Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

The Ultimate Newcomer Mortgage Requirements Checklist for 2026

- Home

- The Ultimate Newcomer Mortgage Requirements Checklist for 2026

Your international credit score effectively disappears the moment you land in Canada, but that doesn’t have to stall your homeownership goals. Many newcomers assume they need years of local history to qualify for a loan. This is a myth. In the 2026 market, meeting the newcomer mortgage requirements is about proving your reliability through non-traditional data. It’s about showing lenders you’re a low-risk borrower using the financial footprint you already have.

We know the GTA housing market moves fast and the costs can feel overwhelming. You’ve worked hard to build a life here. The confusion over PR status or work permit rules shouldn’t stand in your way. You deserve a clear path to your first home. This article promises to simplify the process. You’ll master the exact documentation and eligibility criteria needed to secure a Canadian mortgage, even if your local credit file is currently empty.

Get the facts on 2026 down payment minimums, including the 20 percent rule for homes over 1.5 million dollars. Learn which lenders accept international credit reports. See how utility bills can boost your application. Let’s get your paperwork ready. Stop renting. Start building equity.

Key Takeaways

- Confirm your residency status and employment history to meet the mandatory three-month threshold for a fast approval.

- Unlock the “Alternative Credit” strategy to build a strong borrower profile using your international history and non-traditional data.

- Master the 2026 newcomer mortgage requirements by understanding tiered down payment rules and critical compliance steps for overseas funds.

- Gain the broker advantage by accessing a network of over 50 lenders with flexible policies tailored for new residents.

Understanding the 2026 Newcomer Mortgage Landscape in Ontario

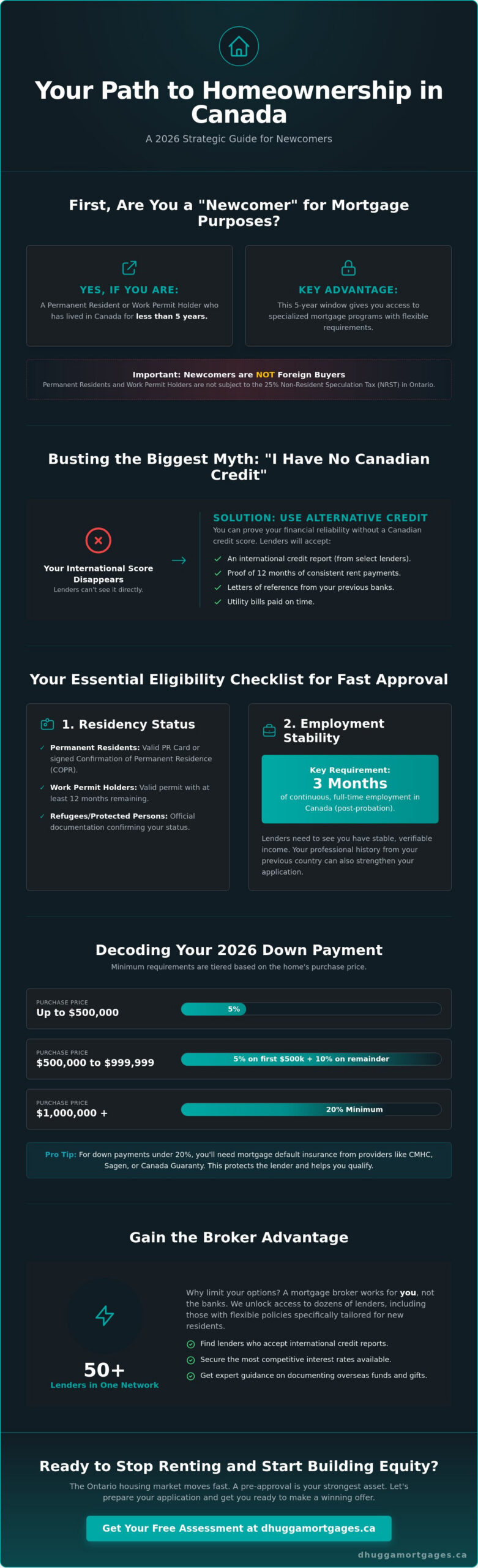

Landing in Ontario is a massive milestone. Buying a home is the next logical step. For mortgage purposes, a “newcomer” is typically defined as a permanent resident or work permit holder who has lived in Canada for less than five years. This five-year window provides access to specialized programs that simplify the qualifying process. Understanding Mortgage Loans is the first step toward securing your future in the Greater Toronto Area.

The 2026 Ontario housing market moves fast. Average prices now hover near $850,000. Success requires a proactive approach. You can’t wait for a local credit score to build up over years. Lenders in 2026 are more flexible with international assets, but they prioritize your Canadian employment stability. Mortgage default insurance from providers like CMHC, Sagen, or Canada Guaranty is often the secret weapon for newcomers. It allows you to enter the market with as little as 5% down on the first $500,000 of a home’s purchase price. These insurers back your loan, which reduces the risk for the bank and helps you secure competitive rates.

Newcomer vs. Foreign Buyer: Knowing the Difference

Don’t confuse newcomer status with being a foreign buyer. Permanent residents and valid work permit holders are not subject to the same restrictions as non-residents. Foreign nationals often face a 25% Non-Resident Speculation Tax (NRST) in Ontario. As a newcomer, your goal is to prove residency. You must have a valid Social Insurance Number (SIN). Lenders need to see you are building a life here, not just investing from afar. Meeting the specific newcomer mortgage requirements early ensures you aren’t grouped with foreign investors who face much higher barriers to entry.

Why 2026 is a Strategic Year for Newcomers in Brampton

Brampton, Mississauga, and Caledon remain high-demand hubs. Inventory levels for semi-detached homes and townhouses are tight, but opportunities exist for those with pre-approvals. With 5-year fixed rates around 4.690%, the 2026 market is more stable than previous years. You can combine newcomer programs with a first time home buyer mortgage Ontario strategy to maximize your benefits. This includes leveraging the $4,000 provincial land transfer tax rebate. Proactive planning helps you realize your homeownership goals faster. Don’t let a lack of Canadian credit history stop you. The programs exist; you just need to know how to access them.

The Essential Eligibility Checklist: Residency and Employment

Efficiency is your biggest advantage in the 2026 Ontario market. Lenders need to see that you’ve planted roots before they approve a loan. This starts with your legal right to live and work in Canada. Proving your status early removes friction from the application process. Meeting the newcomer mortgage requirements isn’t just about having a job; it’s about demonstrating stability through specific paperwork.

Residency Documentation Requirements

Your residency status dictates which mortgage programs you can access. Lenders prioritize borrowers who have a long-term commitment to staying in the country. Ensure you have the following documents ready for immediate review:

- Permanent Residents: A valid Permanent Resident (PR) card or a signed Confirmation of Permanent Residence (COPR).

- Work Permit Holders: A valid work permit with at least 12 months of remaining eligibility. Some lenders may require a history of permit renewals to show continuity.

- Refugees and Protected Persons: Documentation proving your status as a protected person or a successful refugee claimant. These applications often require additional review from specialized lending units.

Securing a Mortgage Approval for Newcomers depends heavily on these foundational documents. Without them, your application will stall before it reaches the underwriting stage.

Employment and Income Verification

Lenders generally require a minimum of three months of full-time employment in Canada. This timeline ensures you have successfully completed your initial probation period. If you’ve recently moved, documenting your professional history from your previous country is vital. It shows you have a consistent career path, even if the location has changed. Professional continuity reduces the perceived risk for the bank. Prepare these items for your file:

- Letter of Employment: A formal document on company letterhead. It must state your position, start date, and guaranteed annual salary or hourly rate.

- Recent Pay Stubs: At least two of your most recent pay slips showing year-to-date earnings and tax deductions.

- Self-Employed Proof: If you’re running your own business, you’ll need two years of Canadian tax returns (NOAs). If you haven’t been here that long, some lenders accept international business records alongside a significant down payment.

Your income must satisfy the Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. These calculations ensure your monthly housing costs and total debts don’t exceed a specific percentage of your gross income. If you’re unsure how your current salary stacks up against 2026 home prices, you can reach out to our team for a quick assessment of your qualifying power. We help you organize these details so you can move from browsing to buying with confidence.

Proving Creditworthiness without a Canadian Credit Score

Your international credit score doesn’t cross the border. It’s a common frustration for many. But a zero score isn’t a “no.” It’s just a different starting point. To meet newcomer mortgage requirements, you need to build a shadow profile. This is the “Alternative Credit” strategy. It proves you’re a low-risk borrower using the bills you already pay every month. Lenders in 2026 are increasingly open to this data if it’s organized correctly.

Consistency is the goal. Lenders typically look for a 12-month history of local Canadian payments. They want to see you’ve managed your new life responsibly since arriving. A letter of reference from a recognized financial institution in your home country also carries significant weight. It validates your past financial character. It tells a story of reliability that a blank Canadian credit report cannot. We help you bridge this gap by presenting your global history as a strategic asset. Understanding how to leverage your international background is a core part of any successful new to Canada mortgage program, and the right documentation strategy can make the difference between approval and rejection.

Alternative Credit Sources Checklist

Start collecting these documents now. Don’t wait until you find a house in Mississauga or Brampton. You need 12 months of on-time payment history for at least two of these sources to satisfy most newcomer programs:

- Utility bills including hydro, water, or natural gas accounts in your name.

- Rental payment history confirmed by a formal lease and matching bank statements showing the funds leaving your account.

- Documentation of other regular, non-negotiable payments like auto insurance premiums or childcare services.

International Credit Reports

Some lenders accept reports from Equifax or TransUnion in your previous country of residence. Request these files early. If the report isn’t in English, you must have it translated by a certified professional. This isn’t just a formality; it’s a requirement for the underwriter’s file. We know which lenders value international history and which ones stick to rigid local rules. Our team helps you package this global data into a format Canadian banks understand. This is your edge. We ensure your past financial success works for your future home in Ontario. Don’t let a lack of local history slow you down. Proactive documentation leads to faster approvals.

Down Payment and Financial Documentation Requirements

Cash is vital, but in the 2026 mortgage market, the paper trail is just as important as the balance. Canadian lenders must adhere to strict Anti-Money Laundering (AML) regulations. This means every dollar you use for your purchase must be verified. Navigating newcomer mortgage requirements means being ready for a deep audit of your global assets. You need to prove the funds weren’t borrowed and that they’ve been in your possession for at least 90 days.

The amount you need depends on the property value. For a home under $500,000, the minimum is 5%. However, with average Ontario prices near $850,000, most newcomers face a tiered system. You’ll pay 5% on the first $500,000 and 10% on the portion above that. If the home exceeds $1.5 million, a full 20% down payment is mandatory. Don’t forget to budget for closing costs. These typically range from 1.5% to 4% of the purchase price. This covers legal fees, inspections, and the Ontario Land Transfer Tax, though first-time buyers can realize a provincial rebate of up to $4,000.

Down Payment Source Checklist

Lenders accept several sources for your down payment, provided they are documented correctly. Gather these records now to avoid delays during the approval process:

- Personal Savings: Bank statements showing the funds sitting in a Canadian account. If recently transferred from abroad, you need the wire transfer receipts.

- Gifted Funds: Money from an immediate family member is acceptable. You must provide a signed “gift letter” confirming the funds are not a loan and do not need to be repaid.

- Property Sales: If you sold a home in your previous country, keep the final sale agreement and the statement of adjustments. Lenders need to see the transition of those funds into your Canadian account.

The 90-Day Rule and Fund Tracking

The “90-day rule” is a standard security measure. Lenders require three months of consecutive bank statements to ensure your down payment is “clean.” They’re looking for stability. Large, unexplained deposits are major red flags. If you move $50,000 into your account suddenly, you’ll have to provide a detailed explanation and supporting documents for that specific deposit.

Organizing statements from multiple countries can be a headache. Ensure every page is included, even the blank ones. If your foreign statements aren’t in English, get them translated by a certified professional immediately. This proactive step prevents last-minute panic. We specialize in helping you package this complex financial history for a seamless review. If you’re ready to see how your savings translate into a 2026 home purchase, contact our team today for a personalized document review. We’ll help you spot potential red flags before the bank does.

Securing Your Advantage with Dhugga Mortgages

Walking into a single big bank limits your options to one set of rules. If you don’t fit their specific newcomer policy, your application stops there. We offer the Broker Edge. By accessing a network of more than 50 lenders, we find the institutions that value your unique financial profile. We understand the newcomer mortgage requirements of 2026 better than anyone else. Our team realizes faster approvals by using pre-packaged documentation kits. We don’t just forward your papers; we package them to ensure underwriters see a low-risk, high-quality borrower from the start.

Efficiency is our standard. We know the 2026 market moves at a high velocity. You need a partner who anticipates hurdles before they appear. Our proactive approach removes the complexity of international credit and foreign fund verification. We take charge of the process so you can focus on finding the right home for your family. This isn’t just about a loan. It’s about a strategic advantage in a competitive landscape. We provide the expert guidance you need to navigate every detail with confidence.

Personalized Guidance for GTA Newcomers

Brampton and Mississauga remain the top choices for new arrivals for a reason. These communities offer established networks and diverse housing options. We specialize in these local markets. We help you identify neighbourhoods that offer the best value for first-time buyers in 2026. If your case involves complex foreign income or non-traditional work history, we have the experience to handle it. We are your dedicated new to Canada mortgage broker Mississauga experts. Our results-oriented strategy ensures your application is positioned for success, regardless of how long you’ve been in the country.

Next Steps: Your Path to Homeownership

The 2026 housing market doesn’t wait for the unprepared. Every day you spend renting is a day you aren’t building equity. Take control of your future now. Our streamlined process is designed to save you time and reduce stress. Follow these steps to secure your home:

- Book a consultation to review your specific newcomer mortgage requirements and identify any documentation gaps.

- Start your pre-approval process immediately to lock in current 2026 interest rates for up to 120 days.

- Use our digital checklist to organize your residency, employment, and down payment records today.

You’ve done the hard work of moving to a new country. Let us do the hard work of securing your financing. We are ready to act immediately. Your first Canadian home is closer than you think. Contact us to start the journey.

Your Path to Homeownership Starts Now

Mastering the newcomer mortgage requirements for 2026 is about preparation and speed. You’ve learned that a lack of Canadian credit history isn’t a barrier when you have the right alternative data. By organizing your residency papers, employment letters, and 90-day fund history, you remove the friction that slows down most applications. The GTA market moves fast. Your financing strategy should move faster.

Dhugga Mortgages offers the edge you need to win in Brampton and Mississauga. We provide access to over 50 Canadian lenders. This ensures you aren’t limited by one bank’s rigid policies. Our specialized newcomer financing experts have a proven track record of turning complex files into successful closings. We handle the paperwork; you focus on the move.

Get Your Newcomer Mortgage Pre-Approval Started with Dhugga Mortgages Today. Don’t wait for the market to change. Take the first step toward building your equity and securing your family’s future in Ontario today. We’re ready to help you succeed.

Frequently Asked Questions

Can I get a mortgage in Canada if I have been here for less than a year?

Yes, you can qualify for a home loan after only three months of full-time Canadian employment. Most lenders simply need to see that you’ve passed your initial probation period. You’ll need a valid work permit or permanent residency status to move forward with your application.

What is the minimum down payment for a newcomer mortgage in Ontario?

The minimum down payment is 5% for the first $500,000 of the purchase price. For the portion between $500,001 and $1,499,999, you’ll need 10%. Properties priced at $1.5 million or more require a full 20% down payment to satisfy federal regulations.

Do I need a Canadian credit score to buy a home in Brampton?

No, you don’t need a local credit score if you use alternative credit validation. Lenders accept 12 months of on-time utility or rental payments to meet newcomer mortgage requirements. International credit reports from your home country also help build a strong case for your reliability.

Are newcomer mortgage rates higher than standard mortgage rates?

Newcomer rates are typically the same as standard market rates. As of May 2026, special offers for 5-year fixed rates sit around 4.690%. You won’t be penalized with higher interest just because you’re new to the country, provided you meet the eligibility criteria.

Can I use a gift from family abroad for my down payment?

Yes, gifted funds from immediate family members are acceptable for your purchase. You must provide a signed gift letter and wire transfer receipts to prove the money isn’t a loan. The funds should ideally be in your Canadian account at least 15 days before your closing date.

What happens if my work permit is set to expire soon?

Lenders generally look for at least 12 months of remaining validity on your work permit at the time of application. If yours is expiring sooner, provide documentation showing you’ve applied for an extension or permanent residency. A stable two-year work history in your specific field also adds significant strength to your file.

Is mortgage insurance mandatory for newcomers?

Insurance is only mandatory if your down payment is less than 20% of the home’s value. This rule applies to all Canadian borrowers, not just new arrivals. If you put down 20% or more, you avoid CMHC, Sagen, or Canada Guaranty premiums entirely.

How long does the newcomer mortgage approval process take?

Pre-approvals often take 24 to 48 hours to complete. A full mortgage approval typically takes 5 to 10 business days once you’ve found a property. This timeline depends on how quickly you can gather your newcomer mortgage requirements, especially international bank statements and employment letters.