Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Second Mortgage Mississauga: The 2026 Strategic Guide to Unlocking Equity

- Home

- Second Mortgage Mississauga: The 2026 Strategic Guide to Unlocking Equity

Why would you sacrifice a record-low mortgage rate just to settle high-interest debt? In 2026, the most strategic move for Mississauga homeowners isn’t a total refinance. It is a surgical strike. Your property is likely worth nearly $1 million. You have built significant equity. You shouldn’t be held back by 20% credit card interest or a rigid bank denial. We know the local market is shifting toward a more favourable buyer’s environment. We also understand that traditional lenders often make Peel Region property appraisals feel like an impossible hurdle.

You want to keep your current low-rate mortgage while accessing the cash you’ve already earned. This is the right move. Our guide shows you exactly how to leverage a second mortgage Mississauga to consolidate debt or fuel new investments this year. You will learn how to bypass the big banks and secure quick funding without resetting your primary loan. We’ll outline the steps to achieve a debt-free lifestyle while keeping your financial foundation intact. It is time to stop waiting for the banks and start using your home’s value to your advantage.

Key Takeaways

- Protect your low-interest first mortgage. Access your home equity without triggering expensive refinancing penalties or resetting your current rate.

- Secure a second mortgage Mississauga. Consolidate high-interest credit card debt into one manageable payment or fund value-adding home renovations.

- Bypass rigid bank requirements. Focus on your property’s appraised value to get the cash you need, even if your credit score isn’t perfect.

- Simplify the approval process. Learn why your Loan-to-Value ratio is the most important factor for unlocking funding in 2026.

- Gain a strategic edge. Navigate the Peel Region lending landscape with expert guidance and access to a broad network of private and institutional lenders.

What is a Second Mortgage in Mississauga and How Does it Work?

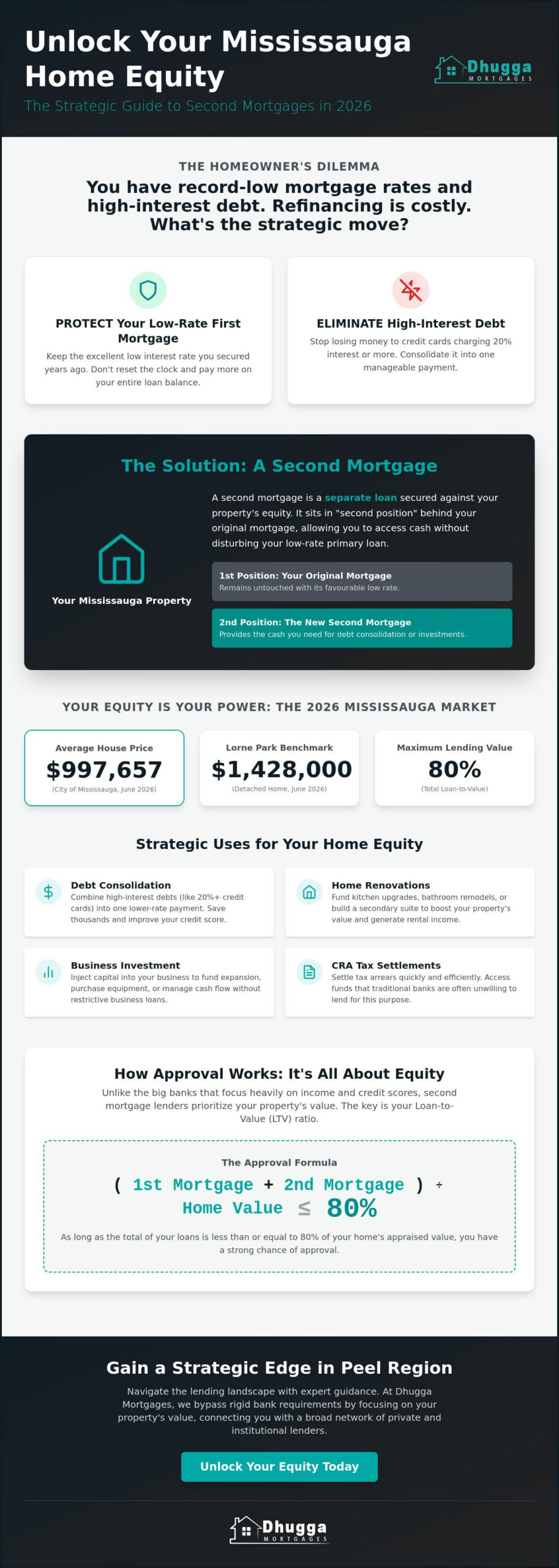

A second mortgage is a separate loan registered against your property while your original mortgage remains in place. Think of it as a secondary layer of financing. It sits behind your primary loan. This is a powerful tool because it allows you to tap into your home’s equity without touching your first mortgage. In 2026, many Mississauga homeowners are holding onto specific low rates from years prior. Refinancing that entire amount would mean losing that advantage. A second mortgage Mississauga solves this. You keep your low-rate first mortgage and take out a smaller, separate loan for the specific amount you need.

The “Second Position” Explained

The term “second” refers to the lender’s priority on your property’s title. If the home is sold or there is a default, the first mortgage lender gets paid first. The second lender is next in line. Because they take on more risk, second mortgage rates are typically higher than first mortgage rates. However, the total interest cost is often lower than a full refinance. You avoid breaking your first mortgage and paying massive prepayment penalties. This setup is a strategic way to access cash quickly. It is about protecting your primary financial foundation while still moving forward with your goals.

Mississauga Real Estate Context in 2026

Mississauga’s property market remains a source of significant wealth. As of June 2026, the average house price in the city is $997,657. In high-demand neighbourhoods like Lorne Park, detached home benchmark prices sit around $1,428,000. This massive value provides a robust equity cushion. Even with the market currently leaning in favour of buyers, the equity built over the last decade is substantial. A second mortgage Mississauga relies heavily on this value.

Lenders focus on your Loan-to-Value (LTV) ratio. In Canada, your total debt cannot exceed 80% of your home’s appraised value. Whether you are in Churchill Meadows or Lakeview, a professional Peel Region appraisal is the key. It confirms exactly how much room you have to borrow. This process is efficient and focused on the “now.” It bypasses the rigid income-testing that often stops bank approvals. You use your home’s current worth to secure your financial future. It is a fast, reliable way to move your plans from the drawing board to reality.

Strategic Reasons to Consider a Mississauga Second Mortgage

Accessing equity isn’t just about getting cash. It’s about strategic growth. In 2026, Mississauga homeowners are using their property as a financial tool to solve immediate problems or build future wealth. A second mortgage Mississauga provides the liquidity you need without disrupting your primary financial plan. It is a targeted solution for specific goals. Whether you are dealing with high-interest debt or looking to expand your portfolio, your home equity is the key. Consider these strategic uses for your capital:

- Debt Consolidation: Wipe out credit card balances that carry 20% interest or higher.

- Home Improvements: Boost your property value by upgrading kitchens, bathrooms, or landscaping.

- Business Growth: Fund an expansion or bridge a cash flow gap for your local business.

- CRA Settlements: Pay off tax arrears that traditional banks refuse to finance.

Debt Consolidation: The Interest Rate Win

Credit card interest is a wealth killer. Many cards today charge 20% or more. A second mortgage Mississauga offers a way out. Even though second mortgage rates are higher than firsts, they typically range from 6% to 12% in 2026. This massive gap saves you thousands in interest every year. Debt consolidation for Mississauga homeowners is the process of using home equity to pay off multiple high-interest creditors, leaving you with one single monthly payment at a much lower interest rate. This move lowers your credit utilization ratio immediately. Your credit score will likely climb as you pay down the principal faster. It is about taking control of your cash flow today.

Property Investment and Renovations

Your home can fund your next big move. Many residents are now building secondary suites or accessory dwelling units (ADUs) to generate income. Under 2026 regulations, homeowners can access an insured refinance of up to 90% for these projects. If you want to keep your current first mortgage intact, a second mortgage provides the capital to start construction now. This adds immediate rental income and long-term value to your property. Others use their Mississauga equity to secure a down payment for a rental property elsewhere in the GTA. According to the Canadian Government on Home Equity, using your home to build wealth is a common strategy, provided you understand the risks involved.

Emergency expenses don’t wait for bank appointments. If you’re self-employed or have had a credit hiccup, the big banks might say no. We focus on your equity instead. You can use your property’s value to settle tax arrears or fund a business expansion when timing is everything. If you’re ready to see how much equity you can unlock, reach out to our team today for a quick assessment. We move fast so you can too.

Second Mortgage vs. HELOC vs. Refinancing: Which is Best?

Choosing the wrong equity product can cost you tens of thousands of dollars in unnecessary interest and fees. In 2026, the decision hinges on your current first mortgage rate and your specific financial profile. Refinancing involves replacing your entire first mortgage with a new loan. This often triggers massive prepayment penalties. If you are currently locked into a 2% or 3% rate from years ago, breaking that contract is usually a poor move. You would be trading a low rate on your entire balance for a much higher market rate today. A second mortgage Mississauga allows you to keep that low rate untouched while accessing the cash you need.

HELOCs (Home Equity Lines of Credit) offer a revolving line of credit. You only pay interest on what you use. However, big banks have strict requirements for HELOCs. They demand high credit scores and traditional proof of income. If you are self-employed or have a bruised credit history, a HELOC might be out of reach. Second mortgages provide a one-time lump sum. They are significantly easier to qualify for because lenders prioritize your property’s equity over your credit report. It is a faster, more accessible route to liquidity.

When to Choose a Second Mortgage

This is the ideal choice if you have a low-rate first mortgage and want to avoid heavy penalties. It is also the go-to for those with non-traditional income. If you are a business owner or freelancer, a second mortgage Mississauga bypasses the red tape. You get the funds you need based on your home’s value. If your goal is to restructure your entire debt load, you might consider mortgage refinancing Ontario, but only if the numbers make sense for your total balance. For most, keeping the first mortgage intact is the winning strategy.

Comparing the Total Cost of Borrowing

Analyze the Return on Investment (ROI) before signing. A second charge involves specific costs like legal fees, appraisal fees, and lender fees. In Ontario, legal fees for these transactions typically range from $1,500 to $2,500. Appraisals generally cost between $300 and $500. While the interest rate is higher than a first mortgage, you are only paying that rate on the new funds, not your entire home loan. This is often the cheapest way to borrow when you factor in the avoided penalties. For many, this is the most efficient path for a debt consolidation mortgage Canada. You eliminate high-interest cards without sacrificing your primary mortgage advantage. It is a surgical financial strike that protects your long-term wealth.

The Mississauga Second Mortgage Approval Process

Speed is our priority. When you need to access equity, you shouldn’t be buried in paperwork for weeks. Our process for a second mortgage Mississauga is streamlined to deliver results quickly. We focus on the value of your home rather than just your credit score. This allows for a much faster approval than traditional bank refinancing. Here is exactly how we move from your first inquiry to cash in your bank account:

- Step 1: LTV Consultation. We calculate your current Loan-to-Value ratio based on your existing mortgage balance and estimated home value.

- Step 2: Documentation. You provide your latest mortgage statement, property tax bill, and proof of insurance. We keep the list short.

- Step 3: Professional Appraisal. A local Mississauga firm visits your property to confirm its current market worth.

- Step 4: Commitment Letter. The lender reviews the file and issues a formal offer outlining your rate and terms.

- Step 5: Legal Closing. Your lawyer reviews the documents, you sign, and the funds are disbursed.

Why Equity is the Primary Driver

Traditional banks obsess over your income and credit score. We don’t. We work with private mortgage lenders Ontario who prioritize the asset. If you have enough equity, you are likely approved. In the Mississauga market, lenders typically offer up to 80% LTV, though some private options may stretch to 90% in high-demand pockets. This asset-based approach is what makes a second mortgage Mississauga so accessible for self-employed individuals or those with non-traditional income. We look at what your home is worth today, not what your credit report said three years ago. It’s about your property’s potential, not your past hurdles.

Navigating Peel Region Appraisals

An appraisal is a professional assessment of your home’s market value that serves as the lender’s security for the loan. In 2026, Mississauga appraisers are focused on specific metrics. They look at lot size, recent sales in your immediate neighbourhood, and any recent upgrades. With the average house price sitting at $997,657 as of June 2026, every detail counts. To maximize your value, ensure your home is clean and curb appeal is at its peak. Appraisers in Churchill Meadows or Lorne Park will compare your property against the 568 homes sold in May 2026 to find an accurate benchmark. A higher appraisal means more cash available for your goals. If you are ready to get started, book your equity consultation today and let’s unlock your home’s potential.

Why Choose Dhugga Mortgages for Your Mississauga Second Charge?

You need a partner who understands the specific pulse of the Peel Region. We aren’t just a voice on the phone. We are your neighbours. Securing a second mortgage Mississauga requires more than just a lender list; it requires a strategic advocate. We bring deep professional expertise to every file. Our team navigates the complexities of local property values and lending regulations so you don’t have to. We focus on your advantage. We ensure every step is handled with the speed and reliability you expect from a local expert.

- Broad Network Access: We connect you to a diverse range of private and institutional second mortgage lenders.

- Proactive Approach: Our results-oriented process values your time and prioritizes your specific financial goals.

- Total Transparency: We provide clear fee structures with no hidden surprises at the lawyer’s office.

- Established Reliability: We have a proven track record of helping homeowners across the GTA unlock their equity.

Local Knowledge, Professional Results

We know Mississauga neighbourhoods from Meadowvale to Port Credit. This local presence allows us to secure faster approvals for our clients. We understand how to position your equity to get the best possible “edge” in the 2026 market. Our history of helping GTA homeowners realize their financial goals is built on trust and efficiency. We remove the complexity from the borrowing process. You get peace of mind and the cash you need without the usual bank delays. It’s about making your home work for you.

Ready to Unlock Your Home Equity?

Don’t let high-interest debt drain your savings. It’s time to act. Contact Jaspreet Dhugga today for a personalized equity assessment. Our 2026 digital application process is streamlined for maximum speed. It is built to fit your busy lifestyle. Stop overpaying on credit cards and start leveraging your home’s true value today. We take charge of the process from start to finish. Your financial freedom is just one conversation away. Let’s get to work on your second mortgage Mississauga and move your plans forward.

Take Charge of Your Mississauga Home Equity Today

Your property is your most powerful financial tool. In 2026, the smartest move is a surgical one. Protect your low-rate first mortgage while accessing the cash you need. A second mortgage Mississauga allows you to consolidate debt or fund renovations without the stress of bank denials. You’ve built the equity. Now it’s time to use it. We’ve simplified the path to liquidity by focusing on your home’s value rather than just your credit score. It’s about moving forward with confidence.

Dhugga Mortgages is your local partner for fast results. We provide access to over 50 private and institutional lenders. As specialists in Mississauga equity-based lending, we understand the local market better than anyone. We move at your speed. Expect fast 24-hour commitment letters to keep your financial goals on schedule. Stop letting high-interest debt hold you back. Start leveraging your success today. We take the complexity out of the process so you can focus on your future.

Get Your Mississauga Second Mortgage Approved Today. We are ready to secure your financial edge. Let’s unlock your potential now.

Frequently Asked Questions

What is the current interest rate for a second mortgage in Mississauga?

Interest rates for a second mortgage in Canada generally range from 6% to 12% as of May 2026. Your specific rate depends on your credit score, the amount of equity in your home, and the lender type. While these rates are higher than primary mortgage rates, they remain significantly lower than the 20% or more typically charged by credit card companies. It is a strategic middle ground for accessing capital.

Can I get a second mortgage in Mississauga with bad credit?

Yes, you can secure a second mortgage Mississauga even with a low credit score or previous bank denials. Private and alternative lenders prioritize the equity in your home rather than your credit history. If your property has sufficient value and sits within the required loan-to-value limits, your credit score becomes a secondary factor. We focus on your asset to get you the funding you need.

How much equity do I need for a second mortgage in Ontario?

You typically need to have at least 20% equity remaining in your home after the new loan is added. Canadian regulations require that the total of your first and second mortgages cannot exceed 80% of your property’s appraised value. For a home in Mississauga valued at the June 2026 average of $997,657, your total debt across both mortgages would be capped at approximately $798,125. This ensures a safety cushion for the lender.

Will a second mortgage affect my existing first mortgage rate?

No, a second mortgage is a separate legal contract and will not change your first mortgage terms. This is why many homeowners choose this path. You keep your existing low interest rate and payment schedule on your primary loan. You simply add a second, smaller payment for the new funds. It is an efficient way to borrow without losing the advantage of a first mortgage secured years ago.

How long does the approval process take for a second mortgage?

The approval process is significantly faster than a traditional bank refinance. We can often issue a commitment letter within 24 hours of receiving your initial documentation. The entire process from application to fund disbursement usually takes between one and two weeks. This timeline includes the professional appraisal and legal signing. We prioritize speed because we know your financial needs are often urgent.

What are the typical fees associated with a second mortgage in Mississauga?

You should budget for legal fees, appraisal costs, and title insurance. In Ontario, legal fees for mortgage transactions typically range from $1,500 to $2,500. A professional appraisal in the Peel Region generally costs between $300 and $500. Title insurance is another common cost, usually ranging from $300 to $500. These fees are often deducted directly from the mortgage proceeds so you don’t have to pay them out of pocket.

Can I use a second mortgage to stop a Power of Sale in Mississauga?

Yes, a second mortgage is a specialized tool used to stop a Power of Sale and protect your home equity. It provides the immediate cash required to pay out arrears on your first mortgage and bring the loan back into good standing. This is a time-sensitive situation that requires a proactive lender who can move fast. We specialize in these high-velocity approvals to save your property from legal action.

Is the interest on a second mortgage tax-deductible in Canada?

Interest is only tax-deductible if the funds are used for the purpose of earning income. If you use a second mortgage Mississauga to invest in a business or purchase a rental property, the interest may be deductible on your tax return. If the funds are used for personal debt consolidation or home renovations on your primary residence, the interest is generally not deductible. You should always verify your specific case with a qualified tax professional.