Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Commercial Mortgage Broker Ontario: Secure Your Business Growth in 2026

- Home

- Commercial Mortgage Broker Ontario: Secure Your Business Growth in 2026

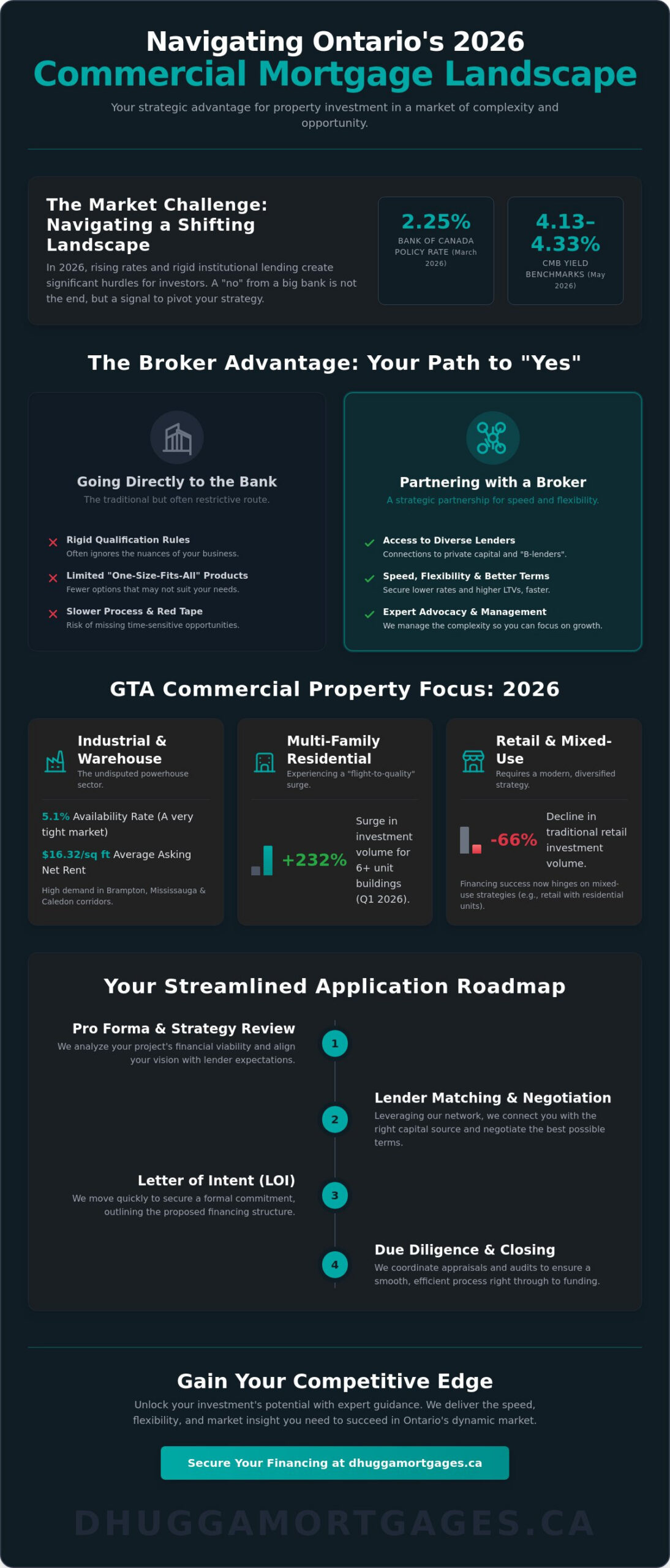

In 2026, a “no” from a Big 5 bank isn’t a dead end for your property investment. It’s a signal that your strategy needs a professional pivot. You’ve likely felt the friction of the 2.25% Bank of Canada policy rate and the tightening qualification rules that make traditional lending feel like a closed door. It’s frustrating to watch prime opportunities in the GTA industrial or multi-family sectors slip away because of rigid institutional red tape. You need speed. You need a path around the complexity.

Partnering with a dedicated commercial mortgage broker Ontario gives you the strategic edge to bypass these hurdles. We help you secure lower interest rates and higher Loan-to-Value ratios by connecting you with flexible private capital and specialized lenders. You’ll learn how to navigate the current CMB yield benchmarks of 4.13% to 4.33% and streamline complex environmental audits for faster closings. We’ll examine why multi-family investment volume jumped 232% this year and how you can capitalize on that momentum. This article provides the blueprint to scale your portfolio despite the shifting regulatory landscape. Let’s get to work.

Key Takeaways

- Identify why 2026 market volatility requires a strategic approach to secure the best rates and overcome institutional hurdles.

- Discover tailored financing structures for high-growth industrial hubs in Brampton and mixed-use developments across the GTA.

- Navigate the critical differences between Big 5 banks and flexible private lenders by consulting an experienced commercial mortgage broker Ontario.

- Follow a clear, multi-phase application roadmap designed to move your project from pro forma review to a signed Letter of Intent quickly.

- Gain a competitive edge through local expertise that prioritizes speed and deal certainty for your next property investment.

The Strategic Role of a Commercial Mortgage Broker in Ontario’s 2026 Market

A commercial mortgage broker is the strategic architect of your business capital. In a market where the Bank of Canada policy rate sits at 2.25% as of March 2026, every decimal point matters. Residential mortgages focus on your personal income; commercial mortgages focus on the property’s ability to generate cash flow. This distinction is vital. A professional commercial mortgage broker Ontario translates your business vision into a language lenders respect. We don’t just submit papers. We advocate for your growth during the underwriting process to ensure your project doesn’t get buried in a pile of “maybe” files. The role of a commercial mortgage broker involves more than just finding a rate; it’s about structuring a deal that survives the scrutiny of a 2026 credit committee. They bridge the gap between your balance sheet and a lender’s risk appetite.

Navigating the 2026 Ontario Lending Landscape

Shifting interest rates directly impact your Debt-Service Coverage Ratio (DSCR). If your debt costs rise, your property’s perceived value might drop in the eyes of a conservative lender. With Canadian Mortgage Bond yields between 4.13% and 4.33% in May 2026, you need precision. High-growth zones like Brampton and Mississauga remain competitive, especially in the industrial sector where availability rates are a tight 5.1%. Local market knowledge is your best defense against low appraisals. We understand why a warehouse in the Caledon corridor is valued differently than a retail storefront in the downtown core. This specific insight ensures your pro forma reflects reality, not just optimistic projections. We help you realize the full potential of your investment by aligning your debt structure with current market velocity.

The Broker Advantage vs. Going Directly to the Bank

Don’t get stuck in the “one-size-fits-all” trap of big institutional lenders. Major banks have rigid qualification rules that often ignore the nuances of a growing business. We provide a shortcut to “B-lenders” and private funds that aren’t available to the general public. These sources offer the speed and flexibility needed for “outside the box” deals that traditional banks might reject. You save time by letting us manage the complex document flow. We handle the coordination of environmental audits and commercial appraisals while you focus on running your company. Efficiency is our priority. We move fast so you don’t miss out on a $3.8 billion GTA investment market that demands quick action. By choosing a commercial mortgage broker Ontario, you ensure you have the edge in a bifurcated market where multi-family and industrial sectors are performing at record levels.

Commercial Property Types and Financing Structures in the GTA

The GTA commercial landscape is highly segmented in 2026. Success depends on knowing which asset classes lenders currently favour. Industrial and warehouse spaces remain the undisputed powerhouses of the Caledon and Brampton corridors. With availability rates sitting at a lean 5.1% in early 2026, these properties represent low risk for institutional and private capital alike. Average asking net rents of $16.32 per square foot provide the stable cash flow lenders demand. If you’re looking to acquire or refinance these assets, a commercial mortgage broker Ontario can leverage this high demand to secure more aggressive terms.

Multi-family residential is another high-performance sector. Investment volume for buildings with 6+ units surged by 232% in Q1 2026. This “flight-to-quality” trend means Toronto apartment blocks are seeing massive interest. Conversely, the retail sector experienced a 66% decline in investment. Financing retail now requires a mixed-use strategy. Combining storefronts with residential units above creates the stability needed to satisfy modern underwriting criteria. Special use facilities like gas stations, car washes, and hospitality require even more specialized handling. These deals often hinge on the operator’s track record as much as the real estate itself.

Understanding Loan-to-Value (LTV) and Debt-Service Ratios

Your Loan-to-Value ratio isn’t just a number. It’s a reflection of property risk. Industrial assets often command higher LTVs because they’re easier to liquidate and maintain high occupancy. Vacant land, however, typically requires a much larger down payment because it doesn’t generate immediate income. To qualify in 2026, you must accurately calculate your Debt-Service Coverage Ratio (DSCR). Lenders want to see that your net operating income comfortably exceeds your debt obligations. All professional interactions and disclosures are governed by Ontario’s Mortgage Brokerages, Lenders and Administrators Act, which ensures your interests are protected throughout this calculation process. If you’re unsure how your current pro forma stacks up, you can reach out to our team for a quick assessment of your numbers.

Construction and Development Financing

Securing land assembly loans is the first step for future GTA developments. These are complex deals that require a clear path to rezoning and site plan approval. Construction financing typically operates through a draw mortgage system. You receive funds in stages as work is completed and verified by third-party inspectors. Many developers prefer interest-only options during the build phase to preserve cash flow. Once the project is complete and stabilized, we help you transition from high-interest construction debt into permanent commercial mortgage broker Ontario solutions with lower, long-term rates. This seamless transition is critical for maintaining project profitability in a cautious 2026 market.

Institutional vs. Private Lenders: Choosing Your Capital Source

Choosing between a bank and a private fund is a strategic fork in the road. It isn’t just about the interest rate. It’s about your timeline, your documentation, and your long-term growth plan. In the 2026 Ontario market, the gap between these two capital sources has widened. Tier 1 lenders, including the Big 5 banks, offer the lowest rates for stabilized properties. They’re the right choice if you have a pristine credit history and AAA tenants with long-term leases. However, their qualification rules are the most stringent. If your business doesn’t fit their rigid box, you need a different path. An experienced commercial mortgage broker Ontario acts as your guide, determining which lender’s appetite matches your specific deal profile.

Credit unions offer a vital middle ground in the Ontario landscape. They provide more localized decision-making than national banks. Often, they’re more willing to look at the character of the borrower and the specific community impact of a project. The Ontario Mortgage and Housing Corporation Act establishes the legal framework that supports this diverse lending environment. Whether you’re targeting institutional funds or local credit union capital, the goal remains the same: secure the most favourable terms for your equity.

When to Opt for Institutional Lending

Institutional lending is ideal for investors with deep financial records and stabilized assets. If you’re financing a multi-family building with 6+ units, CMHC-insured commercial financing is often the gold standard. It provides lower rates and longer amortization periods. The trade-off is the timeline. These applications require extensive audits and can take months to close. You must have your financial house in order. Banks will scrutinize every detail of your debt-service history. If you have the time and the paperwork, the savings on a 5-year fixed rate are significant.

The Private Lending Edge for GTA Business Owners

Private capital is the engine of the GTA real estate market. It’s built for speed. If you’re self-employed or have unstated income, traditional banks might view you as a high risk. Private lenders prioritize equity and property value over tax returns. Using a private mortgage serves as a powerful short-term tool. It allows you to secure a property quickly, renovate, or stabilize the tenant base before moving to a lower-rate institutional lender later. Approvals happen in days, not weeks. This agility is essential in a market where prime industrial or multi-family assets move fast. A commercial mortgage broker Ontario ensures you don’t overpay for this convenience by shopping your deal across a network of vetted private funds.

The Commercial Mortgage Application Roadmap: From Pro Forma to Closing

Closing a deal in Ontario isn’t a mystery. It’s a sequence of precise steps. In a cautious 2026 market, lenders don’t have patience for incomplete files. You need a process that’s as efficient as your business. A seasoned commercial mortgage broker Ontario ensures each phase moves without friction. We take charge of the timeline so you don’t miss out on prime GTA assets. Speed is your competitive advantage. Reliability is ours.

Phase 1: The Initial Assessment and Pro Forma Review. We start by stress-testing your numbers. We look at your projected income versus expenses to ensure the deal makes sense before it hits a lender’s desk. Phase 2: Letter of Intent (LOI) and Lender Selection. Once we identify the right capital source, we secure a soft approval. This LOI outlines the proposed rate, term, and key conditions. Phase 3: Due Diligence. This is the heavy lifting. Third-party experts conduct appraisals, environmental audits, and building condition reports. Phase 4: Commitment Letter and Legal Closing. The lender issues a formal, binding offer. Your lawyer then handles the mortgage registration and fund transfer.

Essential Documentation for a Successful Application

Lenders in 2026 are obsessed with data. You need your personal net worth statements and corporate tax returns organized and ready. If you’re buying an income-producing property, an accurate rent roll is non-negotiable. Lenders also demand property operating statements for the last two to three years. Be prepared for a Phase 1 Environmental Site Assessment (ESA). It’s a standard requirement to check for soil or groundwater contamination. Having these documents ready on day one can shave weeks off your approval time. Don’t let a missing tax form stall your growth.

Navigating the Closing Process in Ontario

The final mile requires a specialized commercial real estate lawyer. They don’t just sign papers; they review titles and manage the complex registration of the mortgage. You must budget for closing costs early. These include Ontario’s Land Transfer Tax, legal fees, and broker fees. In the GTA, these costs can add up quickly. To ensure your funding arrives on the scheduled date, respond to lender queries immediately. Even a small delay in providing a building insurance certificate can push your closing back. Precision at this stage is vital for a smooth transition of ownership.

Ready to start Phase 1 and get your numbers reviewed? Contact us today to move your application forward with confidence.

Why Dhugga Mortgages is Your Strategic Advantage in Ontario

Choosing the right commercial mortgage broker Ontario is a strategic decision for your company’s future. It isn’t just about a transaction; it’s about a partnership built on trust and speed. At Dhugga Mortgages, we don’t just process files. We champion your business growth. You get direct access to Jaspreet Dhugga’s deep industry expertise and the massive reach of the Mortgage Alliance network. This combination gives you a distinct edge. We provide access to a vast pool of institutional and private capital that most borrowers can’t reach alone. Our approach is results-oriented. We prioritize deal certainty above all else. You need to know your funding is secure so you can focus on your daily operations. We remove the friction of complex underwriting. We handle the heavy lifting. We drive the process from start to finish.

Local Expertise in Brampton, Mississauga, and Toronto

Our roots in the community are deep. We understand the specific zoning shifts and growth trends across the GTA. Whether it’s an industrial expansion in Brampton or a multi-family project in the Toronto core, we know the terrain. We speak the language of Ontario business owners because we are part of the same community. Our approach is proactive. We don’t wait for lenders to call us; we drive the conversation. Our track record of successful GTA closings serves as your social proof. We are the helpful neighbour with professional expertise. We realize that every hour matters in a competitive market. We move at the speed of your business. We ensure your capital is ready when you are.

Comprehensive Financial Solutions Beyond Commercial

Your business is only one part of your wealth strategy. We help you integrate your commercial financing with your overall financial goals. Many of our clients transition seamlessly from business acquisitions to personal property needs. We specialize in first-time home buyer mortgages for entrepreneurs looking to plant roots in Ontario. We also provide dedicated support for self-employed and newcomer investors who often face traditional bank hurdles. We see the big picture. We organize your debt to maximize your flexibility and tax efficiency. We don’t offer generic advice. We offer tailored solutions that reflect your unique situation. Ready to act now? Get your commercial quote today and secure your 2026 growth with a partner who values your time.

Dominate the Ontario Commercial Market with Strategic Capital

Success in 2026 requires more than just finding a property. It demands a financing structure that aligns with your specific growth timeline. You’ve seen how selecting the right capital source, whether institutional or private, can mean the difference between a stalled project and a successful closing. By following a clear application roadmap and preparing your documentation early, you remove the guesswork from the lending process. You gain peace of mind through speed and deal certainty. Your business deserves a partner that moves as fast as the market does.

As a leading commercial mortgage broker Ontario, Dhugga Mortgages provides the local expertise you need to navigate these complex decisions. We are independently owned and operated under the Mortgage Alliance network. Our team acts as specialists in complex self-employed and private lending scenarios across the Brampton and GTA markets. We bridge the gap between rigid bank rules and your unique business goals. Don’t let market volatility slow your momentum. Take the next step toward your next property investment with absolute confidence.

Secure Your Strategic Commercial Advantage—Get a Quote Today

Frequently Asked Questions

What is the typical down payment for a commercial mortgage in Ontario?

Down payments for commercial properties usually range from 25% to 35% of the purchase price. High-demand assets like industrial warehouses or multi-family buildings might qualify for lower requirements. Conversely, vacant land or specialized facilities often require 50% or more. Your commercial mortgage broker Ontario helps determine the exact equity needed based on the property’s risk profile and cash flow.

How do commercial mortgage rates in Ontario compare to residential rates?

Commercial rates are generally higher than residential rates; they usually carry a premium of 0.5% to 2%. This reflects the higher risk and complexity of business lending. In May 2026, CMHC-insured benchmarks sat between 4.13% and 4.33% plus lender premiums. You should also account for lender and appraisal fees that aren’t typically part of residential deals.

Can I get a commercial mortgage if I am self-employed with limited NOAs?

You can secure financing through private or alternative lenders who prioritize property equity over personal tax documents. Traditional banks demand extensive income verification. However, alternative lenders focus on your property’s net operating income. We specialize in self-employed mortgages that use bank statements or lease agreements to prove your ability to service the debt.

How long does the commercial mortgage approval process usually take?

A typical approval takes between 4 and 12 weeks from the initial application to the final funding. Private mortgages can close in as little as 5 to 10 days if the appraisal and environmental reports are ready. CMHC-insured deals for multi-family units are the slowest; they often require several months for full processing. Start early to ensure you meet your specific closing deadlines.

What is a DSCR, and why does my broker keep mentioning it?

DSCR stands for Debt-Service Coverage Ratio; it measures your property’s ability to cover its mortgage payments. Lenders calculate this by dividing your Net Operating Income by your total annual debt obligations. Most Ontario lenders look for a ratio between 1.2 and 1.4. If your ratio is too low, you’ll likely need a larger down payment to reduce the loan amount.

Are there specific commercial mortgage programs for newcomers to Canada?

Newcomers can access specialized programs that often require a 35% down payment and proof of credit history from their home country. Lenders also look for significant liquid assets to ensure you can manage the property during your transition. Working with a commercial mortgage broker Ontario ensures you find lenders who value your international experience and global net worth.

What are the main differences between a commercial bank loan and a private commercial mortgage?

Banks offer the lowest interest rates but follow rigid, slow qualification rules. Private mortgages prioritize speed and flexibility; they’re ideal for bridge financing or deals that don’t fit institutional boxes. While private loans have higher rates, they require less paperwork and can fund projects that banks won’t touch. Choose the source that matches your timeline and deal complexity.

Do I need a Phase 1 Environmental Assessment for all commercial properties?

Most lenders require a Phase 1 Environmental Site Assessment (ESA) for every commercial transaction. This report ensures the land isn’t contaminated from previous industrial or automotive use. If the Phase 1 report flags potential issues, you’ll need a more detailed Phase 2 study involving soil samples. Skipping this step can lead to a sudden decline of your mortgage application during the due diligence phase.