Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Private Mortgage Requirements Ontario: Your 2026 Approval Guide

- Home

- Private Mortgage Requirements Ontario: Your 2026 Approval Guide

In the Ontario lending market, your property is the primary borrower; your equity is your credit score. If a major bank recently rejected your application due to a strict stress test or self-employment status, don’t worry. You’re part of a growing group of homeowners who realize that traditional institutions often ignore real-world property value in favour of rigid debt ratios. Mastering the private mortgage requirements Ontario lenders demand is the fastest way to bypass these hurdles and secure the funding you deserve. We understand the fatigue of bank rejections, especially when you need urgent capital for debt consolidation or a fast-approaching closing date.

This guide provides a clear roadmap to the 2026 lending landscape. You’ll learn how the January OSFI regulations for investment properties impact your options and why Loan-to-Value ratios are the most critical factor in your approval. We’ll break down the specific documentation needed to move your application from pending to funded without the typical bank delays. Get ready to take control of your finances with a professional, proactive approach to private lending.

Key Takeaways

- Focus on property equity over credit scores. Unlock short-term funding even after a traditional bank rejection.

- Learn the specific private mortgage requirements Ontario lenders demand. Discover why a 65-75% Loan-to-Value ratio is the sweet spot for GTA approvals.

- Use our streamlined document checklist. Move from application to funding with professional speed and efficiency.

- Understand how urban locations in centres like Mississauga impact your rates. Use property condition to your advantage.

- Build a clear exit strategy. Use private lending as a strategic bridge to repair your credit and return to traditional bank rates.

Understanding Private Mortgages in Ontario: A Strategic Short-Term Tool

Think of a private mortgage as a strategic financial bridge. It is a short-term loan, typically lasting one to three years, funded by private individuals or corporations instead of traditional institutions. Understanding Private Mortgages requires shifting your perspective from your salary to your property value. These lenders don’t get bogged down in your credit history or complex income verifications. They look at the equity you’ve built in your home. This asset-based approach is what defines the private mortgage requirements Ontario lenders use to assess risk and approve files that banks won’t touch.

In Ontario, these loans provide the speed that big banks simply can’t match. Whether you need to close a property deal in days or consolidate high-interest debt, private lending offers a path forward. The Financial Services Regulatory Authority of Ontario (FSRA) oversees these transactions to ensure the process remains transparent. They emphasize that these loans should be short-term solutions. By choosing this path, you gain access to capital based on your home’s appraisal rather than a computer-generated credit score. It’s a regulated, professional alternative for homeowners who favour flexibility over rigid institutional rules.

When to Consider a Private Lender

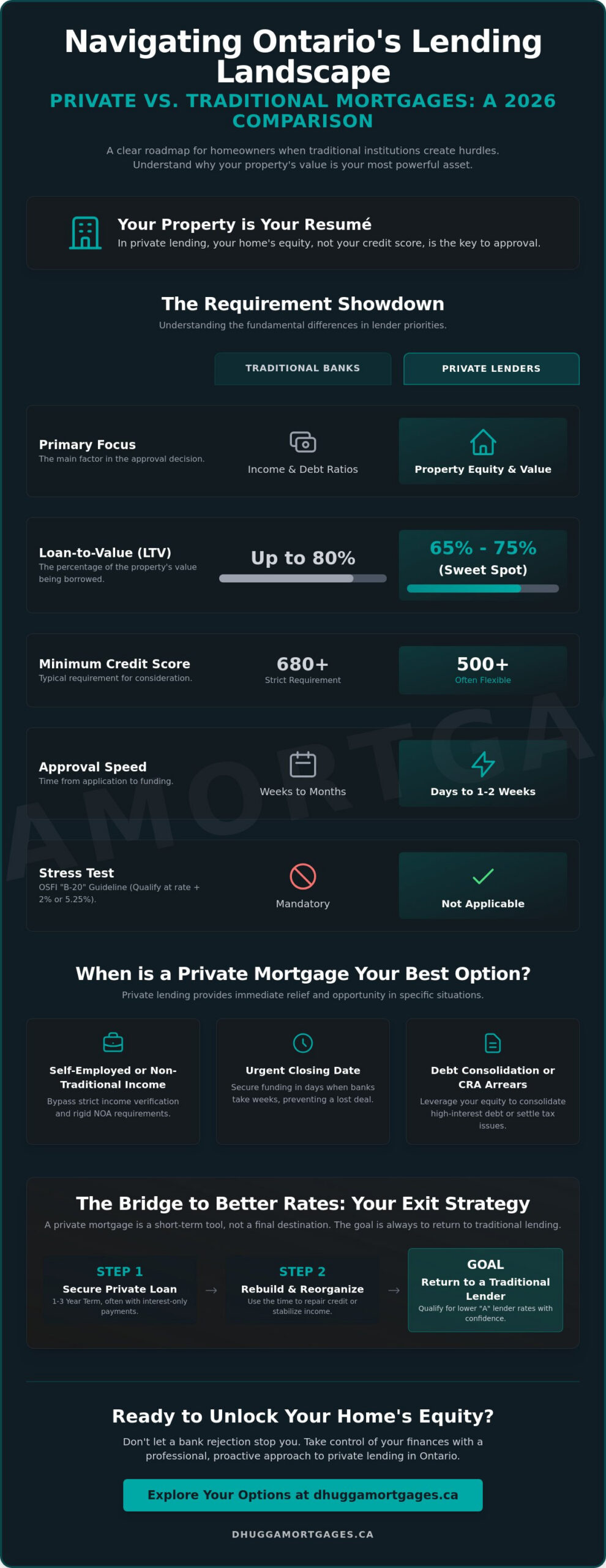

The “B-20” stress test remains the biggest hurdle for many Ontario residents. As of May 2026, you must still qualify at the higher of 5.25% or your contract rate plus 2%. This often disqualifies self-employed professionals who lack standard Notices of Assessment (NOA) or have non-traditional income streams. If you’re facing a power of sale or have significant CRA arrears, a private lender provides immediate relief. It stops the clock. It gives you the breathing room to reorganize your finances without the fear of losing your property. You realize the value of your home today instead of waiting for a credit score to catch up.

The Short-Term Nature of the Loan

Most private terms in Brampton and across major Ontario centres are 12 months. This isn’t a permanent destination; it’s a 365-day window to improve your credit or prepare for a future sale. These loans often feature interest-only payments. This structure keeps your monthly cash flow manageable while you execute your recovery plan. You aren’t paying down the principal during this time. Instead, you’re buying the time needed to eventually qualify for lower bank rates. Every private loan must have a clear exit strategy from day one. We help you map out that 12-month horizon so you can transition back to traditional lending with confidence.

The Essential Private Mortgage Requirements in Ontario for 2026

In the private lending world, your home is your resumé. While traditional banks obsess over your debt-to-income ratios, private lenders prioritize your equity stake. This shift from borrower-centric to property-centric underwriting is the core of private mortgage requirements Ontario lenders use today. To secure a 2026 approval, you generally need a minimum equity position of 25% to 35%. This means your Loan-to-Value (LTV) ratio should ideally sit between 65% and 75%. If you’re in a high-demand area like the GTA, lenders are often more aggressive. If you’re in a rural area, they might ask for more skin in the game to mitigate risk.

Compliance is also a key factor for your peace of mind. All private lending activities must align with The Essential Private Mortgage Requirements in Ontario, which are governed by the Mortgage Brokerages, Lenders and Administrators Act. This legislation ensures that even though the rules are flexible, the process remains professional and transparent. You don’t need a perfect credit score to qualify. In fact, many lenders will approve applications with scores as low as 500, provided the property value is stable and the exit strategy is clear. They want to see a path back to traditional banking, not a permanent debt cycle.

Private vs. Traditional Requirement Comparison

Understanding the gap between institutional and private lending helps you prepare a winning application. Private lenders focus on the marketability of the asset. They want to know how quickly the home could sell if needed. This is why location often trumps income history. Consider these key differences:

- Credit Score: Banks typically require 680 or higher. Private lenders are often satisfied with 500 or above.

- Income Proof: Banks demand T4s and Notices of Assessment. Private lenders accept stated income or bank statements.

- Property Location: Banks prefer urban or suburban hubs. Private lenders have a broader range but favour marketable areas.

- Approval Speed: Banks take weeks. Private lenders can often provide a commitment within 24 hours.

The Role of the Appraisal

An Ontario-certified appraisal is your most important document. Lenders won’t rely on your tax assessment or a real estate listing price. They need an independent, third-party valuation of the “as-is” condition. In Brampton, where the market moves fast, appraisers look at recent comparable sales within a tight radius. In rural areas, they might look at a wider range. This valuation determines your total loan amount. If you’re ready to see how much equity you can unlock, speak with a mortgage expert today to start the process.

Property Standards and Equity: What Ontario Lenders Prioritize

In private lending, the property is the security. While your personal story matters, the marketability of your real estate is what drives the final decision. Lenders prioritize liquidity. They want to know how quickly a property can be sold in a worst-case scenario. This is why location is a primary factor in private mortgage requirements Ontario lenders establish for their portfolios. Urban centres like Mississauga or Toronto often command more competitive rates because the high demand in these areas ensures a fast exit. Conversely, properties in remote areas or those with unique zoning, such as agricultural land in Caledon, may face stricter terms due to a smaller pool of potential buyers.

Property condition also plays a vital role. Private lending is a strategic short-term tool that allows you to secure funds for fixer-uppers or homes mid-renovation. However, lenders will focus heavily on the “as-is” value provided in the appraisal. If a renovation is incomplete, the lender may hold back a portion of the funds until specific milestones are reached. Their goal is to ensure the asset remains a viable piece of collateral throughout the term of the loan. They aren’t just looking at the house today; they’re looking at its resale potential tomorrow.

Calculating Your Usable Equity

Equity is the difference between what your home is worth and what you owe. To find your Loan-to-Value (LTV) ratio, use this simple formula: (Total Mortgages / Property Value) x 100. For example, if your home is worth $1,000,000 and you have a $600,000 first mortgage, your LTV is 60%. Most Ontario private deals require a minimum of 25% equity to move forward. It’s also important to realize that existing liens or judgements, such as unpaid property taxes or CRA arrears, are subtracted from your usable equity. Lenders want a clean equity position before they commit their capital.

Acceptable Property Types

Standard residential properties are the easiest to fund. This includes detached homes, townhouses, and high-rise condos in major Ontario hubs. Rural properties present different challenges. Lenders often require proof of a functioning septic system and a water potability test for well-fed homes. For investment properties, lenders are increasingly interested in the rental income the property generates. While the equity remains the foundation of the private mortgage requirements Ontario investors look for, a strong rental profile can sometimes help justify a higher LTV or a more favourable interest rate.

Documentation and the Fast-Track Application Process

Speed is our standard. Momentum is your advantage. When you are facing a tight closing date or an urgent debt deadline, waiting weeks for a bank’s decision is not an option. Our ‘Speed to Lead’ philosophy focuses on getting you a commitment letter within 24 hours. This rapid pace is possible because private mortgage requirements Ontario lenders prioritize the property over complex personal financial histories. We cut through the red tape to focus on what matters: your equity and your exit strategy. You provide the documents; we provide the path to funding.

The appraisal is the most critical step in this timeline. It is the engine that drives the deal. Without an Ontario-certified appraisal from an approved professional, the process stops. This document confirms the “as-is” value that determines your total loan amount. Once the value is established, we move to the paperwork. You will also need separate legal representation. In Ontario, the borrower and the lender must each have their own lawyer to ensure the transaction is transparent and legally sound. This protects your interests while ensuring the funds are disbursed correctly.

Step-by-Step Approval Timeline

- Initial Consultation (1-2 hours): We assess your usable equity and define your immediate financial goals.

- Commitment Letter: You receive a formal offer. This document outlines your interest rate, lender fees, and terms. Review it. Sign it. We move to the next stage.

- The Closing Process: Your lawyer handles the final signatures and receives the funds. They pay out any existing liens or debts directly from the proceeds.

Common Documentation Hurdles

Small details can cause big delays. Ensure your property taxes are up to date with your municipality. Lenders require a clean tax certificate before funding. You must also provide proof of home insurance with the private lender named as the “loss payee” on the policy. Don’t worry about CRA arrears. Even if you owe back taxes, providing your most recent Notice of Assessment (NOA) is a requirement. We often use the new private mortgage to pay those arrears off, clearing your path back to traditional bank rates. If you are ready to bypass the bank’s delays, apply for your fast-track approval now.

Your essential document checklist includes:

- Two pieces of valid Canadian ID.

- A current property tax bill or statement.

- Your most recent mortgage statement for any existing loans.

- Proof of homeowner’s insurance.

- A professional appraisal (we can help coordinate this).

Securing Your Exit Strategy: The Dhugga Mortgages Advantage

A private mortgage is a bridge. It is never a final destination. In the 2026 Ontario market, having a clear exit strategy is a core component of the private mortgage requirements Ontario lenders expect to see. We don’t just find you the capital to solve today’s problem. We map out the path to ensure you aren’t paying private rates longer than necessary. Whether you are consolidating debt or avoiding a power of sale, the goal is always a return to traditional institutional lending. We provide the roadmap. We guide the transition.

Our team understands the unique shifts within the GTA real estate market. From Brampton to Mississauga, property values fluctuate. We use our local expertise to time your transition perfectly. We monitor market trends to ensure your equity position remains strong. This proactive approach removes the complexity from the process. You get peace of mind knowing your short-term solution has a long-term plan. We act as your strategic partner, not just a broker. We take charge so you can focus on your financial recovery. Speed matters; results matter more.

Your Path Back to Traditional Lending

The journey back to the bank starts on day one. We set clear milestones for your credit score improvement. Reaching the 680 threshold is often the target for major lenders. We help you organize your income documentation and clean up any outstanding collections. This preparation is vital for future ‘B’ lender or ‘A’ lender applications. For those looking at long-term homeownership goals, check our First Time Home Buyer Mortgage Ontario guide for comprehensive strategic planning. We ensure every step you take moves you closer to lower interest rates.

Why Experience Matters in Private Lending

Experience is the edge you need. We provide access to an exclusive network of Ontario private investors who understand real-world equity. Our fee structures are transparent. There are no hidden surprises at the lawyer’s office. We believe in direct action and immediate results. We handle the heavy lifting. We coordinate with the appraisers and lawyers to ensure a seamless experience. Don’t let bank rejections stop your progress. Contact Jaspreet Dhugga today for a fast equity appraisal. Let’s secure your funding and build your exit strategy together. Your equity is your power; use it wisely.

Take Control of Your Financial Future

You now have the roadmap to bypass traditional bank rejections. Property equity is your greatest asset. By mastering the private mortgage requirements Ontario lenders demand; you turn your home’s value into immediate capital. This strategic bridge buys you the time needed to repair credit. It allows you to reorganize finances without the pressure of institutional stress tests. Momentum matters. Results matter more.

We are a FSRA Licensed Brokerage and GTA local market experts. We specialize in removing complexity. We deliver 24-hour commitment letters to keep your financial goals on track. Speed is our standard. Reliability is our promise. Don’t let a “no” from a bank stop your progress. Take the next step with a partner who understands the local market landscape. Your financial recovery starts with a single proactive decision. We are ready to help you move forward with confidence and clarity.

Secure Your Private Mortgage Approval Now

Frequently Asked Questions

What is the minimum credit score for a private mortgage in Ontario?

A credit score of 500 is often the baseline for approval. While banks demand high scores, private lenders prioritize your property’s equity position. If you have 25% to 35% equity, your credit history becomes a secondary concern. We focus on your home’s value to secure the funding you need quickly.

How much are private mortgage fees in Ontario for 2026?

Private mortgage fees generally include a lender fee and a broker fee. These are typically deducted from the total loan amount at the time of closing. You should also account for legal costs and appraisal fees. These costs reflect the higher risk and the speed of the transaction compared to traditional bank loans.

Can I get a private mortgage if I am self-employed with no proof of income?

Yes, you can qualify using stated income. Meeting the private mortgage requirements Ontario lenders set often means bypassing traditional T4 or NOA verification. We look at your bank statements and property value rather than institutional income ratios. This makes it an ideal solution for self-employed professionals with non-traditional earnings.

How long does it take to get a private mortgage approved in Brampton?

Approvals in Brampton and the GTA often happen within 24 hours. The entire process from application to funding typically takes 5 to 10 business days. This timeline depends on how quickly the appraisal is completed and how fast your lawyer processes the documents. Speed is the primary advantage of this lending model.

Do I need a lawyer for a private mortgage transaction in Ontario?

Independent legal representation is a mandatory requirement in Ontario. You and the lender must each have your own lawyer to ensure a transparent transaction. Your lawyer will handle the title search, verify the mortgage terms, and facilitate the transfer of funds. This structure protects all parties involved in the deal.

What happens if I cannot pay back my private mortgage at the end of the term?

You must execute a clear exit strategy before the term ends. If you cannot pay back the principal, you may need to refinance into a new loan or sell the property. While some lenders offer renewals, they are not guaranteed. We work with you from day one to ensure a viable path back to traditional bank rates.

Can I use a private mortgage to stop a Power of Sale?

Private mortgages are a common tool used to stop a Power of Sale. By securing fast equity-based funding, you can pay off the arrears and legal costs of the existing lender. This stops the legal proceedings immediately. It gives you the time needed to reorganize your finances or list the home on your own terms.

Is a private mortgage a second mortgage or a first mortgage?

A private mortgage can be registered as either a first or a second mortgage. If you have an existing low-interest bank loan, a private second mortgage allows you to access equity without breaking your current term. If your property is clear of debt, the private loan is registered in the first position.