenders who may lack the liquidity to fund quickly or the professionalism to handle renewals fairly. At Dhugga Mortgages, we filter for lenders who offer fair mid-term practices and transparent renewal options. We negotiate the renewal clause before you sign the initial deal. This ensures you aren’t held hostage by a lender when your term expires. Our goal is to find the best fit for your specific hurdle, ensuring the bridge you build is solid enough to carry you back to bank-rate financing.

The Step-by-Step Guide to Executing a Successful Exit Strategy

A private mortgage is a tactical bridge, not a permanent residence. Success depends entirely on how you plan to leave it. Knowing when to use a private mortgage lender requires a clear understanding of your return path to traditional bank rates. Without a documented exit strategy, you risk getting stuck in a cycle of high-interest renewals. Follow these five steps to ensure your private loan remains a short-term solution.

- Step 1: Audit the rejection. Identify why the bank said no. Was it a low credit score, high debt ratios, or unconventional income? You can’t fix a problem you haven’t defined.

- Step 2: Set monthly milestones. Build a plan to repair your credit or document your business income. Target a beacon score of 680 or higher to satisfy traditional lenders.

- Step 3: Monitor property value trends. In May 2026, the GTA average selling price was $1,069,700. Keep a close eye on Brampton and Mississauga values to ensure your loan-to-value (LTV) ratio stays within bank requirements.

- Step 4: The four-month rule. Start your re-application process at least four months before the private term expires. This provides a buffer for bank processing times and appraisals.

- Step 5: Finalize the switch. Move your mortgage to an ‘A’ or ‘B’ lender as soon as you meet their criteria. Don’t wait for the final day of your private term.

Milestone Tracking: Your 12-Month Checklist

Your first six months should focus on debt-to-income ratio improvements. Lower your Total Debt Service (TDS) and Gross Debt Service (GDS) ratios by paying down high-interest balances. Between months seven and nine, ensure all tax filings and Notices of Assessment (NOAs) are up to date and paid in full. The exit strategy is the most critical component of the loan.

Common Exit Strategy Pitfalls to Avoid

Avoid taking on new debt. A car lease or a new credit card can instantly disqualify you from a future bank mortgage. Many homeowners also make the mistake of ignoring their renewal date until the final 30 days. This leaves no time for a bank application. Finally, stay aware of market shifts. If values in the GTA soften, your equity position changes. You may need to pay down the principal to meet the bank’s loan-to-value requirements. Stay proactive to protect your equity.

Don’t leave your future to chance. Build your custom exit strategy today and secure your path back to lower rates.

Securing Your GTA Private Mortgage with Dhugga Mortgages

Expertise matters when time is your most expensive commodity. At Dhugga Mortgages, we maintain deep roots in Brampton, Mississauga, and the Greater Toronto Area. We don’t just find the first lender available. We find the best fit for your specific financial hurdle. Our proactive approach ensures that your private financing serves as a strategic advantage rather than a burden. We specialize in fast-track approvals for urgent closings and complex self-employed files that traditional banks often ignore.

Our “Exit-First” philosophy defines how we work. We refuse to fund a mortgage unless we can clearly see a viable way out for you. A private loan is a bridge. If the bridge doesn’t lead to a traditional bank-rate mortgage, we won’t build it. This protects your equity and ensures you aren’t trapped in high-interest debt. Knowing when to use a private mortgage lender is only half the battle. You also need a partner committed to your long-term financial health.

Local Expertise in Brampton and Mississauga Markets

Local property knowledge is critical for appraisal accuracy. A lender who understands the nuances of GTA neighbourhoods will provide more favourable terms based on realistic valuations. We leverage an extensive network of Ontario-based MICs and private investors who trust our local market insights. This allows us to secure funding that others might miss. This regional edge is exactly why homeowners choose us to navigate complex deals. For a deeper look at the landscape, explore our private mortgage lenders Ontario guide.

Your Next Steps to Financial Freedom

Stop guessing and start executing. You can begin a confidential file review with our team today to determine if private financing is the right move for your situation. We move fast because your closing date won’t wait. Have these documents ready for a 24-hour private mortgage quote:

- A recent mortgage statement for your existing loan.

- Your most recent property tax bill.

- A brief summary of your exit goal (credit repair, sale of property, or income seasoning).

- Basic property details for a preliminary valuation.

Take charge of your financial narrative now. Your home equity is a powerful tool when managed with professional guidance. Knowing when to use a private mortgage lender gives you the flexibility to win in a competitive market. Contact Dhugga Mortgages today to secure your funding and start your journey back to traditional bank rates.

Take Command of Your Financial Future

Knowing when to use a private mortgage lender is about spotting a strategic opportunity where traditional banks only see a risk. You now understand that these loans are short-term bridges designed to solve specific hurdles like timing gaps or credit fluctuations. The most critical component is your exit strategy. By setting clear milestones for credit repair or income documentation, you ensure your private mortgage remains a temporary step toward lower bank rates. You have the tools to protect your home equity and move forward with confidence.

Dhugga Mortgages brings seasoned expertise in the Brampton and GTA markets to your file. We are specialists in navigating complex self-employed applications and credit repair scenarios. Our deep network of Ontario private lenders ensures you get a solution tailored to your needs, not just a generic offer. We prioritize your successful exit because your long-term financial health is our primary goal. Stop letting bank rejections slow you down and start executing a plan that works for your unique situation.

Get Your Private Mortgage Strategy Session with Dhugga Mortgages

Your financial recovery starts with a single proactive step. We are ready to help you bridge the gap and secure your future in the Ontario housing market.

Frequently Asked Questions

Can I get a private mortgage with a 500 credit score in Ontario?

Yes, you can secure a private mortgage with a 500 credit score because these lenders prioritize property equity over credit history. Traditional banks will reject scores this low immediately. A private lender focuses instead on the loan-to-value ratio of your home. This is a primary scenario for when to use a private mortgage lender to stabilize your finances while you implement a credit repair plan.

How much are the typical fees for a private mortgage lender in Brampton?

Typical fees for a private mortgage include lender and brokerage fees that each generally range from 2% to 4% of the loan amount. You must also budget for legal costs and a professional appraisal. These fees are standard across the GTA and are often deducted from the loan proceeds at the time of funding. This ensures you don’t need to provide all the cash upfront to close the deal.

Is it possible to get a second mortgage from a private lender if I have a bank mortgage?

Yes, it is very common to secure a private second mortgage while keeping your existing first mortgage with a bank. This strategy allows you to access equity without triggering the heavy pre-payment penalties of breaking a low-rate bank term. It’s an efficient tool for debt consolidation or urgent home repairs. You get the capital you need while maintaining your primary financing at a lower interest rate.

How long does the approval process take for a private mortgage?

The approval process is built for speed and usually takes between 24 and 48 hours. Once you submit your property details and a recent mortgage statement, we can often secure a commitment letter almost immediately. Funding typically follows within 7 to 14 days depending on legal paperwork. This rapid timeline is essential for Ontario homeowners facing imminent closing dates or urgent financial deadlines that banks can’t meet.

What happens if I cannot pay off my private mortgage at the end of the term?

You generally have two options: negotiate a renewal or sell the property to satisfy the debt. Most lenders are willing to renew for another 12-month term if you’ve made your interest-only payments on time, though a renewal fee will apply. This is why we emphasize having a professional exit strategy. You must have a clear path back to traditional bank financing to avoid getting stuck in a high-interest cycle.

Can I use a private mortgage for a self-employed business expansion?

Yes, a private mortgage is an excellent tool for self-employed individuals looking to expand their business operations. Since private lenders focus on equity rather than strict tax returns or Notices of Assessment, you can access capital that a bank would likely deny. It allows you to leverage your home’s value to invest in your company’s growth. This provides the liquidity needed to move quickly on new business opportunities.

Are private mortgage interest rates fixed or variable in 2026?

Private mortgage rates in 2026 are almost exclusively fixed for the duration of the short-term contract. This provides you with predictable interest-only payments while you execute your exit plan. Fixed rates are preferred in the private market because they remove the risk of payment fluctuations during your restructuring period. Because these loans are meant to be temporary bridges, variable rate structures are rarely used by Ontario private investors.

Do private lenders require a full appraisal of my Toronto property?

Yes, almost all private lenders require a full professional appraisal to verify the current market value of your property. Since the loan is secured primarily by the asset, the lender needs a third-party report to confirm the available equity. This step is mandatory for when to use a private mortgage lender in the GTA. It ensures the loan-to-value ratio remains within safe limits for both the borrower and the lender.