Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

HELOC vs. Second Mortgage: Which Home Equity Option Wins in 2026?

- Home

- HELOC vs. Second Mortgage: Which Home Equity Option Wins in 2026?

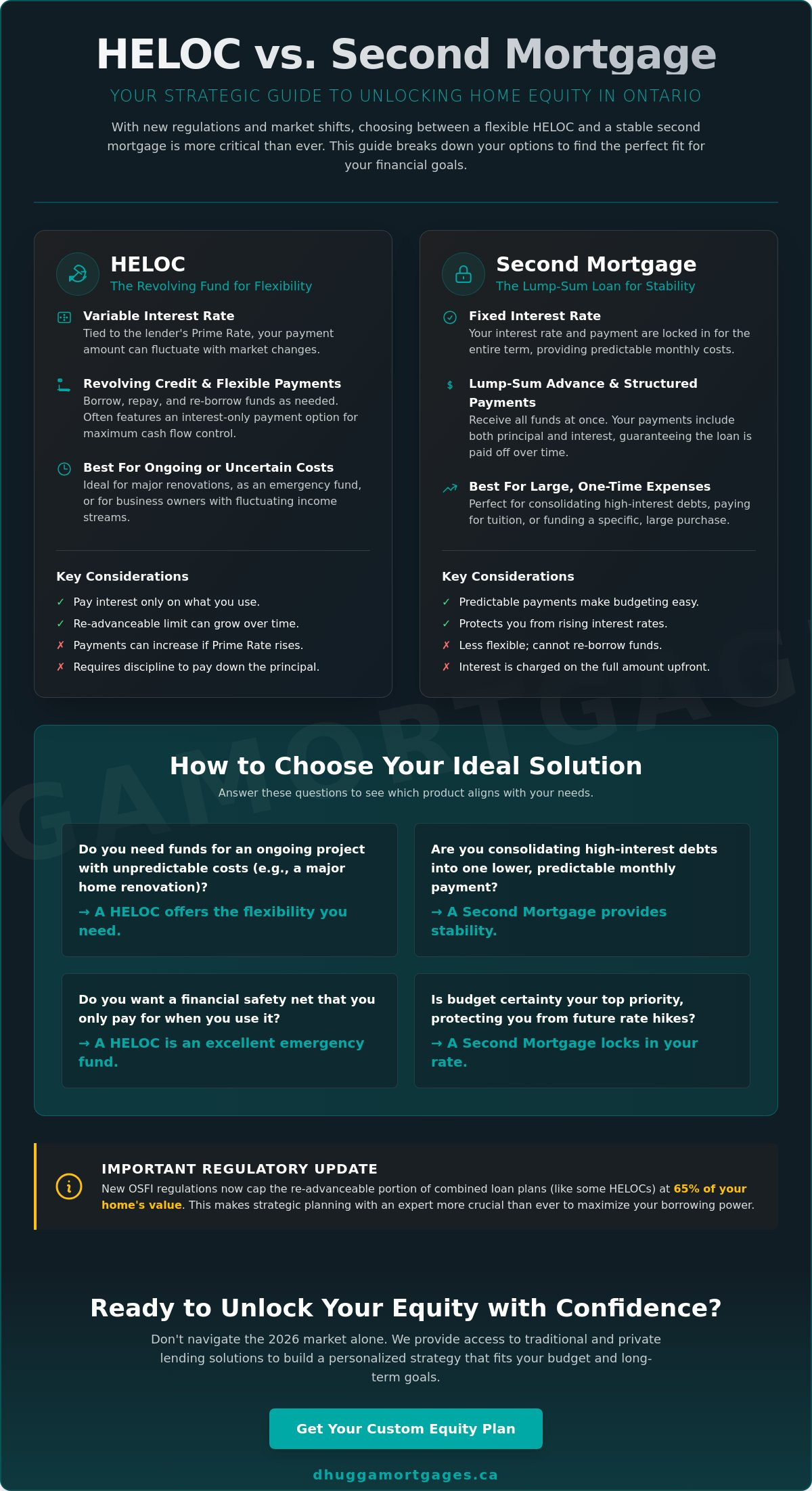

The lowest interest rate on your home equity isn’t always the cheapest path to debt freedom. You likely feel the pressure of rising interest rate uncertainty in 2026 while trying to manage high monthly debt payments. It is a frustrating spot to be in. New OSFI regulations now cap re-advanceable limits at 65% of your home’s value, making the HELOC vs second mortgage decision more complex than ever. You need an expert guide to cut through the noise and find a solution that fits your budget.

We are here to help you unlock your home equity with total confidence. This article provides the clarity you need to lower your monthly interest costs and secure a flexible source of funds. We will compare current 5-year fixed rates against variable lines of credit, explain the latest LTV restrictions, and show you exactly how to qualify under the 2026 stress test. Get the facts. Take control of your finances today.

Key Takeaways

- Calculate your usable equity in the GTA to unlock maximum borrowing power and financial freedom.

- Master the revolving nature of a HELOC to ensure you only pay interest on the funds you actually use.

- Identify why a fixed-rate second mortgage offers superior stability for long-term debt consolidation during market shifts.

- Compare a HELOC vs second mortgage to find the perfect balance between variable flexibility and fixed certainty.

- Access private lending solutions and specialized products that go far beyond standard big bank offerings.

Understanding Home Equity in Ontario: Why Borrow Now?

Home equity is your most powerful financial tool. It is the simple difference between your property’s current market value and the total of all debts registered against it. For a foundational look at these concepts, you can review Wikipedia’s explanation of home equity loans. In 2026, homeowners in Brampton and Toronto are sitting on record levels of equity. Even with market shifts, property values in the GTA remain a massive source of untapped wealth. You’ve worked hard for your home; now it is time to make that value work for you.

Canadian regulators enforce a strict 80% Loan-to-Value (LTV) rule. This means your combined mortgage and equity loans cannot exceed 80% of your home’s appraised value. Whether you want to fund a major renovation, cover university tuition, or consolidate high-interest credit card debt, your equity is the key. Deciding between a HELOC vs second mortgage is the first step toward a smarter financial future. It’s about finding the right fit for your monthly cash flow and long-term goals.

The 2026 Ontario Real Estate Context

Price stability in Mississauga and Caledon has created a unique opportunity for borrowers. While the explosive growth of previous years has leveled off, the “Appraisal Gap” is a real factor. This gap occurs when your perceived home value differs from what a professional appraiser sees. A current, professional valuation is mandatory in 2026. Lenders are more cautious now. They want to see exactly what the collateral is worth before approving any funds. The current interest rate environment means you need a precise strategy to avoid overpaying on your borrowing costs.

Why Traditional Refinancing Might Not Be the Answer

Breaking your first mortgage is often a mistake. If you secured a low rate years ago, the penalties to refinance can be staggering. You don’t want to lose a low interest rate just to access some cash. This is where equity products shine. You can leave your existing first mortgage alone and simply layer a new product on top. It’s a faster, more efficient way to get the capital you need without the heavy bank fees. If you’re looking to use this equity to help a family member enter the market, our First Time Home Buyer Mortgage Ontario guide can show you how to leverage your success into their new home. Accessing cash shouldn’t mean starting over from scratch.

The HELOC Advantage: Flexibility and Control for GTA Homeowners

A Home Equity Line of Credit (HELOC) is a revolving credit facility. It works much like a high-limit credit card secured by your property. This is a powerful tool for GTA homeowners who value liquidity. The biggest draw is the “pay for what you use” model. If you have a $100,000 limit but only spend $10,000 on home repairs, you only owe interest on that $10,000. It is efficient. It is direct. It puts you in total control of your debt. When comparing a HELOC vs second mortgage, this revolving nature is a massive differentiator.

The interest rate on a HELOC is variable. It is tied directly to the lender’s Prime Rate. This means your monthly costs can fluctuate as the market moves. However, the flexibility of interest-only payments is a major benefit for cash flow management. You aren’t forced to pay down the principal every month. You can choose to pay only the interest, keeping your mandatory monthly obligations at a minimum. This is ideal for homeowners with fluctuating incomes or those who want to maximize their monthly budget. If you want to see how this fits your current budget, reach out to our team for a personalized assessment.

How the HELOC Draw Period Works

The draw period is your window of accessibility. During this time, you can withdraw funds, pay them back, and withdraw them again. Accessing your money is simple. You can use specialized cheques, set up online transfers, or use a linked debit card. Many Toronto homeowners use a HELOC as a robust emergency fund. You don’t pay a cent until you actually use the money. It provides a safety net without the immediate cost of a lump-sum loan. It is there when you need it and costs nothing when you don’t.

Pros and Cons of a Revolving Line

The benefits are clear. You get low initial payments and total control over your borrowing. Many HELOCs in 2026 feature re-advanceable components. As you pay down your first mortgage principal, your available credit limit grows automatically. It is a self-expanding financial resource. But there are risks. Variable rates mean your costs could rise if the Prime Rate climbs. There is also the risk of “persistent” balances where you never actually reduce the debt. Understanding the risks of second mortgages and lines of credit is essential. Lenders can also “call” the loan or freeze the limit if property values in Mississauga or Brampton drop significantly. You need a proactive strategy to manage these variables effectively.

Second Mortgages: Fixed Stability and Private Lending Solutions

A second mortgage is a one-time lump sum loan. It sits behind your first mortgage on the property title. Unlike a line of credit, you receive the entire amount upfront. This provides immediate liquidity for major expenses. Most second mortgage products feature a fixed interest rate. This means your payment stays the same every single month. No surprises. No market-driven spikes. For many homeowners, this predictability is the ultimate goal. When weighing the HELOC vs second mortgage debate, stability often wins for those on a strict monthly budget.

Mississauga homeowners frequently choose this path for structured debt consolidation. You take your high-interest credit cards and roll them into one manageable payment. It is a clean, decisive move toward debt freedom. You can find more detailed comparisons on HELOC Vs. Home Equity Loan options to see which structure matches your risk tolerance. Choosing between a HELOC vs second mortgage depends on whether you value ongoing access or a one-time injection of cash.

Lump Sum Funding vs. Revolving Credit

Large, fixed-cost projects require certainty. If you are finishing a basement or paying a flat tuition fee, a lump sum makes sense. You get the cash. You pay the bill. You start the repayment. There is a significant psychological benefit to a set repayment schedule. You know exactly when the loan will be paid off. A second mortgage is registered on your property title, just like your first. It is a formal, transparent agreement that protects both you and the lender. It is about commitment and a clear path to zero balance.

Private Second Mortgages in Brampton and Caledon

The big banks often say no. They have rigid boxes that don’t fit everyone. If you are self-employed, have non-traditional income, or are recovering from a bruised credit score, private lenders are the answer. This is where we excel. Private second mortgages in Brampton and Caledon focus more on your home’s equity than your tax returns. These solutions usually have shorter terms, typically one to two years. They serve as a bridge. They give you the capital you need today while you improve your credit or wait for a traditional bank refinance.

Dhugga Mortgages has deep roots in the Ontario private lender network. We act fast. We find the edge you need to secure funding when others walk away. We handle the complexity so you can focus on your goals. Private lending isn’t a last resort; it’s a strategic tool for savvy homeowners. Don’t let a no from a bank stop your progress. Move forward with a partner who understands the local market and delivers results quickly.

HELOC vs. Second Mortgage: Which One Wins Your Situation?

Choosing between a HELOC vs second mortgage isn’t about finding a superior product. It’s about matching a financial tool to your specific 2026 goals. A HELOC offers a variable rate tied to the Prime Rate. It provides the flexibility of interest-only payments. A second mortgage delivers a fixed rate with a structured principal and interest repayment schedule. One gives you a safety net. The other gives you a finish line. You must decide if you value ongoing access to cash or the certainty of a closed loan.

Repayment structures create the biggest impact on your monthly budget. With a HELOC, your minimum payment can stay very low. This is helpful when cash flow is tight. However, a second mortgage forces you to pay down the balance from day one. It is a disciplined approach. If you want to see which structure fits your household income, contact our team for a custom quote. We can run the numbers for both options in minutes.

The “Winner” by Scenario

- Renovations with uncertain costs: The HELOC wins. Contractors often find surprises. You only draw what you need as the project evolves.

- Consolidating $50,000 in credit card debt: The Second Mortgage wins. You need a structured path to zero. Revolving credit can be a trap if you only pay the minimum.

- Investing in a new business: It depends on the ROI. Compare your expected business returns against the fixed cost of a second mortgage to ensure the math makes sense.

Qualification Requirements in 2026

Qualification hurdles have shifted. For A-lenders in Ontario, a credit score of 680 is the standard benchmark. Scores above 720 typically unlock the most competitive rates. The Mortgage Stress Test remains a major factor for HELOC applications. You must prove you can handle payments at the contract rate plus 2%, or a floor rate of approximately 5.25%, whichever is higher. This often reduces the total amount you can borrow compared to a second mortgage.

Debt-to-income ratios are also calculated differently. Banks look at your total debt load with a critical eye. Private second mortgages are more lenient. They focus heavily on the equity in your home rather than just your tax returns. This makes equity-based lending a faster route for self-employed individuals or those with non-traditional income streams. We specialize in finding the edge where your equity carries more weight than a computer-generated credit score.

Strategic Equity Planning with Dhugga Mortgages

Expert advice is the difference between a debt trap and a wealth-building strategy. Tapping into your home’s value is a major financial decision that requires a professional lens. Determining the winner in the HELOC vs second mortgage debate requires a look at your total financial picture. We don’t just look at rates. We look at your five-year plan. Most homeowners go straight to their local bank branch. This is a mistake. The “Big Five” banks only sell their own products. They won’t tell you if a private lender offers a more flexible term or a lower qualifying threshold. We give you the full view.

Our team provides the “Efficiency Advantage” in the competitive GTA market. We know Brampton, Mississauga, and Toronto property values better than anyone. We move fast because we know your time is valuable. The HELOC vs second mortgage choice is easier when you see the numbers side-by-side in a clear, digestible format. We remove the complexity. We handle the paperwork. You get the results you need to move forward with your life. Speed is our currency. Reliability is our promise.

The Dhugga Mortgages Process

- Step 1: Free equity assessment and goal alignment. We start by defining exactly what you need. Is it cash for a renovation or a clean slate through debt consolidation? We verify your usable equity and set a clear target.

- Step 2: Comparison of bank products vs. private equity solutions. We scan the entire market. We compare standard bank HELOCs against specialized second mortgages from our private lender network. You see every available option.

- Step 3: Rapid approval and streamlined closing process. Once you choose your path, we push for speed. Our established relationships with lenders mean faster turnarounds and fewer hurdles for you.

Ready to Realize Your Home Advantage?

Jaspreet Dhugga brings a results-oriented approach to every client in Brampton and beyond. We are proactive partners in your success. We don’t wait for things to happen; we make them happen. If you are a senior homeowner looking to stay in your home while accessing funds, you should also consider a Reverse Mortgage Canada as a powerful alternative. It might be the strategic edge you need for a comfortable retirement. Stop guessing about your financial future. Get the facts today. Book a consultation to see your specific numbers and take the first step toward debt freedom.

Take Control of Your Home Equity Now

You have the data to make a confident decision. The 2026 market requires a sharp strategy to navigate new LTV caps and stress test requirements. Whether you value the revolving flexibility of a line of credit or the fixed-rate stability of a lump sum loan, your home is your strongest asset. Finding the right fit in the HELOC vs second mortgage debate is about more than just interest rates; it’s about your long-term peace of mind. You deserve a plan that protects your cash flow while clearing your debt.

Don’t settle for the limited options at a single bank branch. Jaspreet Dhugga and our expert team provide access to over 50 Canadian lenders, specializing in private and alternative mortgage solutions. We move at the speed of the GTA market to ensure you get the best possible terms. Get Your Free Equity Assessment from Dhugga Mortgages Today. Your path to lower monthly payments and financial freedom starts with a single click. We are ready to help you succeed. Let’s make your home equity work for you today.

Frequently Asked Questions

Can I have both a HELOC and a second mortgage at the same time?

Yes, you can have both. It is possible to layer multiple equity products as long as your total debt stays at or below 80% of the home’s appraised value. This combined approach is a common tactic when comparing a HELOC vs second mortgage for different needs. You might use the loan for a major renovation and the line of credit for ongoing emergency access. We can help you structure these products to maximize your borrowing power while keeping your first mortgage intact.

Does a HELOC or a second mortgage affect my credit score more?

A HELOC often has a more immediate impact on your credit score because it is a revolving trade-line. High utilization on your line of credit can lower your score, similar to a maxed-out credit card. A second mortgage is an installment loan. It shows a steady repayment history and doesn’t affect your credit utilization ratio in the same way. Both require on-time payments to maintain a healthy credit profile in the Ontario market.

How much equity do I need to qualify for a second mortgage in Ontario?

You generally need at least 20% equity in your home to qualify for a second mortgage in Ontario. This ensures the total debt against your property doesn’t exceed 80% of its market value. If you live in a high-demand area like Brampton or Mississauga, your equity might be higher than you realize due to local appreciation. We verify your available equity through a professional appraisal process to ensure accuracy for the lender.

Are interest rates for second mortgages higher than HELOCs in 2026?

Interest rates for second mortgages are generally higher than HELOC rates. This is because the second lender takes more risk by being second in line for payment if you default. When deciding between a HELOC vs second mortgage, you must weigh the lower initial variable rate of the line of credit against the fixed certainty of the loan. One offers a lower entry cost; the other offers a guaranteed monthly payment that won’t change if the Prime Rate climbs.

Can I use a HELOC to pay off my primary mortgage?

You can use a HELOC to pay down or pay off your primary mortgage, but it is a strategic move that requires caution. Converting a low-rate first mortgage into a variable-rate line of credit exposes you to interest rate hikes. This is often done by homeowners using specialized strategies to make their mortgage interest tax-deductible through investment. It’s a bold move that works best for those with high risk tolerance and a clear repayment plan.

What happens to my HELOC if property values in Toronto drop?

If property values in Toronto drop significantly, your lender has the right to freeze your HELOC or reduce your credit limit. This is the “callable” nature of a revolving line. It happened during previous market corrections and remains a risk in 2026. A second mortgage is a closed loan. Once the funds are advanced, the lender cannot take them back or change the terms as long as you make your payments on time.

Is the interest on a second mortgage tax-deductible in Canada?

Interest is only tax-deductible in Canada if the borrowed funds are used to earn income. This applies to both products. If you use the money for a rental property or dividend-paying stocks, the interest is usually deductible. If you use it for home renovations or personal debt consolidation, it is not. You should keep a clear paper trail for the CRA to prove exactly how the funds were utilized.

How long does it take to get approved for an equity loan in Brampton?

Approval times vary by lender type. Private lenders in Brampton can often provide a commitment letter within 24 to 48 hours. Traditional banks take much longer, often two to three weeks, due to stricter stress test requirements and internal red tape. We prioritize speed and aim to get your funds registered as quickly as the legal process allows. Our team handles the heavy lifting to ensure a streamlined closing.