Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Commercial Mortgage Broker Brampton: Your 2026 Business Financing Guide

- Home

- Commercial Mortgage Broker Brampton: Your 2026 Business Financing Guide

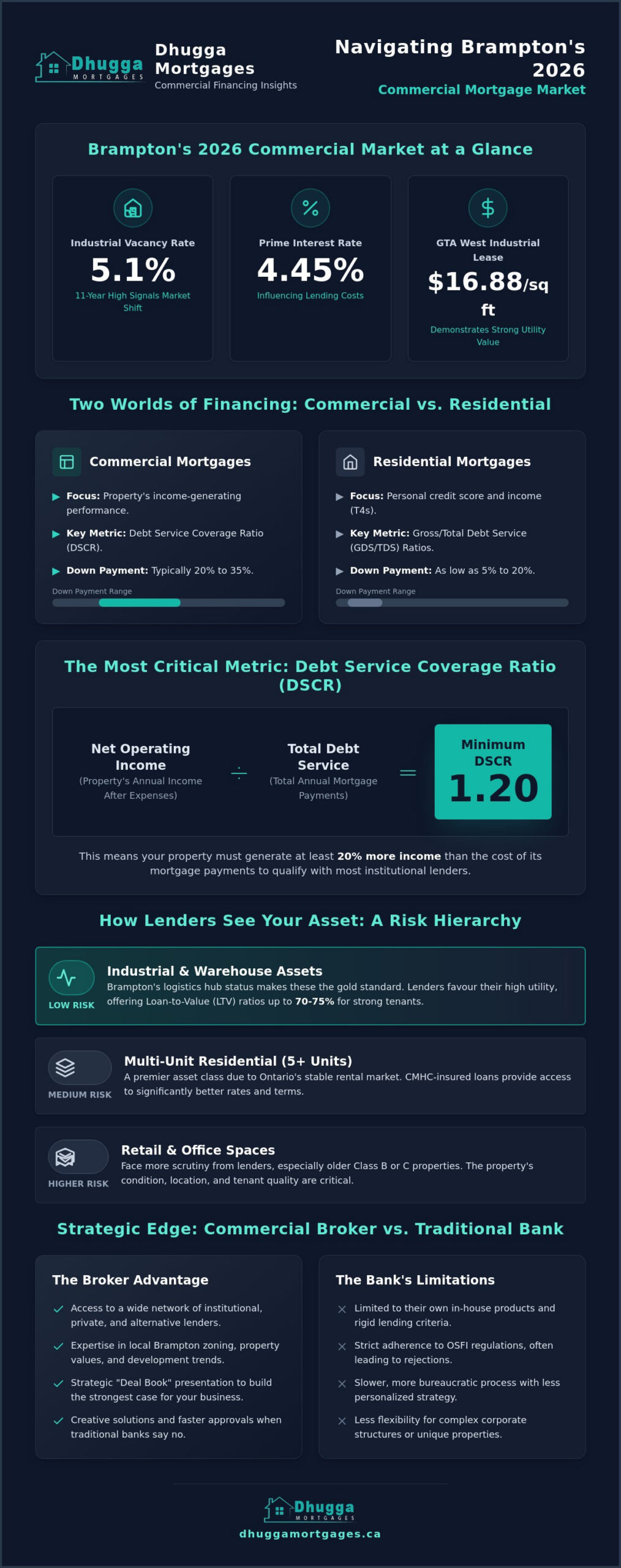

Brampton’s industrial vacancy rate hit an 11-year high of 5.1% in early 2026, signaling a major shift toward a utility-driven market. If you are trying to acquire property or expand operations, you have likely noticed that the financing environment has changed. You need a commercial mortgage broker Brampton who understands that “A” lenders have tightened their grip, often leaving business owners frustrated by rigid income requirements and high conventional rates.

It is exhausting to navigate the new OSFI regulations that prevent double-counting income while managing a Prime rate of 4.45%. You deserve a proactive partner who cuts through the noise of industrial zoning and complex corporate applications. This guide will help you master the 2026 lending market to secure the capital your business needs to thrive. We will show you how to bypass bank rejections through private lenders, streamline your approval process, and use refinancing to lower your monthly overhead.

Key Takeaways

- Understand how 2026 market shifts and new OSFI regulations impact your ability to qualify for industrial or retail properties.

- Learn why property type dictates your interest rate and how to position your asset to minimize lender risk.

- Discover how a commercial mortgage broker Brampton provides a strategic edge by accessing private funds when traditional banks decline.

- Master the “Deal Book” strategy to present a high-impact executive summary that fast-tracks your financing approval.

- Leverage local expertise and a streamlined process to secure competitive financing for your business growth in the GTA.

The Evolution of Commercial Real Estate in Brampton for 2026

Brampton is no longer just a bedroom community; it is a powerhouse in the Ontario economy. In 2026, a commercial mortgage serves as the primary debt-based funding tool for businesses looking to own their space. These loans are specifically designed for income-producing properties. This includes everything from retail plazas to massive logistics hubs. While residential loans focus on your personal credit score, commercial financing is about the property’s performance. Brampton remains a top-tier investment centre because of its strategic location. We see a clear trend toward mixed-use developments and industrial-logistics assets. With GTA West industrial net lease rates holding at $16.88 per square foot, the potential for long-term growth is undeniable. Investors are moving away from speculative growth and focusing on utility-driven value.

Why Business Owners Realize the Value of a Brampton Broker

Local knowledge is your biggest asset. Brampton’s industrial market is stabilizing, but zoning bylaws remain complex and specific to the region’s infrastructure. A Commercial mortgage broker understands these local nuances. They know how the logistics-heavy economy impacts property values in the 400-series highway corridors. You need a partner who can interpret development trends and ensure property appraisals are accurate. A commercial mortgage broker Brampton doesn’t just find a rate; they build a case for your business. They ensure your application reflects the true utility-driven value of your investment in today’s market. This proactive approach is what separates a fast approval from a flat rejection.

Commercial vs. Residential: Key Differences You Need to Know

The qualification process for business properties is a different beast. Lenders prioritize the Debt Service Coverage Ratio (DSCR) over your personal T4 slips. In 2026, most institutional lenders demand a minimum DSCR of 1.20. This means the property must generate 20% more income than the cost of the mortgage payments. Unlike your home loan, these deals require rigorous environmental assessments. Phase I reports are standard to check for historical contamination risks. Amortization periods and interest structures also vary significantly. Commercial rates often track the 5-year Government of Canada bond yield, which currently sits around 3.1%. Expect to provide a down payment between 20% and 35% for most conventional deals. It is a technical environment that requires a streamlined process to secure the capital you need.

Financing Structures for Different Property Asset Classes

Every commercial property is not treated the same by lenders. Financial institutions categorize risk based on the asset’s liquidity and current market demand. In Brampton, industrial assets are currently the gold standard. Retail and office spaces face more scrutiny, especially Class B or C properties that lack modern amenities. A commercial mortgage broker Brampton helps you identify which category your acquisition falls into and how that affects your down payment requirements. We’re seeing a massive rise in flex-space across the GTA. These units combine warehouse storage with professional office fronts. They’re perfect for small businesses that need logistics space without sacrificing a corporate presence. Lenders look at exit strategies; if a business fails, how easily can the building be repurposed? Industrial buildings are easy to flip to new tenants, which keeps your interest rates more competitive.

Industrial and Warehouse Financing in the Brampton Hub

Brampton is Canada’s logistics heart. Lenders favour industrial assets here because the vacancy rate remains manageable at 5.1% as of early 2026. If you’re looking for warehouse acquisitions or expansion projects, expect terms that reflect this stability. Institutional lenders often offer Loan-to-Value (LTV) ratios up to 70% or 75% for strong industrial tenants. You must follow Ontario’s mortgage brokering regulations to ensure your financing is handled by a licensed professional who understands these high-demand zones. Lenders prioritize clear ceiling heights and loading dock configurations. A warehouse with 24-foot clear height is significantly more attractive to a lender than an older unit with low ceilings. High utility equals lower risk.

Multi-Unit Residential and CMHC Insured Loans

Multi-family properties with five or more units are a premier asset class for 2026. The rental market in Ontario continues to show long-term growth despite the 2.1% rent increase cap. You can qualify for significantly lower interest rates by using CMHC insurance programs. These government-backed loans offer extended amortizations and higher LTVs that conventional loans can’t match. It’s a strategic move for investors seeking stability in a post-2025 economy. Qualifying for CMHC often requires meeting specific energy efficiency or affordability criteria, but the payoff is a rate that can be 1% lower than standard commercial products. If you want to explore these specific asset classes, you can speak with our team to see which financing structure fits your growth plan. We focus on speed and removing the complexity of these high-unit applications.

Broker vs. Bank: Analyzing the Best Path for Your Investment

Choosing between a bank and a broker determines your deal’s success. Major Canadian banks offer the lowest rates. However, they’re often the most restrictive. If you are a self-employed business owner in Brampton, you’ve likely faced a “no” from your local branch. This is where a commercial mortgage broker Brampton shifts the power back to you. We don’t just ask one bank for a favour. We force credit unions, trust companies, and private funds to compete for your business. This competition drives down your rate and improves your terms. It’s about creating an “edge” in a crowded market. You gain access to a broad lender network that looks beyond a simple credit score to see the true potential of your business operations.

The Role of Private Mortgage Lenders in Ontario

Sometimes speed is more important than the lowest possible rate. Private financing is a strategic tool for bridge loans or quick closings when a bank’s 60-day window is too slow. It’s about the “now.” You can use alternative funds to secure a property today and then transition back to a traditional bank once your financials are seasoned. For a deeper look at these alternative paths, explore our guide on private mortgage lenders Ontario. These lenders focus on the asset’s value rather than just your personal tax returns. It’s about flexibility and immediate action. We use these funds to bridge the gap while you organize long-term “A” financing, ensuring you never miss a property acquisition due to bank delays.

Traditional Bank Requirements and “A” Lending Criteria

If your business has clean financial statements and strong corporate credit, the “A” lender path is viable. These institutions look for a stable Debt Service Coverage Ratio (DSCR) and a proven track record of profitability. They’re slower. They require more paperwork. But they offer the security of long-term, low-interest funding. A commercial mortgage broker Brampton acts as your advocate here. We package your “Deal Book” so it fits the bank’s strict criteria the first time. This prevents the back-and-forth delays that kill most commercial deals. We ensure your application is bank-ready before it ever hits an underwriter’s desk. Banks prioritize stability. They want to see that your business can weather the 4.45% Prime rate without breaking a sweat. We help you demonstrate that resilience through professional financial presentation.

The Step-by-Step Roadmap to Commercial Approval

Speed is the ultimate currency in commercial lending. A well-oiled machine gets the deal done while others are still waiting for a callback. Your commercial mortgage broker Brampton handles every technical hurdle through a proven five-phase roadmap designed for efficiency. This process removes the guesswork and puts you in a position of strength before you ever talk to a lender.

Phase 1 begins with a pre-consultation to define your specific financing goals. We identify your borrowing capacity and target lenders that align with your property type. Phase 2 is the creation of your “Deal Book.” This is a high-impact executive summary that frames your business’s strengths for the underwriter. Phase 3 involves the submission and negotiation of the Letter of Intent (LOI). We ensure the terms favour your long-term cash flow. Phase 4 covers due diligence, including professional appraisals and environmental assessments. Phase 5 is the final commitment. We drive the legal process to ensure funding happens exactly when you need it.

Essential Documentation for Business Owners and Corporations

Lenders in 2026 are meticulous about their records. You must provide two to three years of audited or review-engagement financial statements to prove stability. If you are financing an income-producing property, current rent rolls and lease agreements are mandatory. All major shareholders must also provide Personal Net Worth statements. This transparency builds immediate trust with the lender. It proves your business can comfortably handle the 1.20 DSCR requirement. Having these documents ready is the fastest way to shorten your approval timeline. It shows you are a professional, low-risk borrower who is ready to act.

Navigating the Application Process in the GTA

The GTA market moves at high velocity. You need to present a business case that emphasizes utility and architectural prominence. Common pitfalls in Brampton include zoning delays or outdated environmental reports that don’t meet modern standards. A proactive approach prevents these closing-day surprises. We identify potential hurdles in the appraisal process early. This keeps your timeline intact and your capital accessible. Don’t let a missing document or a slow appraisal kill your expansion plans. If you are ready to secure your business’s future, contact our team today to fast-track your commercial approval. We focus on results-oriented service that saves you time and money.

Strategic Advantages of Partnering with Dhugga Mortgages

Jaspreet Dhugga has built a reputation on one thing: delivering results when others can’t. As a seasoned commercial mortgage broker Brampton clients trust, our team focuses on removing the friction from corporate lending. We don’t just provide a service. We act as your proactive partner. We understand that your time is your most valuable asset. That is why our communication is direct and our processes are streamlined. We handle the complexity of Brampton’s industrial zoning and corporate applications so you don’t have to. You get peace of mind and the capital you need to grow.

Our reach extends across the entire Greater Toronto Area. We leverage a massive network of over 100 lenders to find your competitive edge. This includes major banks, credit unions, and private funds. This variety ensures that we always have a solution, even for the most complex files. Whether you are a newcomer to Canada or a seasoned investor, we find the path that fits your 2026 business goals. We prioritize speed and reliability to ensure your deal closes on time.

Tailored Financing for Self-Employed and Business Owners

Traditional banks often struggle with non-traditional income. If your tax returns don’t tell the whole story, you need a different approach. We specialize in programs for business owners who prioritize growth over standard T4 slips. We use equity and asset-based lending to secure your approval. This ensures your hard-earned assets work for you. For a deeper look at these options, read our guide on self-employed mortgage Canada. We bridge the gap between your business success and the lender’s requirements.

Fast Approvals and Proactive Debt Management

Speed is our signature. We’ve designed a high-velocity workflow to reduce your stress and save you time. This isn’t just about new acquisitions. We also help you refinance your mortgage in Ontario to unlock vital business capital. Accessing your existing equity can provide the fuel needed for expansion or debt consolidation. The Dhugga Mortgages advantage is simple. We do the heavy lifting. We manage the paperwork and the negotiations. You focus on running your business. We ensure your financing is a strategic benefit, not a hurdle.

Take Command of Your 2026 Business Financing

Brampton’s commercial landscape is moving toward utility-driven value and specialized logistics hubs. You now have the roadmap to navigate high interest rates and strict “A” lender requirements. Success in this market requires more than just an application; it requires a professional presentation and a massive lender network. Partnering with a seasoned commercial mortgage broker Brampton ensures you have the edge needed to outpace the competition. We specialize in both institutional and private lending sectors to provide the flexibility your business growth demands.

Dhugga Mortgages is independently owned and operated under the Mortgage Alliance brand. We bring a proven track record across the Brampton, Mississauga, and Toronto markets. Our streamlined process removes the complexity from your corporate files so you can focus on your operations. Don’t let bank delays or rigid criteria stall your momentum. Secure your Brampton business financing today with Dhugga Mortgages. It’s time to unlock the capital your business deserves. We’re ready to act when you are.

Frequently Asked Questions

How much down payment is required for a commercial mortgage in Brampton?

Most lenders require a down payment between 20% and 35% for commercial properties. However, owner-occupied businesses with strong financials may qualify for higher leverage, sometimes reaching up to 100% loan-to-value. Your commercial mortgage broker Brampton will help you determine which bracket your specific property falls into based on its utility and income potential.

What are the current commercial mortgage rates in Ontario for 2026?

Conventional commercial mortgage rates in early 2026 range from 5.52% to 8.81% depending on the asset class and risk profile. Multi-family loans for larger investments currently start around 5.57%. These rates are influenced by the 5-year Government of Canada bond yield, which sits at approximately 3.1%, and the Prime rate of 4.45%.

Can I get a commercial mortgage if I am self-employed with no proof of income?

Yes, you can secure financing using alternative or private lending paths that prioritize property equity over traditional T4 slips. We specialize in programs for self-employed individuals who may not show high personal income but have strong business assets. These lenders focus on the property’s value and your business’s cash flow rather than rigid bank requirements.

How long does the commercial mortgage approval process typically take?

A traditional bank approval usually takes between 45 and 60 days from application to funding. This timeline accounts for appraisals, environmental assessments, and legal due diligence. If you need capital faster, private lenders can often fund a deal within two weeks. We streamline the process to ensure no time is wasted on unnecessary paperwork.

What is a Debt Service Coverage Ratio (DSCR) and why does it matter?

The Debt Service Coverage Ratio (DSCR) measures a property’s ability to cover its mortgage payments using its net operating income. Most lenders in 2026 require a minimum DSCR of 1.20. This means the property must earn 20% more than the annual debt cost. It’s the primary metric used by a commercial mortgage broker Brampton to determine your loan amount and interest rate.

Are there specific grants or programs for first-time commercial buyers in Brampton?

There are no specific government grants for first-time commercial buyers similar to residential programs, but owner-occupied financing offers significant advantages. Businesses that occupy at least 51% of their property can often access higher loan-to-value ratios. This reduces the initial capital required to move from leasing to owning your own headquarters in the GTA.

What is the difference between a commercial mortgage and a small business loan?

A commercial mortgage is a debt-based tool secured specifically by income-producing real estate. In contrast, a small business loan is typically used for operational costs, inventory, or equipment and may be unsecured. Mortgages offer longer amortization periods and lower interest rates because the lender has the property as collateral to mitigate their risk.