Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Best Debt Consolidation Options in Ontario: A 2026 Homeowner’s Guide

- Home

- Best Debt Consolidation Options in Ontario: A 2026 Homeowner’s Guide

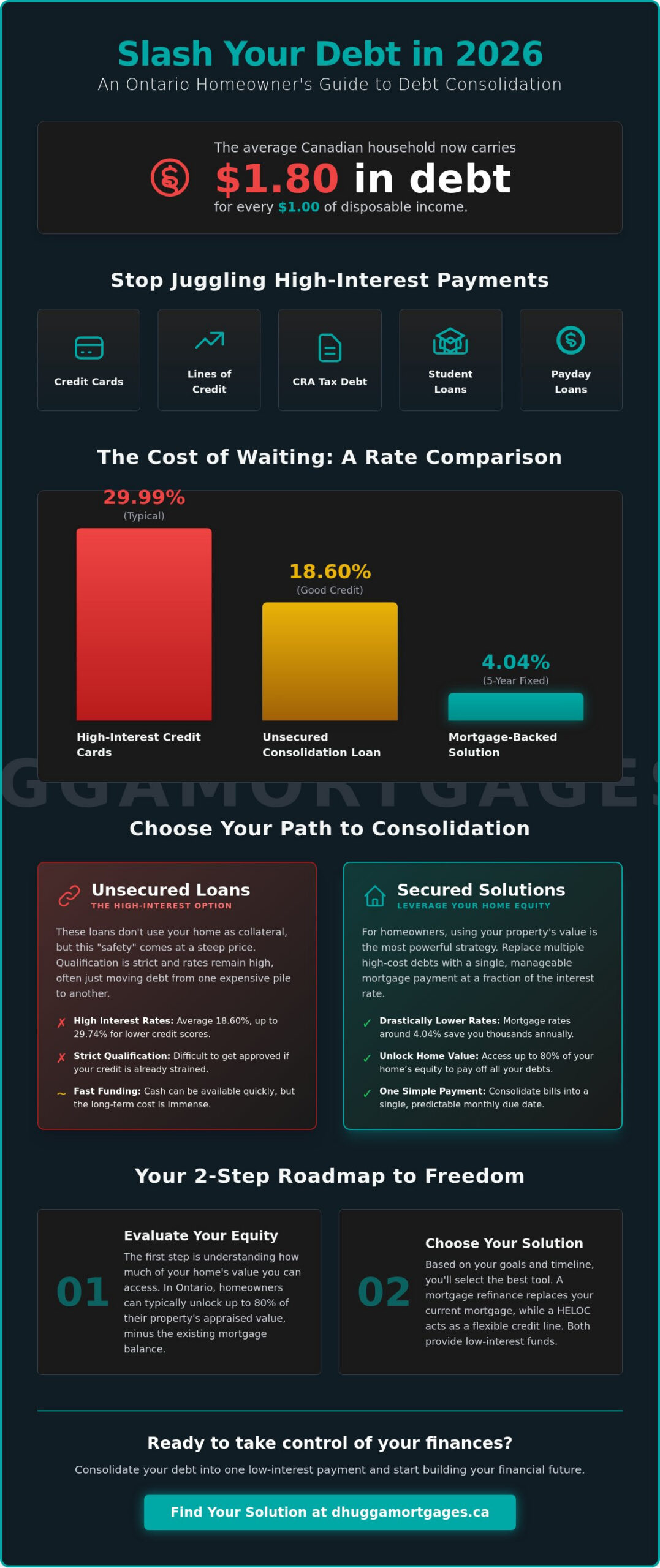

The average Canadian household now carries $1.80 in debt for every dollar of disposable income. It’s a staggering weight. If you’re living in the GTA, you likely feel this pressure every time you check your bank balance. Managing multiple high-interest credit cards is exhausting and expensive. You want relief, but you’re rightfully worried that a consumer proposal will tank your credit score. You deserve a strategy that builds your financial future instead of tearing it down.

You can stop the cycle of endless interest payments today. This guide breaks down the most effective debt consolidation options Ontario homeowners have at their disposal in 2026. We’ll show you exactly how to leverage your home equity to slash your monthly obligations and move toward a debt-free life. You’ll get a direct look at how mortgage refinancing and HELOCs compare to traditional bank loans. We’ll provide the data you need to simplify your bills into one single due date. It’s time to take a proactive step toward peace of mind and financial stability.

Key Takeaways

- Stop losing money to high-interest credit cards. Consolidate your balances into one manageable monthly payment.

- Explore the most effective debt consolidation options Ontario provides to help homeowners leverage their equity.

- Unlock up to 80% of your home’s value. Use strategic mortgage refinancing to drastically reduce your monthly overhead.

- Understand the massive interest rate gap between secured and unsecured debt relief. Find the cheapest path to financial freedom.

- Follow a clear, two-step roadmap. Evaluate your equity and choose a solution that fits your specific timeline.

What is Debt Consolidation and How Does it Work in Ontario?

Debt consolidation isn’t just about moving money around. It’s a strategic move to regain control. In the Ontario real estate market, debt consolidation is the process of using your home equity to replace high-cost consumer debt with a single, lower-interest mortgage-backed solution. You take multiple high-interest debts and roll them into one. It’s simple. It’s effective. The goal is to stop the bleeding from high interest rates and start paying down your principal faster.

To understand the mechanics, we can look at the foundational concept. What is debt consolidation? It’s the act of taking out a new loan to pay off several others. For most Ontario residents, this means escaping credit card rates that often soar above 20%. With the Bank of Canada key rate held steady at 2.25% as of June 2026, those retail bank rates are unnecessarily predatory. By exploring the best debt consolidation options Ontario provides, you can slash your monthly outflows and simplify your life with one single due date.

Why Ontario Homeowners Face Unique Challenges in 2026

Living in the GTA comes with a high price tag. As of early 2026, Canadian consumer debt hit a record $2.66 trillion. Ontario households are feeling the squeeze, with many carrying $1.80 in debt for every dollar of disposable income. In cities like Brampton and Mississauga, home equity has grown significantly, yet the cost of living continues to rise. This creates a paradox where you’re “house rich” but “cash poor.” Ontario’s specific mortgage rules allow you to access up to 80% of your home’s value through mortgage refinancing. This is a massive advantage. It gives you the power to use your property as a tool to eliminate high-interest debt that would otherwise take decades to clear.

Common Debts Ontarians Consolidate

Most homeowners we help are juggling a variety of high-cost obligations. These are the most frequent targets for debt consolidation options Ontario clients choose to tackle:

- High-interest credit card balances: Debt from major Canadian banks or retail cards with rates up to 29.99%.

- Unsecured personal lines of credit: These often have floating rates that have become unpredictable in the current market.

- CRA tax debt: Outstanding balances with the Canada Revenue Agency that carry heavy penalties and interest.

- Provincial student loans: Older loans that still carry significant interest costs.

- Payday loans: Short-term, high-cost loans that create a dangerous cycle of debt.

Consolidating these into a single mortgage-backed payment provides immediate relief. You stop managing five or six different creditors. You start focusing on one clear path to being debt-free. It’s about working smarter, not harder, with your money.

Comparing Debt Consolidation Options in Ontario

Choosing the right path requires a clear look at the numbers. Not all debt consolidation options Ontario lenders offer are created equal. The biggest divide sits between secured and unsecured debt. If you don’t use collateral, you pay for it through higher interest rates. As of June 2026, the average APR for an unsecured consolidation loan for someone with good credit is approximately 18.60%. Compare that to current mortgage rates, where a 5-year fixed rate sits around 4.04%. For homeowners, the choice is usually clear. Using your home as leverage isn’t just a convenience. It’s a strategic move to save thousands in interest costs over the long term.

Speed is another factor to consider. Unsecured loans from high-interest lenders offer fast cash, often within 24 hours. However, the long-term cost of borrowing can be 20% to 30% higher than a mortgage-backed solution. You need to decide if immediate funding is worth the massive interest premium. Reviewing the Government of Canada debt consolidation options can help you understand these basic structures before you commit to a specific lender.

Unsecured Consolidation Loans

Personal loans from major banks are the most common unsecured route. They don’t require your home as collateral, which feels safer to some. The reality is different. Qualification is strict. If your credit score is below 580, you could face interest rates as high as 29.74%. These loans are often a last resort because they don’t solve the underlying interest rate problem for most GTA homeowners. They simply move the debt from one high-interest bucket to another.

Credit Counselling and Debt Management Plans

Non-profit organizations like Credit Canada offer debt management plans. These are helpful if you’re truly struggling to make even minimum payments. There’s a catch. These programs often result in a “note” on your credit report, similar to a consumer proposal. This can make it difficult to renew your mortgage or get new credit for several years. While they lower your monthly payment, they don’t provide the same wealth-building benefits as restructuring your debt through your home.

Mortgage-Based Consolidation (The Strategic Play)

This is where homeowners gain the “edge.” By using your property as collateral, you access prime interest rates that are impossible to get elsewhere. You can choose a total refinance or a second mortgage to clear your high-interest balances. This move protects your credit score and puts more money back in your pocket every month. If you want to understand the full mechanics, read our debt consolidation mortgage Canada guide. It’s the most efficient way to turn high-interest debt into low-interest home equity. If you’re ready to see your specific numbers, you can speak with our team today to explore your local options.

Strategic Mortgage Tools for Consolidating Debt

Your home is a massive financial asset. It’s time to use it. When looking for the best debt consolidation options Ontario offers, mortgage-backed tools stand out for their efficiency. You have three primary paths: refinancing, HELOCs, or second mortgages. Each serves a specific purpose depending on your current mortgage rate and credit health. These tools allow you to stop being “house rich and cash poor” by turning your equity into a low-interest debt-clearing machine.

Refinancing to Consolidate Credit Card Debt

Refinancing your primary mortgage allows you to unlock up to 80% of your home’s appraised value. This is a game-changer for anyone carrying five-figure credit card balances. You can consolidate credit card debt with mortgage rates that are a fraction of what retail banks charge for plastic. Even with a prepayment penalty, the long-term savings are often substantial. You stop paying 20% interest and start paying 4%. The math is simple. The results are immediate. You need to calculate your “break-even” point to ensure the interest savings outweigh the cost of breaking your current term.

HELOC vs. Home Equity Loans

A Home Equity Line of Credit (HELOC) offers flexibility. It’s a revolving credit line where you only pay interest on what you use. This is perfect for ongoing debt management. However, if you need a one-time lump sum to clear everything at once, you should consider a home equity loan for debt consolidation. It provides a fixed repayment schedule and a clear end date. This ensures you actually pay off the principal instead of just treading water with interest-only payments. It’s about discipline and a structured path to freedom.

Solutions for Bad Credit and Self-Employed Individuals

Don’t let a low credit score stop your progress. Many Ontario homeowners believe they’re stuck because of past financial hurdles or non-traditional income. Private lenders operate differently. They focus on the equity in your property rather than just your Equifax report. This is a vital bad credit debt consolidation mortgage strategy. It’s also ideal for business owners who need to separate personal and corporate debt. Private mortgages provide a bridge. They clear your high-interest debt, improve your credit score, and eventually allow you to move back to a prime lender at a lower rate.

If you have a very low interest rate on your first mortgage, don’t break it. A second mortgage allows you to access equity without losing your current 2% or 3% rate. It’s a tactical move. It protects your existing low-cost debt while providing the cash needed to eliminate credit card balances. Every situation is unique. The key is to act quickly to stop the interest from compounding and start building real wealth again.

How to Choose the Right Option for Your Situation

Selecting from the available debt consolidation options Ontario residents have requires a methodical approach. Don’t guess. Run the numbers. Finding the right solution depends on your current debt load, your home’s value, and your long-term financial goals. Follow this five-step process to identify your best path to a debt-free life.

- Step 1: Calculate your weighted average interest rate. List every credit card, personal loan, and line of credit. If your average rate is 18% and a mortgage refinance is 4.04%, the savings are massive.

- Step 2: Determine your usable home equity. Take your home’s current market value and multiply it by 0.80. Subtract your existing mortgage balance. This is the maximum amount you can typically access for consolidation.

- Step 3: Check your credit tier. Your credit score dictates your interest rate. In 2026, borrowers with scores above 740 access the best prime rates, while those below 600 may need to look at private mortgage solutions.

- Step 4: Contrast savings with costs. Compare your new monthly payment against your current total. Factor in legal fees and appraisal costs. If you save $500 a month, a $2,000 implementation cost pays for itself in just four months.

- Step 5: Get professional verification. Consult a Brampton-based mortgage expert to run the final numbers. We see GTA-specific files every day and can spot opportunities local banks often miss.

The ‘Penalty vs. Savings’ Math

Refinancing often involves breaking your current mortgage term. This comes with a cost. You must decide if the penalty is worth the interest savings. Banks often push high-fee unsecured loans to keep you from breaking your mortgage. Don’t fall for it. In 2026, fixed-rate mortgage penalties are typically calculated as the greater of three months’ interest or the interest rate differential (IRD) based on current market rates. If you’re consolidating $50,000 of 20% credit card debt, paying a $3,000 mortgage penalty is a strategic win that saves you tens of thousands in the long run.

Timing the Ontario Market

Timing is everything. With total Canadian consumer debt reaching $2.66 trillion in 2026, the pressure on households is at an all-time high. Waiting too long to consolidate can be dangerous. If your debt grows faster than your home value, your equity-to-debt ratio erodes. This makes it harder to qualify for prime rates later. GTA home values remain stable for now. Act while you have the equity to secure a low-interest rate and lock in your monthly savings. You can contact our Brampton office today to get a custom analysis of your equity.

Why Dhugga Mortgages is Your Ontario Consolidation Partner

We don’t just provide mortgages. We deliver financial breakthroughs. When you explore debt consolidation options Ontario, you need more than a list of rates. You need a partner who understands the local landscape. We know the Brampton, Mississauga, and Toronto markets inside and out. We understand the specific pressures of living in the GTA. Our team specializes in complex files that big banks often ignore. Whether you are self-employed, a newcomer to Canada, or dealing with bruised credit, we find the path to “yes.”

Our advantage is our network. We have access to a broad range of prime and private lenders across the province. This means we aren’t limited to a single suite of products. We shop the market to find the most strategic fit for your equity. We are proactive. We are results-oriented. We value your time above all else. Our role is to act as your high-energy facilitator, taking charge of the process and removing every bit of unnecessary complexity. You get the professional expertise of a seasoned local leader with the approachability of a helpful neighbour.

Fast Approvals and Streamlined Processes

Speed is our signature. We move from application to funding faster than the big banks. We’ve removed the friction from the consolidation process. Our communication is direct and punchy. You won’t find flowery language or confusing jargon here. We tell you exactly what you need to know and what the next steps are. This transparency builds trust. Our history of helping Ontario families find financial peace is built on this foundation of efficiency. We prioritize your results so you can stop worrying about high-interest payments and start focusing on your family’s future.

Get Started Today

Waiting is the most expensive choice you can make. Every day spent at a high interest rate is equity leaving your pocket. We offer a no-obligation debt assessment to help you see the possibilities. Our customized consolidation plans are built for your specific life stage and financial goals. We run the math to ensure your new plan provides immediate relief and a clear end date for your debt. It is time to take a bold, action-oriented step toward your freedom. Secure your financial future with a Dhugga Mortgages debt consolidation plan today.

Secure Your Financial Freedom Today

You now have the roadmap to eliminate high-interest debt and reclaim your monthly cash flow. Using your home equity is the most efficient way to slash interest rates and simplify your life with one single payment. Whether you choose a full refinance or a strategic second mortgage, the objective is clear. Stop the interest bleed and start building real wealth again. You’ve explored the most effective debt consolidation options Ontario provides for homeowners in 2026.

As an expert mortgage brokerage serving the GTA, Dhugga Mortgages delivers the speed and reliability you need. We offer specialized solutions for private and second mortgages with direct access to over 50 lending partners. We take charge of the process so you don’t have to. Don’t let multiple due dates and rising costs hold you back any longer. Take control of your debt now with a tailored Ontario consolidation strategy.

Your path to a debt-free future starts with one proactive decision. We are ready to help you make it happen quickly.

Frequently Asked Questions

Is debt consolidation a good idea for Ontario homeowners?

Yes. It’s a strategic move when your consumer debt interest exceeds current mortgage rates. You use your home’s value to replace high-cost credit cards with a low-interest solution. This is one of the top debt consolidation options Ontario residents choose to increase their monthly cash flow. It’s about working smarter with the equity you’ve already built in your property to stop wasting money on interest.

How much home equity do I need to consolidate my debt in Ontario?

You can typically access up to 80% of your home’s appraised value. To find your limit, multiply your home’s current market price by 0.80 and subtract your current mortgage balance. The result is the maximum amount available for consolidation. If you have significant equity in a GTA home, you likely have more than enough room to clear your high-interest debts and simplify your finances.

Will debt consolidation hurt my credit score?

It typically helps your credit score over the long term. When you pay off multiple credit cards, your credit utilization ratio drops significantly. This is a primary factor in Canadian credit scoring models. You replace high-risk revolving debt with a stable, amortized mortgage payment. This shift shows lenders you’re managing your finances proactively and reduces your overall credit risk profile in the eyes of the bureaus.

Can I consolidate my debt if I have a bad credit score in Ontario?

Yes. You can still consolidate with a low credit score by looking beyond traditional banks. Private lenders in Ontario focus on your home’s equity and location rather than just your credit history. This provides a vital bridge. You clear the high-interest debt that’s dragging your score down, which allows you to rebuild your credit and eventually return to a prime lender at a lower rate.

What is the difference between debt consolidation and a consumer proposal?

Consolidation is a loan that pays your creditors in full, while a consumer proposal is an insolvency process where you negotiate to pay back only a portion. Proposals severely damage your credit report for up to three years after completion. Consolidation is a proactive financial tool that keeps your credit intact. It’s the preferred choice for homeowners who want to maintain their future borrowing power and financial reputation.

How long does the debt consolidation process take through a mortgage broker?

Our process is designed for speed and efficiency. We can often secure an initial approval within 24 to 48 hours of receiving your application. The full process, including the appraisal and legal work, usually takes about two to three weeks. This is significantly faster than the big banks, which can often take over a month to process similar consolidation requests for Ontario homeowners.

Can I consolidate CRA tax debt into my Ontario mortgage?

Yes. Consolidating CRA tax debt into a mortgage is a common strategy for Ontario homeowners. The Canada Revenue Agency charges high interest and penalties on overdue balances. By rolling this debt into your mortgage, you stop the penalties and protect your home from potential liens. It’s an efficient way to resolve tax issues while keeping your monthly payments low and predictable within your household budget.

What are the fees associated with debt consolidation in Ontario?

You should account for appraisal fees, legal costs, and potential mortgage prepayment penalties. These are standard when exploring debt consolidation options Ontario homeowners use to restructure their finances. Fees depend on your specific situation and current mortgage terms. We prioritize transparency and will outline every cost before you commit. Most clients choose to roll these expenses into the new mortgage amount to avoid paying out of pocket.