Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

How to Get a Mortgage When Self-Employed: The 2026 Ontario Roadmap

- Home

- How to Get a Mortgage When Self-Employed: The 2026 Ontario Roadmap

What if your tax return is actually the biggest obstacle to your new home? You’ve spent years building a successful business in Ontario. Now, traditional banks are penalizing you for the same tax deductions that helped you grow. It’s a frustrating cycle for the 13.2% of Canadians who are self-employed. You need to know how to get a mortgage when self-employed without the standard T4 roadblocks. We understand that your taxable income rarely tells the full story of your financial strength.

You shouldn’t be forced to choose between tax efficiency and homeownership. We promise to show you exactly how to navigate the 2026 lending landscape to secure your spot in the GTA market. This roadmap simplifies the process. We will cover the specific documents you need. You’ll learn the critical differences between ‘A’ and ‘B’ lenders and how to use your business bank statements to prove your real worth. It’s time to stop worrying about paperwork and start planning your move.

Key Takeaways

- Understand why lenders view Business for Self (BFS) applicants differently and how to overcome the T4 documentation gap.

- Discover how to get a mortgage when self-employed by leveraging stated income programs that reflect your actual earnings rather than just your taxable net.

- Identify the right lender tier for your needs, from Big Banks to alternative B-lenders offering more flexible income verification.

- Organize your BFS Survival Kit with the specific tax documents and business records required for a streamlined approval process in Ontario.

- Learn the advantage of professional packaging to highlight your business growth and access wholesale rates not available to the public.

The Self-Employed Mortgage Challenge: Why Banks Say No

Banks love T4 slips. They provide a simple, predictable story that fits neatly into a computer algorithm. Your business story is more complex. If you’re “Business for Self” (BFS), you’re an outlier in the traditional banking world. The system is built for employees; it isn’t built for entrepreneurs. Understanding how to get a mortgage when self-employed starts with recognizing why the standard process often fails you. Lenders view business owners as higher risk because your income isn’t guaranteed by a third-party employer. They see fluctuations where you see growth. They see uncertainty where you see opportunity.

The two-year business history is the standard benchmark for most Big 5 banks. They want to see two years of steady, or ideally increasing, income on your tax returns. This is a hurdle, but it isn’t an absolute wall. Modern BFS borrowers often require Flexible Mortgage Options to bridge the gap between their bank statements and their tax returns. We focus on the reality of your cash flow, not just the history on a page. You’ve built a business. You shouldn’t be penalized for that success.

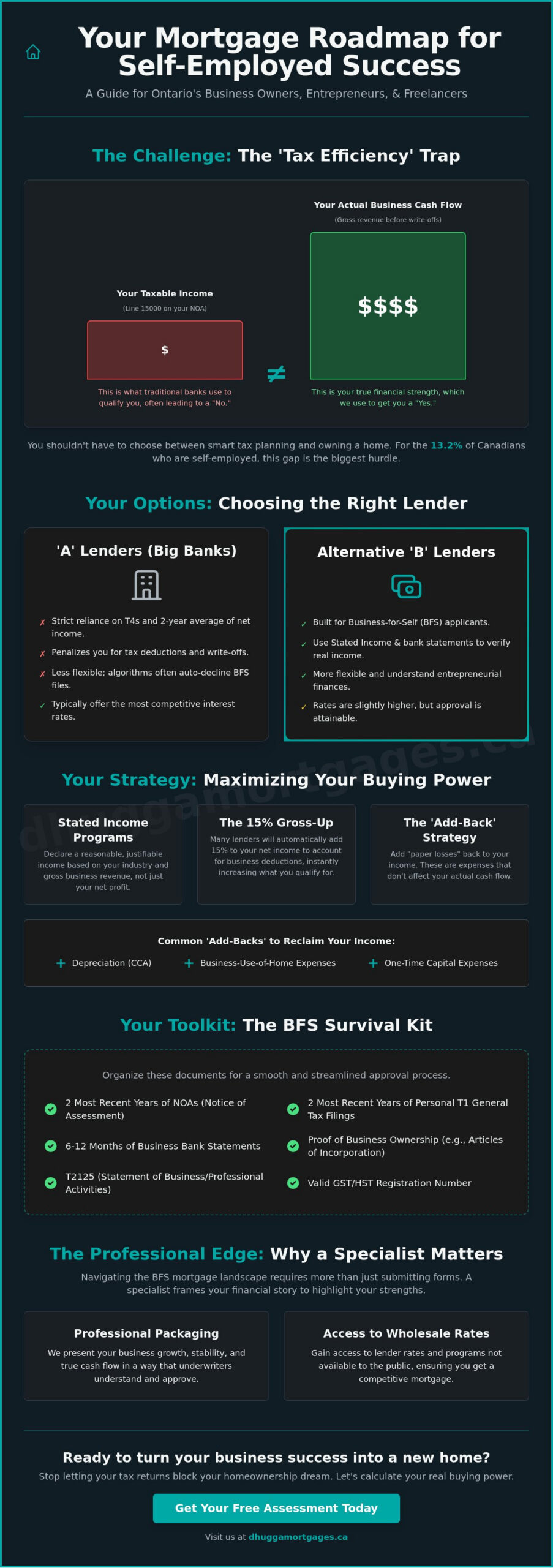

The ‘Tax Efficiency’ Trap for Ontario Business Owners

You work with your accountant to minimize your tax bill. You write off the truck, the equipment, and the home office. This is smart business. Your “Line 15000” income on your Notice of Assessment (NOA) drops, which is great for your bank account but terrible for your borrowing power. Traditional Gross Debt Service (GDS) ratios are calculated based on that lower taxable number. In the GTA, where the average home price is approaching $850,000, a low paper income will trigger an automatic decline. You end up rich on paper but “poor” in the eyes of the bank. This trap stops thousands of qualified Ontario business owners from entering the market every year.

Who Qualifies as Self-Employed in the Eyes of a Lender?

Lenders don’t just look at what you do; they look at how you’re structured. Are you a sole proprietor, an incorporated business owner, or a gig economy professional? Generally, if you own 25% or more of a business, you’re classified as BFS. This classification changes the rules of the game. It dictates the specific “BFS Survival Kit” of documentation you’ll need to provide. Whether you’re a freelance consultant in Toronto or a tradesperson in Brampton, your ownership percentage is the first thing a lender will verify. Your structure determines your path to approval.

Stated Income vs. Net Income: Calculating Your Real Buying Power

Traditional lenders love the simplicity of a T4. For you, they typically use a two-year average of your net income from your Notice of Assessment. This math often works against you. If your income is trending upward, they’ll average the two years; if it’s trending downward, they’ll usually take the lower, more recent number. This rigid approach doesn’t reflect your actual buying power or business growth. Understanding how to get a mortgage when self-employed requires a shift toward stated income programs.

Stated income, or “alt-doc” programs, are designed for borrowers with strong credit scores who have legitimate reasons for low taxable income. These programs allow you to state a reasonable income based on your gross business revenue rather than just your net profit. Many lenders also offer a “15% gross-up.” This means they take your net income and automatically add 15% to account for the business expenses you’ve deducted. It’s a quick way to boost your qualifying power without extra paperwork.

Mastering the ‘Add-Back’ Strategy

Your tax return includes “paper losses” that don’t actually reduce the cash in your pocket. Savvy brokers look for these “add-backs” to strengthen your application. Common examples include:

- Depreciation (Capital Cost Allowance): A non-cash expense for equipment or vehicles.

- Business-use-of-home: Expenses you’d pay anyway, like utilities or insurance.

- One-time expenses: Large, non-recurring business investments that won’t happen next year.

By identifying these paper losses, you can effectively increase your qualifying income by thousands of dollars. If you’re unsure which expenses qualify for your specific situation, reach out to our team for a quick review of your recent tax filings.

The Impact of Your Business Structure

Your legal structure dictates the documents a lender will demand. Sole proprietors are the most straightforward; lenders focus on your personal T1 General and the T2125 (Statement of Business or Professional Activities). This form is the heartbeat of your application. It shows the lender exactly where your money goes and where we can find hidden borrowing power.

If you are incorporated, you have more leverage. Lenders can look at your corporate financial statements and retained earnings. If your corporation is profitable but you only pay yourself a small salary to save on taxes, we can often use a portion of those corporate earnings to qualify you for a much higher mortgage amount. Your structure is a tool. Use it correctly to maximize your edge in the Ontario market.

Comparing Your Options: From Big Banks to Private Lenders

The Ontario mortgage market is a hierarchy. It’s not one-size-fits-all. When you’re researching how to get a mortgage when self-employed, you’ll find three distinct tiers of lenders. Each has its own appetite for risk. Each has its own documentation demands. Choosing the wrong tier can lead to a quick decline. Choosing the right one secures your home.

A-Lenders are the Big 5 banks. They offer the lowest interest rates in Canada, currently around 4.09% for a 5-year fixed high-ratio mortgage as of May 2026. However, they are the most rigid. They demand “clean” income. This means two years of consistent NOAs that match your mortgage request. If your tax write-offs are high, an A-lender will likely decline your application because your “on-paper” income doesn’t meet their strict debt-service ratios.

B-Lenders are often trust companies or credit unions. They are the middle ground. They understand that entrepreneurs have complex finances. They are more flexible with income verification, often using bank statements to prove cash flow instead of just tax returns. The trade-off is a slightly higher interest rate and a typical requirement of a 20% down payment. They are built for borrowers who are “rich in cash” but “poor on paper.”

Private Lenders are the final tier. These are individuals or investment groups. They focus on the equity in the property rather than your income history. They offer interest-only payments. This is a strategic move for a short-term fix or a unique GTA property situation where traditional financing isn’t an option.

When to Pivot to Alternative (B) Lending

Don’t view a B-lender as a failure. View it as a bridge. Many entrepreneurs in Mississauga and Brampton choose B-lending because it allows them to buy a home now. You don’t have to wait years to show higher taxable income. You pay a slightly higher rate to gain immediate homeownership. This is often better than paying rent while you wait for your “clean” income to catch up. If your situation is even more unique, you might need Private Mortgage Lenders Ontario: The 2026 Strategic Guide to Alternative Financing to secure your property and maintain your business momentum.

The Role of Mortgage Default Insurance (CMHC/Sagen)

If you have less than a 20% down payment, you’ll need mortgage default insurance. This is mandatory in Canada for high-ratio loans. CMHC is the standard provider, but they have strict guidelines for BFS borrowers. You must show a minimum credit score of 600 to qualify. There is a big difference between “insured” and “insurable” BFS programs. Sagen and Canada Guaranty often provide more flexibility for self-employed Canadians through their Alt-A programs. These programs are specifically designed for those who can’t prove their full income through traditional means but have a strong credit history. Knowing how to get a mortgage when self-employed with a low down payment means knowing which insurer will actually support your file.

Step-by-Step: Your Roadmap to Approval While Self-Employed

Success in the Ontario real estate market doesn’t happen by accident. It requires a tactical approach. While salaried employees rely on a simple pay stub, your path involves proving stability through a well-organized narrative. Knowing how to get a mortgage when self-employed is about more than just having money in the bank. It’s about timing, documentation, and choosing the right lending tier before you ever step foot in an open house. The GTA market moves fast. You must move faster. Don’t let a missing tax document or a sudden credit dip kill your deal at the finish line.

Start by organizing your “BFS Survival Kit” to establish your baseline. Once your files are ready, focus on your credit score. A score of 700 or higher is typically the magic number to access A-lender rates. After your score is polished, consult a specialist broker to determine if you fit the A, B, or Private lender profile. Secure a pre-approval immediately to lock in your rate. Finally, finalize your down payment source. Lenders require a clear 90-day history for all funds. If you’re transferring equity from your business or receiving a gift, you’ll need the paper trail to prove it.

The Essential Documentation Checklist

- Tax Records: Provide your full T1 General tax returns and matching Notices of Assessment (NOAs) for the last two years.

- Business Proof: Supply your Articles of Incorporation or a valid business licence to confirm you’ve been operating for at least 24 months.

- Revenue Flow: Prepare 6 to 12 months of business bank statements to demonstrate consistent cash flow and operational health.

Preparing Your Credit and Down Payment

Lenders scrutinize BFS applicants with extra care. They want to see that you manage personal debt as effectively as your business expenses. If you’re a first-time buyer in Brampton or Toronto, your down payment strategy is critical. Whether you’re using saved earnings or gifted funds, every dollar needs a documented history. For those just starting their journey, our First Time Home Buyer Mortgage Ontario: The Complete 2026 Strategic Guide provides the specific breakdown you need to succeed.

Ready to see which mortgage tier fits your business profile? Contact our team today to start your pre-approval process.

Why a Self-Employed Mortgage Specialist Gives You the Edge

Walking into a big bank as a business owner is often a waste of your time. They see a file that doesn’t fit their box. We see a success story that needs the right audience. Knowing how to get a mortgage when self-employed requires more than just submitting a pile of papers. It requires strategic “packaging.” We highlight your business growth and mitigate year-over-year income fluctuations. Our team presents your financial strength in a language that underwriters actually understand. This isn’t just data entry. It’s advocacy for your homeownership goals.

Our process protects your credit score. When you apply at multiple banks yourself, each inquiry can lower your score. We use a “one application, many lenders” approach. One credit pull gives you access to dozens of options. This preserves your borrowing power while we shop for the best terms. You also gain access to wholesale B-lender rates. These are exclusive rates not available to the public walking off the street. We use our volume and established reputation to secure a competitive edge for your specific file.

Custom Strategies for GTA Business Owners

The GTA market is fast and unforgiving. Property values in Toronto, Mississauga, and Brampton require precise appraisals to satisfy lenders. We know how to navigate high-value appraisals for self-employed buyers. We’ve managed cases where a major bank issued a decline based on a single year of high expenses, yet we secured a “yes” by demonstrating a strong three-year trajectory. The Dhugga Advantage is built on proactive communication and rapid closing times. We handle the complexity. You focus on your business.

Taking the Next Step Toward Homeownership

Don’t wait for the next tax season to start your assessment. You might already qualify under a stated income or alt-doc program. Every month you wait is a month of missed equity growth in the Ontario market. Realize your true borrowing potential now. It’s time to stop guessing and start planning your move with a partner who understands the entrepreneur’s journey. Ready to see what you qualify for? Contact Dhugga Mortgages today.

Secure Your Future in the Ontario Market

You’ve built your business with vision and persistence. Now it’s time to apply that same strategic mindset to your homeownership goals. Tax write-offs don’t have to be a dead end for your borrowing power. By using stated income programs and looking beyond traditional banks, you can bridge the gap between your tax returns and your real buying power. You have the roadmap. You know the tiers of lending. You have the checklist for your BFS Survival Kit.

Mastering how to get a mortgage when self-employed is about choosing a partner who understands the local landscape. We bring deep roots in the Brampton and Mississauga communities to every file. With access to over 50 residential and commercial lenders, we find the competitive edge that a standard bank branch simply can’t offer. Our expertise in alternative and private lending ensures your application is packaged for success from day one.

Don’t let another year pass while you wait for “perfect” tax returns. Take control of your financial story right now. Get your self-employed mortgage pre-approval in Brampton today! Your new home is closer than you think.

Frequently Asked Questions

Can I get a mortgage if I’ve been self-employed for less than 2 years?

You can secure a mortgage with less than two years of history. While major banks usually demand a full 24-month track record, alternative lenders are more flexible. They often accept 6 to 12 months of self-employment if you have a proven history in the same industry as a previous employee. We focus on your total professional experience to build a strong case for your income stability.

What is the minimum credit score for a self-employed mortgage in Ontario?

A minimum score of 600 is required for at least one borrower to be eligible for CMHC mortgage loan insurance. For the best rates at Big 5 banks, you should aim for 700 or higher. Lower scores are still manageable, but they usually require a move to alternative lending tiers where equity is prioritized over your credit history.

Do I need a larger down payment if I am self-employed?

You don’t always need a larger down payment. If you qualify at an A-lender with standard income proof, you can provide as little as 5% down on the first $500,000. However, if you need the flexibility of a B-lender or an “alt-doc” program, you’ll typically need a 20% down payment. This larger stake offsets the lender’s risk when taxable income is low.

What if I don’t have my most recent Notice of Assessment (NOA)?

Most traditional lenders won’t proceed without your most recent Notice of Assessment. It’s the only way they can verify you don’t have outstanding tax debt to the CRA. If your NOA is delayed or missing, we may need to explore private lending options as a short-term bridge until your tax filings are up to date.

Can I use my business bank statements to prove my income instead of tax returns?

Bank statements are often the most effective way to prove your real income. Many alternative lenders review 6 to 12 months of business statements to verify your actual cash flow rather than just your net profit. This is a primary strategy for how to get a mortgage when self-employed while maintaining a tax-efficient business structure.

Are mortgage rates higher for self-employed individuals in Canada?

Your status as a business owner doesn’t automatically mean higher rates. If you meet the bank’s standard documentation and credit criteria, you get the same market rates as a salaried employee. You only pay a higher rate if your specific financial situation requires the flexibility of a B-lender or a private mortgage solution.

What is a ‘stated income’ mortgage and do they still exist in 2026?

True “no-doc” stated income loans where no verification is required are a thing of the past. In 2026, we use “alt-doc” programs. These allow you to state a reasonable income based on your industry standards, but you must back it up with bank statements or business records. It’s a transparent version of the old model that satisfies modern regulations.

How do lenders view rental income if I’m already self-employed?

Lenders view rental income as a significant asset that boosts your total borrowing power. They typically use a “rental offset” or “add-back” method, recognizing 50% to 80% of the gross rent from your properties. This extra revenue is added to your business earnings, making it easier to qualify for a higher mortgage amount in the GTA.