Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

First Time Home Buyer Incentives Ontario: The Complete 2026 Guide

- Home

- First Time Home Buyer Incentives Ontario: The Complete 2026 Guide

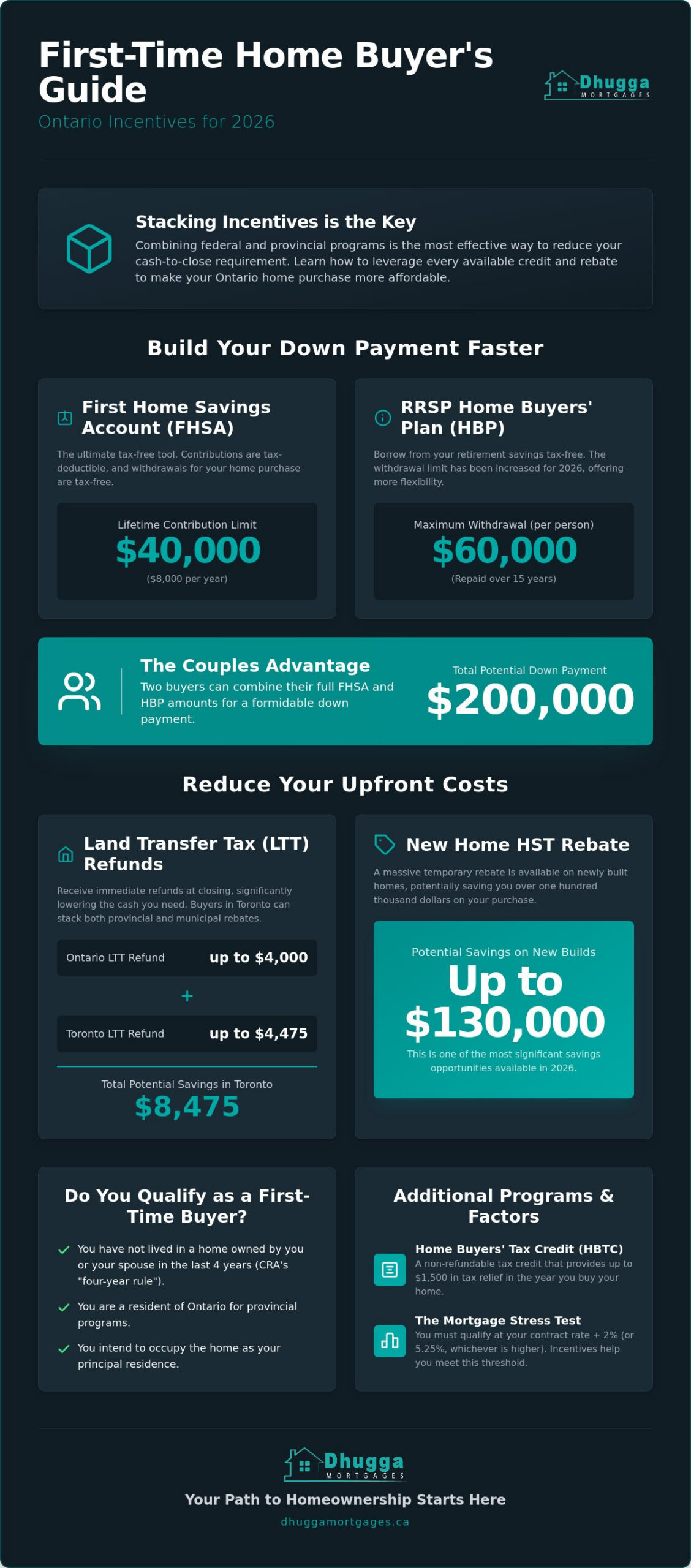

Stacking the right government credits can slash your upfront costs by over $130,000 in 2026. Most buyers leave money on the table because they don’t know how to combine federal and provincial programs. It’s frustrating to watch interest rates fluctuate while you’re struggling to save for a massive down payment. You deserve a clear path to homeownership. This guide simplifies every first time home buyer incentives Ontario program currently available. We’ll help you cut through the confusion and keep more cash in your pocket.

You’ll learn exactly how to maximize your savings using the latest 2026 rules. We cover the increased $60,000 RRSP withdrawal limit and the massive temporary HST rebate on new builds. We also show you how to stack the Ontario and Toronto land transfer tax refunds to save up to $8,475 at closing. Stop guessing and start planning with confidence. Here is your roadmap to a more affordable Ontario home. Get the edge you need to secure your first property now.

Key Takeaways

- Maximize your down payment by combining the $60,000 RRSP withdrawal limit with the tax-free growth of an FHSA.

- Stack provincial and municipal rebates to save up to $8,475 on land transfer taxes for properties within the City of Toronto.

- Use our comprehensive list of first time home buyer incentives Ontario to significantly lower the total cash required at closing.

- Unlock massive potential savings of up to $130,000 through the temporary HST rebate available on newly built homes.

- Navigate the 2026 mortgage stress test with expert guidance to ensure your application is approved quickly and efficiently.

Understanding the 2026 First-Time Home Buyer Incentive Landscape

2026 is the year to act. Government updates have shifted the math in your favour. The primary goal for any new buyer is simple. You need to reduce your cash-to-close requirement. This is the total liquid capital you must provide on moving day for your down payment and legal fees. Using first time home buyer incentives Ontario programs is the most effective way to bridge the affordability gap in the current market. You aren’t just looking for a loan. You’re looking for a strategic advantage.

You must distinguish between your tools. A tax credit like the HBTC lowers your annual income tax bill. A rebate, such as the Land Transfer Tax refund, provides immediate relief at the lawyer’s office. A savings vehicle like the First Home Savings Account (FHSA) allows you to grow your down payment with tax-deductible contributions. Understanding how these interact is the key to a successful purchase. We help you stack these benefits to maximize every dollar.

Who Qualifies as a First-Time Buyer in Ontario?

You might be a first-time buyer even if you’ve owned before. The CRA applies a four-year rule. If you haven’t lived in a home that you or your spouse owned in the last four years, you qualify again. This is a massive opportunity for those returning to the market. Be mindful of spousal history. If your partner owns a property, it may disqualify you from certain provincial rebates. Ontario residency is also mandatory for provincial programs. We verify these details early to avoid surprises at closing. Speed and accuracy matter here.

The 2026 Affordability Reality in the GTA

The market in Brampton, Mississauga, and Toronto remains fast-paced. As of July 2026, the average Ontario home price is approximately $850,000. This makes the mortgage stress test a significant hurdle. You must qualify at 5.25% or your contract rate plus 2%. With the Bank of Canada policy rate at 2.25%, qualifying is easier than in previous years, but it still requires precision. Incentives aren’t just bonuses anymore. They are essential tools to help you pass the stress test and secure a lower interest rate. Professional guidance ensures you navigate these moving targets without friction. We provide the local expertise you need to win in the GTA.

Federal Powerhouses: The FHSA and RRSP Home Buyers’ Plan

Federal incentives are your primary engine for growth. In 2026, updated rules give you more room to move. You can now access more capital than ever before. This is where you build your financial foundation. Most buyers treat these as separate options. That is a mistake. You need to view them as a combined force to maximize your first time home buyer incentives Ontario strategy. The math is clear. Stacking these tools is the fastest way to a larger down payment.

Couples have a massive advantage in the GTA market. You can stack these programs to create a formidable fund. Two people can pull $120,000 from their RRSPs. They can also use $80,000 from their FHSAs. That is $200,000 in tax-advantaged cash. This liquidity covers your down payment and the costs remaining after your Ontario Land Transfer Tax Refund is applied. If you want to see how this fits your specific budget, speak with our team today.

Maximizing the FHSA in 2026

The First Home Savings Account (FHSA) is the ultimate tax-free tool. Contributions are tax-deductible, which lowers your annual tax bill. Withdrawals for your home purchase are entirely tax-free. It combines the best features of an RRSP and a TFSA. You can contribute up to $8,000 annually with a lifetime limit of $40,000. If you don’t buy within the 15-year limit, you can transfer the balance to an RRSP without losing contribution room. This flexibility makes the FHSA superior to the HBP for many long-term savers. It’s a proactive way to build wealth while planning your move.

The RRSP Home Buyers’ Plan (HBP) Update

The RRSP Home Buyers’ Plan (HBP) remains a cornerstone of Canadian homeownership. It allows you to borrow from your retirement savings without immediate tax penalties. As of 2026, the HBP withdrawal limit is a $60,000 per person maximum. You have a grace period before the 15-year repayment window begins. These funds are versatile. Use them for a standard purchase, a new build, or even “live-in” renovations. It’s a powerful way to leverage your existing savings for immediate use in Brampton or Mississauga.

- Repayment: You must repay the HBP in equal instalments over 15 years.

- Tax Impact: Missed repayments are added to your taxable income for that year.

- Timing: Funds must be in your RRSP for at least 90 days before withdrawal.

Ontario-Specific Savings: Land Transfer Tax and HST Rebates

Provincial incentives provide the immediate relief you need on closing day. While federal tools build your down payment, Ontario-specific programs target your closing costs. The Ontario Land Transfer Tax (LTT) Refund is your primary provincial tool. It offers a maximum refund of $4,000. For homes purchased for $368,000 or less, this refund covers the entire tax amount. In the current market, this is a vital component of your first time home buyer incentives Ontario strategy. You see the savings at the lawyer’s office. It directly reduces the liquid cash required to finalize your purchase.

Timing is everything. You must claim these rebates at the time of registration to avoid paying the tax upfront and waiting for a refund. We ensure your paperwork is ready for a seamless transaction. If you’ve already utilized the RRSP Home Buyers’ Plan (HBP) to boost your down payment, these provincial rebates protect your remaining cash reserves. It’s about maintaining liquidity throughout the entire process.

The Toronto Municipal Land Transfer Tax Rebate

Buying within the 416 area code introduces a “double tax” challenge. Toronto is the only city in Ontario with its own municipal land transfer tax. However, first-time buyers have a specific advantage here. The Toronto Municipal Land Transfer Tax Rebate offers up to $4,475 in additional savings. When you stack this with the provincial refund, your total tax relief reaches $8,475.

Consider the difference between closing in Brampton versus Toronto. A buyer in Brampton only pays the provincial tax and receives the $4,000 refund. A buyer in Toronto pays both taxes but receives both rebates. This combined support helps offset the higher property values found in the city core. We help you calculate these exact figures for your specific postal code. No surprises. Just clear numbers.

Rebates for New Builds and Substantial Renovations

New construction offers the largest potential savings in 2026. The GST/HST New Housing Rebate provides significant relief for buyers of newly built homes. A temporary Ontario rebate now covers the full 13% HST on homes valued up to $1 million. This can result in savings of up to $130,000. It’s a massive boost to your purchasing power.

- Price Caps: The full federal GST rebate applies to homes up to $1 million.

- Phasing Out: Partial rebates are available for properties between $1 million and $1.5 million.

- Assignment Sales: Be cautious. Buying a contract from another buyer can disqualify you from these rebates.

Eligibility thresholds are strict. If your purchase price exceeds $1.5 million, these specific first time home buyer incentives Ontario disappear. We verify the contract details early to protect your rebate eligibility. Precision ensures you don’t leave six figures on the table.

Qualifying Beyond the Incentives: Debt, Credit, and the Stress Test

Incentives are powerful tools, but they don’t work in a vacuum. You can stack every available credit, but if you fail the mortgage stress test, the deal dies. Your financial health is the engine that drives your application. Lenders prioritize your credit score and debt ratios before they consider your rebates. In an Ontario market where average prices hover around $850,000, your qualifying power is everything. We focus on cleaning up your credit and managing debt so you can actually access the first time home buyer incentives Ontario offers. You need a solid foundation to build your future.

Your credit score determines your interest rate. A higher score unlocks lower rates, which directly impacts your monthly affordability. Even a small difference in your rate can save you tens of thousands of dollars over your mortgage term. We help you identify quick wins to boost your score before you apply. This proactive approach ensures you aren’t just qualifying, but qualifying for the best possible terms. If your ratios are tight, we look at alternative lenders who offer more flexibility than the big banks. Ready to see your numbers? Contact us for a pre-approval to get started.

The Mortgage Stress Test in 2026

The 2026 stress test remains a significant hurdle for GTA buyers. You must qualify at the higher of 5.25% or your contract rate plus 2%. With the Bank of Canada policy rate at 2.25%, your qualifying rate is likely near 6%. This reduces your maximum loan amount. Lowering your Total Debt Service (TDS) ratio is the fastest way to increase your budget. Pay down high-interest credit cards and car loans before you start house hunting. In many cases, adding a co-signer is a strategic move to bridge the gap in the current Ontario market. It provides the extra weight needed to satisfy strict lender requirements.

Specialized Situations: Newcomers and Business Owners

Traditional banks often struggle with non-standard income. If you run your own business, you need a specific self-employed mortgage Canada strategy. We help you prove your income using bank statements and contracts rather than just T4 slips. New arrivals face similar challenges with limited Canadian credit history. The new to Canada mortgage program allows recent immigrants to secure financing with as little as 5% down. These specialized programs work alongside provincial incentives to make homeownership a reality. We handle the complex paperwork so you can focus on finding the right home in Brampton or Mississauga.

Your Path to Homeownership: The Dhugga Mortgages Advantage

Navigating first time home buyer incentives Ontario requires more than a simple checklist. It requires a high-velocity partner who understands the GTA landscape. Big banks often move at a glacial pace. They have rigid criteria that can leave unique buyers behind. We operate differently. We provide a streamlined path to approval by connecting you with a broad network of lenders. This includes traditional banks, credit unions, and alternative options. We handle the heavy lifting of stacking your FHSA and HBP funds. We ensure every rebate is claimed accurately and on time. Your move should be exciting, not exhausting.

We’ve spent years mastering the specific market conditions in Brampton, Mississauga, and Toronto. We know how to position your application for success. Our team focuses on the “now.” We act immediately to secure your advantage in a competitive environment. From the first phone call to the final signature, we are your proactive guide. We don’t just provide a service. We provide a strategic edge. We bridge the gap between your initial pre-approval and the moment you finally hold the keys to your new home.

Why Work with a GTA Mortgage Expert?

A generic mortgage doesn’t work in a specialized market. You need a first time home buyer mortgage Ontario plan that accounts for your career path and long-term goals. We offer personalized planning that goes beyond the interest rate. We look at your total financial health. This includes optimizing your debt ratios and credit profile before you submit an application. Our communication is direct and results-oriented. We value your time above all else. We remove the complexity so you can move forward with confidence and clarity.

Next Steps: Get Pre-Approved Today

The market waits for no one. A pre-approval is your most powerful tool when shopping for a home. It transforms you from a browser into a serious buyer with real negotiating power. Our 24-hour pre-approval goal ensures you stay ahead of the competition. To move at high velocity, please have the following documents ready for your consultation:

- Recent pay stubs and your current employment letter.

- Your last two years of T4 slips and Notices of Assessment from the CRA.

- Proof of down payment, including current FHSA or RRSP statements.

- A valid piece of government-issued photo ID.

Take charge of your future in the Ontario real estate market. We are ready to act. Let’s secure your first home together. Contact our team today to begin your journey with a partner who delivers results quickly.

Take Control of Your 2026 Buying Power

2026 is the year to secure your future in the Ontario market. You now have the blueprints to stack every federal and provincial credit available. Combining high-limit RRSP withdrawals with the tax-free growth of an FHSA builds a formidable down payment. Don’t let the stress test or closing costs hold you back. We help you navigate every first time home buyer incentives Ontario program with total precision. We remove the complexity. You focus on finding the right property in Brampton, Mississauga, or Toronto.

We are your proactive partner in this journey. As a GTA Local Expert, we specialize in Fast 24-Hour Pre-Approvals that give you immediate negotiating power. We also offer Specialized Newcomer & Self-Employed Programs to ensure every financial profile has a path to success. Stop guessing and start planning with a team that values your time. Your first home is closer than you think. Get Started with Your 2026 First-Time Buyer Strategy at Dhugga Mortgages today. Let’s get you the keys to your new home.

Frequently Asked Questions

Can I use the FHSA and the RRSP Home Buyers’ Plan together in 2026?

Yes, you can stack both accounts to maximize your down payment. A couple can withdraw up to $120,000 from their RRSPs while also utilizing their FHSA balances. This is a core part of first time home buyer incentives Ontario strategies in 2026. It provides a massive cash injection when you need it most. We help you coordinate these withdrawals to avoid tax penalties and ensure your funds are ready for closing.

How much is the Land Transfer Tax rebate for first-time buyers in Ontario?

The provincial rebate is worth a maximum of $4,000. This amount fully covers the land transfer tax for homes priced at $368,000 or less. For properties above this price, you pay the remaining tax balance. If you buy in Toronto, you qualify for an additional municipal rebate of up to $4,475. Combining both can save you up to $8,475 at the lawyer’s office.

Do I qualify for first-time buyer incentives if my spouse has owned a home before?

You qualify for federal programs like the HBP if you haven’t lived in a home owned by your spouse in the last four years. Provincial rules are much tighter. In Ontario, you are disqualified from the Land Transfer Tax refund if your spouse owned a home anywhere in the world while they were your spouse. We review your marital history and ownership timeline to confirm your specific eligibility.

What is the First-Time Home Buyers’ Tax Credit (HBTC) worth in 2026?

The HBTC is a $10,000 non-refundable tax credit that provides up to $1,500 in direct tax savings. You claim this credit on your personal income tax return for the year you purchased your home. It’s a simple way to recoup some of your moving and legal costs. While it doesn’t provide cash at closing, it significantly lowers your tax bill the following spring.

Are there specific incentives for first-time buyers in Brampton or Mississauga?

Brampton and Mississauga buyers rely on provincial and federal programs rather than municipal-specific rebates. You receive the $4,000 Ontario Land Transfer Tax refund and all federal credits. Since property values in Peel Region are often high, stacking the FHSA and HBP is your best path to affordability. We specialize in navigating these programs for clients in the Brampton and Mississauga markets.

What happens to my incentives if I decide to rent out my first home?

Most incentives require you to use the property as your principal residence within one year of purchase. If you rent it out too early, you may be required to repay the GST/HST rebate or face tax consequences for HBP withdrawals. These programs are designed to help owner-occupants, not investors. Always consult with our team before changing your property’s use to avoid an unexpected bill from the CRA.

Is there a price limit on the homes that qualify for Ontario incentives?

There is no hard price limit for the LTT refund, but the benefit caps at $4,000. However, first time home buyer incentives Ontario for new builds have strict thresholds. The full GST/HST New Housing Rebate is only available for homes up to $1 million. Partial rebates are available for properties between $1 million and $1.5 million. Once the price exceeds $1.5 million, these rebates disappear entirely.

How do I apply for the GST/HST new housing rebate?

You typically apply through your builder during the closing process. Most builders apply the rebate directly to the purchase price to lower your total cost. If the builder does not handle this, you must file Form GST190 with the CRA within two years of your closing date. We ensure your purchase agreement is structured correctly so you don’t miss out on these substantial savings.