Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

New to Canada Mortgage Broker Mississauga: Your 2026 Newcomer Financing Guide

- Home

- New to Canada Mortgage Broker Mississauga: Your 2026 Newcomer Financing Guide

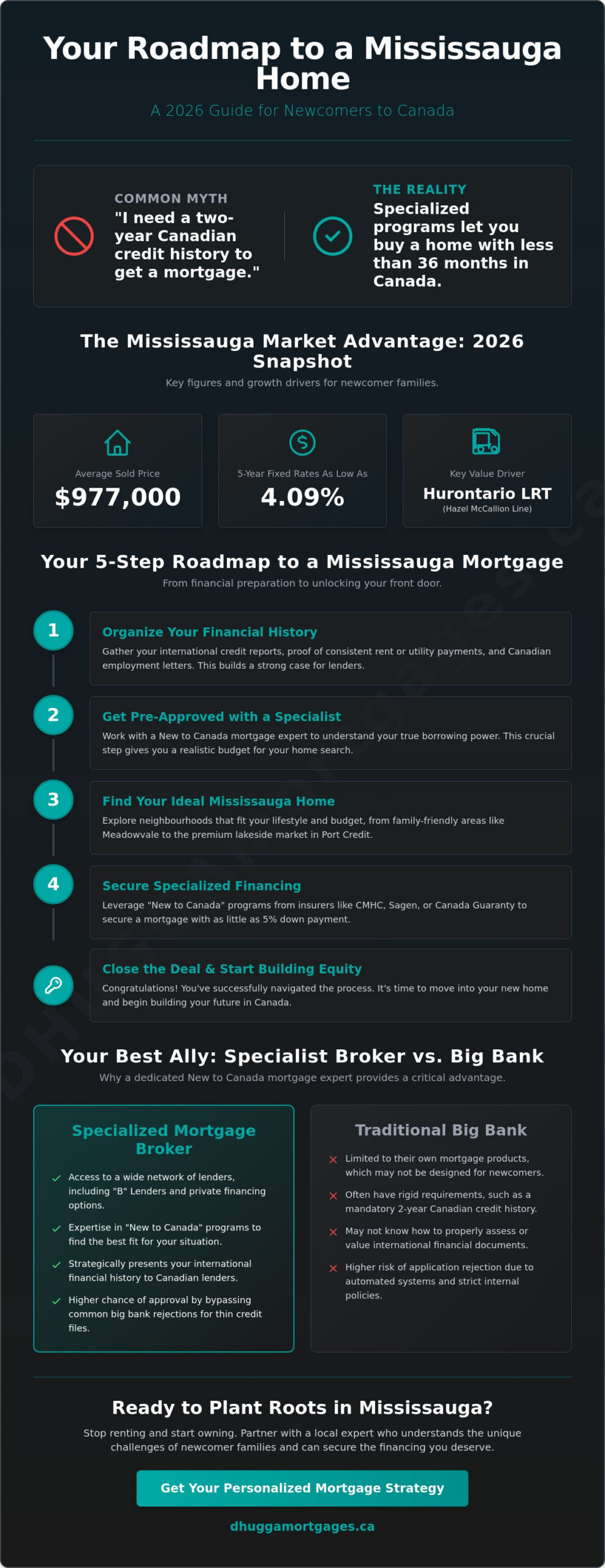

You don’t need a two-year Canadian credit history to unlock the front door of your first home in the GTA. Many newcomers believe they’re stuck renting for years while they build a credit score from scratch. That’s a myth that stops too many families from building equity in a city they love. Moving to Mississauga is a massive transition. You’re likely facing high living costs and the fear that big banks will reject your application because of a thin credit file. It’s frustrating to feel like a visitor when you’re ready to plant roots.

This 2026 guide reveals how to secure a mortgage with as little as 5% down, even if you just arrived. You’ll discover how to leverage international credit reports and specialized newcomer programs to find a competitive rate. We’ll break down the current market, where the average sold price sits at $977,000 and 5-year fixed rates are as low as 4.09%. Working with an expert new to Canada mortgage broker Mississauga gives you the strategic edge to stop renting and start owning. Let’s get you into a safe Mississauga neighbourhood today.

Key Takeaways

- Discover why the Hurontario LRT is driving property value growth in Square One and Cooksville, making Mississauga a strategic 2026 investment.

- Learn how to qualify for specialized financing with as little as 5% down through CMHC, Sagen, or Canada Guaranty programs designed for residents of less than 36 months.

- Find out how a dedicated new to Canada mortgage broker Mississauga bypasses big bank rejections by accessing “B” lenders and private financing options.

- Master the 5-step roadmap to homeownership, starting with organizing your international financial history and Canadian employment letters.

- Gain a competitive edge in the GTA market by partnering with a local expert who understands the unique challenges of newcomer families.

The Mississauga Advantage for Newcomers in 2026

Mississauga has evolved into a global destination that offers much more than just proximity to Toronto. For newcomers arriving in 2026, this city represents a strategic landing spot where economic opportunity meets high quality of life. The city’s infrastructure has seen a massive transformation. The Hazel McCallion Line, also known as the Hurontario LRT, has fundamentally shifted property values in the Square One and Cooksville corridors. This transit link connects Port Credit to Brampton, making these neighbourhoods prime targets for long-term appreciation. If you’re looking for a home that will grow in value, these transit-oriented hubs are the place to start.

The local economy is another major draw. Mississauga’s City Centre has become a thriving tech hub, attracting international talent and providing high-paying jobs close to home. Being minutes away from Pearson International Airport is a logistical dream for families who travel back to their home countries frequently. For multi-generational families, the city’s diverse neighbourhoods offer a range of housing styles. You can find everything from modern high-rise condos to spacious detached homes that accommodate extended family structures. This variety is why so many new Canadians choose to plant roots here.

Navigating the Mississauga Real Estate Market

The 2026 market has entered a stabilization phase, giving buyers more leverage than they had in previous years. Understanding the local geography is vital. Mississauga North, including areas like Meadowvale and Lisgar, often provides better value for semi-detached homes and townhouses. These are perfect for first-time buyers looking for more square footage. Conversely, Mississauga South and the Port Credit area remain premium lakeside markets with a focus on luxury condos and detached properties. Working with a new to Canada mortgage broker Mississauga gives you a distinct advantage over using online-only lenders. A local expert understands these pocket-by-pocket shifts and can help you secure financing that reflects the true value of your chosen neighbourhood.

Why Mississauga is the Ideal Landing Spot

Transitioning to a new country is complex, but Mississauga makes it easier through robust settlement services and cultural hubs. The city is Ontario’s third-largest, offering a stable investment environment for your hard-earned capital. To enter this market, many newcomers utilize programs backed by the Canada Mortgage and Housing Corporation (CMHC). These programs allow for down payments as low as 5% for those with permanent resident status. At Dhugga Mortgages, we specialize in helping families navigate these specific Mississauga opportunities. We don’t just find you a loan; we help you secure a future in a community that values your contribution. Your Canadian dream starts with a smart local strategy.

Understanding “New to Canada” Mortgage Programs

“New to Canada” mortgage programs are specialized financial tools for residents who have lived in the country for less than 36 months. These programs recognize that building a local credit score is a slow process. You shouldn’t have to wait years to start building equity in the GTA. Working with an experienced new to Canada mortgage broker Mississauga ensures you access the right programs immediately. Major insurers like Sagen, Canada Guaranty, and the Canada Mortgage and Housing Corporation (CMHC) provide the backing needed to approve these applications. This insurance bridges the gap, allowing lenders to focus on your global financial health rather than just your local history.

Proving your creditworthiness involves more than just a local bank statement. Lenders often look at international credit reports or alternative proof of payment. Twelve months of consistent rent payments or utility bills can serve as powerful evidence of your reliability. It’s essential to weigh all financial considerations for moving to Canada, including how your existing debts impact your Mississauga borrowing power. We help you assemble a bulletproof file that speaks the language Canadian lenders understand. If you’re unsure where your credit stands, connect with us to review your options.

Criteria for Permanent Residents (PR)

Permanent Residents enjoy the most flexible entry points into the Mississauga market. For homes priced below $1 million, the minimum down payment remains as low as 5%. You’ll typically need to demonstrate 12 months of reliable payment history, which can include international credit references. According to 2026 Sagen guidelines, PR holders can qualify for standard insured financing by providing a valid PR card and proof of stable Canadian employment.

Criteria for Work Permit Holders

Holding a work permit doesn’t mean you’re stuck in the rental cycle. You can qualify for a mortgage if you have a valid permit and a stable income source in the Mississauga area. While down payment requirements can vary, many work permit holders still access 5% to 10% down payment programs. The 2026 foreign buyer ban extension includes clear exemptions for those on active work permits who are working toward permanent residency. You’ll need to provide your most recent T4 or employment contract to verify your status. This path allows you to secure a home while you build your long-term future in Ontario.

Specialized Mortgage Brokers vs. Big Banks for Newcomers

Big banks love predictability. They want a decade of Canadian history and a perfect local credit score. Newcomers rarely fit this rigid mold. If your credit file is thin, traditional lenders often see you as a risk rather than an opportunity. It’s a frustrating reality. One rejection at a major bank isn’t just a “no”; it can actually lower your credit score. This makes your next attempt even harder. You need a partner who sees your global value, not just a local snapshot. Don’t let a bank’s algorithm dictate your future in Ontario.

A new to Canada mortgage broker Mississauga provides the perspective you need. We don’t rely on a single lender’s algorithm. Instead, we tap into a network of over 50 lenders, including “B” lenders and private financing options. These institutions are often more flexible with recent arrivals. They understand that a lack of Canadian credit history doesn’t mean a lack of financial responsibility. We package your application to highlight your international assets and professional background. We turn your global success into Canadian borrowing power. We focus on results, not just paperwork.

The best part? This expertise costs you nothing. In the Canadian mortgage industry, lenders pay the broker’s commission. You get professional guidance, access to better rates, and a streamlined process without a service fee. It’s a “free to you” model that puts the advantage back in your hands. We do the heavy lifting. You reap the rewards.

The Limitations of Traditional Banking

Banks have a narrow focus. They offer a limited variety of products designed for the average Canadian borrower. For a newcomer, this lack of variety is a major barrier. Their rigid credit score requirements penalize you for being new. They don’t have the tools to verify international financial history or alternative proof of payment. This “one-size-fits-all” approach fails families who have the income but lack the local history. Don’t settle for a bank’s limitations when you can have a broker’s options. Speed and variety are the keys to 2026 financing.

The Broker Advantage in Mississauga

Navigating the GTA market requires local expertise and a personalized touch. We realize that immigrant finances are often complex. You might have funds coming from overseas or a non-traditional employment structure. We provide a strategic edge by finding exclusive newcomer rates not advertised to the public. Our deep knowledge of first time home buyer mortgage Ontario programs helps you maximize your savings. We handle the negotiations. We manage the stress. You get the keys to your Mississauga home faster. Partner with a new to Canada mortgage broker Mississauga to secure your spot in a safe, thriving neighbourhood today.

Your 5-Step Roadmap to a Mississauga Mortgage

Securing a home in the GTA requires a tactical approach. You can’t afford to guess your budget in a market where the average sold price is $977,000. Follow this streamlined roadmap to move from newcomer to homeowner with confidence. Preparation is your greatest asset. Speed is your competitive edge.

Step 1: Organize your history. Gather your international financial records and Canadian employment letters immediately. Lenders need to see stability. Step 2: Connect with a local expert. Partner with a new to Canada mortgage broker Mississauga to assess your true borrowing power. We look at your global assets to find options banks miss. Step 3: Secure a pre-approval. Don’t start your search without a locked-in rate. With the best 5-year fixed rates at 4.09% as of May 2026, knowing your exact numbers keeps your offers competitive. Step 4: Find your home and calculate costs. Navigate Mississauga-specific closing costs before you fall in love with a property. Step 5: Finalize and move. Complete the paperwork and get the keys to your new Canadian life.

Essential Documentation Checklist

Lenders require a specific paper trail for newcomer files. You’ll need your valid status documents, such as a PR card or a valid Work Permit. Proof of down payment is critical. If family members abroad are assisting you, ensure you have a signed gift letter and a clear record of the wire transfer. Gather your most recent Canadian T4s or international tax returns to verify your income history. Having these ready prevents delays during the underwriting process. If you aren’t sure if your documents meet the criteria, contact our team today for a professional review.

Closing Costs and Hidden Fees

The purchase price isn’t the only number that matters. Budget for the Ontario Land Transfer Tax. First-time homebuyers in Ontario can receive a refund of up to $4,000, which helps offset this cost. You must also account for legal fees and home inspection costs, which are standard for Peel Region properties. Mississauga approved a 5.21% blended property tax increase for 2026, so factor this into your monthly carrying costs. We help you realize the full cost of ownership before you sign. No surprises. Just a clear path to your front door.

Why Newcomers Choose Dhugga Mortgages in Mississauga

Choosing the right new to Canada mortgage broker Mississauga is the final step in securing your future. It’s about more than just a loan. It’s about finding a partner who understands the immigrant experience. Jaspreet Dhugga provides that strategic edge. We don’t just process applications. We advocate for families. Our deep roots in Mississauga, Brampton, and Caledon mean we know the local market dynamics better than anyone. We prioritize speed and reliability. When you’re anxious about a closing date, you need a broker who acts fast. You need results you can count on.

Through the Mortgage Alliance network, we provide access to the most competitive 2026 rates. This includes exclusive offers from major banks and private lenders alike. We work to find the best fit for your unique situation. Whether you’re looking for a first-time home buyer mortgage or a specialized newcomer program, we have the reach to make it happen. We leverage our industry connections to give you an advantage that big banks simply can’t match.

A Proactive Partner for Your Journey

We cut through the noise. Canadian mortgage terminology can be confusing. We simplify complex jargon into clear, actionable advice. You’ll always know exactly where you stand. Our track record speaks for itself. We’ve helped countless newcomers secure financing even after big banks said no. We handle the complexity so you can focus on your move. It’s a streamlined, efficient process designed for your peace of mind. We remove the friction from your application. You get a clear path to homeownership without the stress.

Beyond the Mortgage: A Community Expert

Our support doesn’t end when you get the keys. We help you build Canadian credit quickly. This prepares you for future refinancing or property investment opportunities. We also connect you with a trusted network of local professionals. Whether you need a real estate lawyer or a home inspector in Peel Region, we have the right referrals. We’re your community-focused guide in a new country. We want to see you thrive in your new Mississauga neighbourhood. Your success is our success. We’re here to help you plant deep roots in Ontario.

Ready to start your journey? Connect with Jaspreet Dhugga today.

Start Your Mississauga Journey Today

Owning a home in Ontario is more than a financial move; it’s the foundation of your family’s new life. You’ve seen that a thin Canadian credit file doesn’t have to stop your progress. Specialized newcomer programs and flexible lenders are ready to help you plant roots. The right strategy turns your international success into local borrowing power. You don’t have to navigate this complex market alone. A dedicated new to Canada mortgage broker Mississauga provides the strategic edge you need to win in a competitive environment.

Jaspreet Dhugga has served the Mississauga and Brampton communities for nearly a decade. As a specialized newcomer financing expert and a member of the Mortgage Alliance network, we offer the speed and reliability you deserve. We handle the complexity. You focus on the move. Stop wondering if you qualify and start planning your housewarming party. Efficiency is our priority. Your peace of mind is our goal.

Secure your Mississauga newcomer mortgage pre-approval today!

Welcome home. Your Canadian dream is closer than you think. Let’s make it a reality together.

Frequently Asked Questions

How long do I need to be in Canada before I can apply for a mortgage in Mississauga?

You can apply for a mortgage immediately if you have permanent resident status and a stable Canadian income. Most lenders prefer to see at least three months of full-time employment history in Canada. Newcomer programs are specifically designed for those who have been in the country for less than 36 months. If you have a strong professional background and a valid work contract, your journey to homeownership can start the moment you land.

What is the minimum down payment for a newcomer mortgage in Ontario?

The minimum down payment is 5% for permanent residents purchasing a home under $500,000. For properties between $500,000 and $1,499,999, you need 5% on the first $500,000 and 10% on the remaining balance. Since the average Mississauga house price is $976,943, most buyers should budget for a blended down payment of approximately 7.5%. This allows you to secure a home without waiting years to save a full 20%.

Can I get a mortgage on a work permit in Mississauga?

Work permit holders can absolutely secure a mortgage in Mississauga. You must have a valid permit and be legally authorized to work in Canada to qualify for CMHC-insured loans. Lenders will verify your income through employment letters and recent pay stubs. While some programs may require a higher down payment for non-PR status, many permit holders still access competitive rates. It’s a proactive way to build equity while you work toward permanent residency.

Do I need a Canadian credit score to buy a home as a newcomer?

A traditional Canadian credit score is not a mandatory requirement for newcomer financing. Lenders often accept international credit reports or alternative proof of reliability. You can use 12 months of consistent rent payments or utility bills to demonstrate your creditworthiness. Working with an expert new to Canada mortgage broker Mississauga is the best way to present this alternative data. We package your global financial history to ensure lenders see your full potential.

Are there specific grants for first-time home buyers who are new to Canada?

Newcomers can access several provincial and federal incentives. Ontario offers a land transfer tax refund of up to $4,000 for first-time buyers. Additionally, the 2026 temporary HST rebate applies to newly built homes up to $1 million. You can also use the Home Buyers’ Plan to withdraw up to $60,000 from your RRSP tax-free for a down payment. These programs significantly reduce the initial cost of entering the Mississauga market.

How does a mortgage broker differ from a bank for a newcomer?

A broker provides access to a vast network of lenders, whereas a bank only sells its own products. This variety is crucial for newcomers who don’t meet the rigid criteria of major banks. A new to Canada mortgage broker Mississauga finds “B” lenders who prioritize your income over a thin credit file. This strategic approach ensures you get competitive 2026 rates while avoiding the credit damage of a bank rejection. We work for you, not the lender.

What happens if my down payment is coming from a gift outside of Canada?

Lenders accept gifted down payments from immediate family members living outside of Canada. You must provide a signed gift letter and a clear record of the wire transfer into your Canadian account. Lenders typically want to see these funds in your account at least 15 to 30 days before the closing date. This documentation proves the money is not a loan and ensures a smooth approval process for your Mississauga home purchase.

Can I qualify for a mortgage if I am self-employed and new to Canada?

Self-employed newcomers can qualify for a mortgage, but the documentation requirements are more extensive. You typically need to provide two years of business history and tax assessments to prove stable earnings. However, some specialized programs allow for “stated income” if you have a significant down payment. We help you organize your bank statements and contracts to show lenders the strength of your business. It’s a complex path that requires a proactive and expert approach.