Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Commercial Mortgage Rates Toronto: Your 2026 Strategic Financing Guide

- Home

- Commercial Mortgage Rates Toronto: Your 2026 Strategic Financing Guide

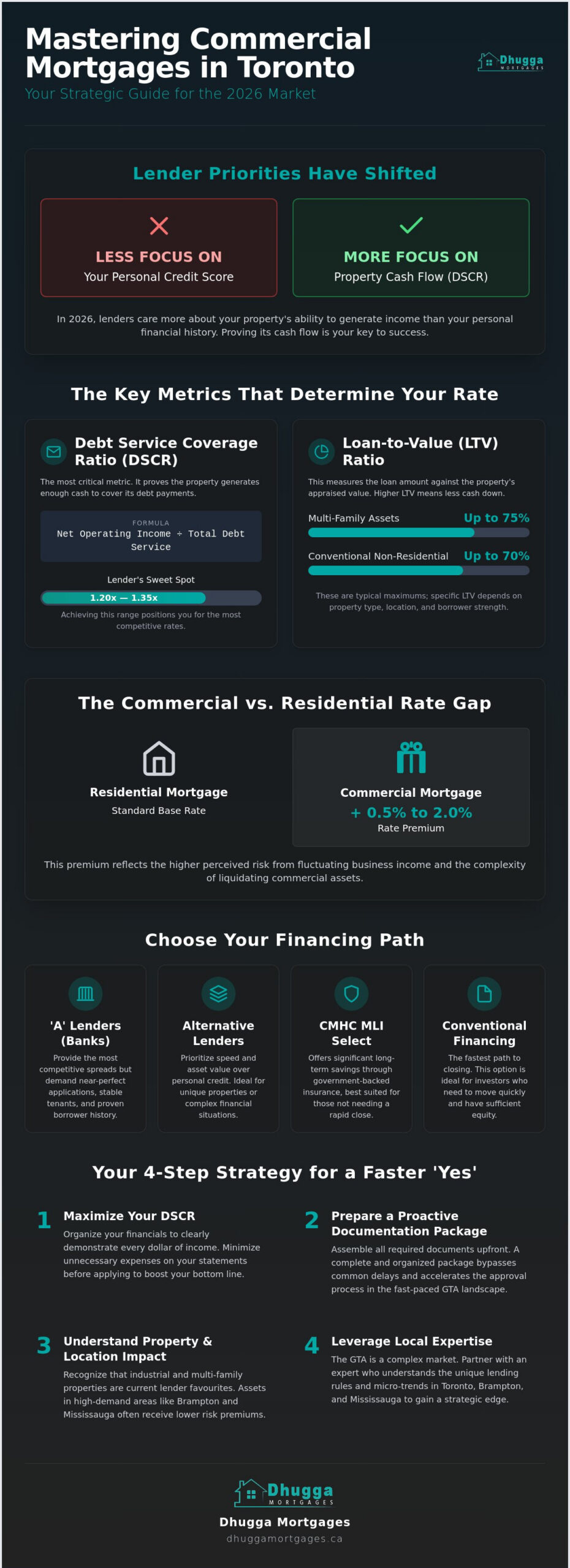

Your credit score isn’t the most important factor in your commercial mortgage application. In the 2026 market, lenders care more about your property’s cash flow than your personal history. It’s a tough reality to face when you’re ready to grow. High barriers to entry and slow closing times often stall even the best investments. You want to secure the best commercial mortgage rates Toronto has to offer, but the choice between fixed and variable options feels like a high-stakes gamble in this economy.

You can stop the guesswork and take control of your financing. This guide provides the strategy you need to master the local lending market. We’ll break down the 2026 environment, where the Bank of Canada policy rate holds steady at 2.25 percent. You’ll learn the difference between CMHC-insured and conventional financing to maximize your cash flow. We cover everything from Debt Service Coverage Ratios to finding a local expert who streamlines your application. Get ready to move fast and secure your edge.

Key Takeaways

- Understand how bond yields and lender spreads influence the commercial mortgage rates Toronto investors encounter in the 2026 market.

- Prioritize your Debt Service Coverage Ratio (DSCR) to prove property income potential and unlock the most competitive terms.

- Compare the long-term savings of CMHC MLI Select against the rapid closing speeds of conventional financing to suit your timeline.

- Organize a proactive documentation package to bypass common delays and realize a faster approval in the fast-paced GTA landscape.

- Leverage local expertise in Toronto, Brampton, and Mississauga to navigate complex lending rules and secure a strategic edge.

Current Landscape of Commercial Mortgage Rates in Toronto

A Commercial mortgage isn’t a one-size-fits-all product. It’s a customized financial tool built for growth. In 2026, the commercial mortgage rates Toronto lenders offer are a calculation of Government of Canada bond yields plus a specific risk spread. This spread is where the negotiation happens. Toronto is a global financial hub. Rates here reflect international capital flows and local economic stability. It’s a sophisticated market that rewards prepared investors.

You have distinct choices in the GTA lending landscape. ‘A’ lenders, such as major banks, provide the most competitive spreads but require nearly perfect applications. They want long-term leases and proven stability. Alternative private options offer a different path. These lenders prioritize speed and asset value over personal credit history. If you have a unique property or a complex financial background, these private sources provide the necessary liquidity. Standard rates don’t exist for unique assets. Your rate is as individual as your business plan.

Why Toronto Market Dynamics Influence Your Rate

Your postal code directly affects your interest costs. Massive industrial demand in Brampton and Mississauga has made these areas favourites for institutional lenders. Low vacancy rates in these hubs translate to lower risk premiums for borrowers. The Toronto retail sector’s 2026 recovery has also eased the pressure on storefront financing. Currently, the Bank of Canada policy rate sits at 2.25 percent. This stability helps you plan with confidence. However, lenders still watch local micro-trends. A tech office in the Downtown Core carries a different risk profile than a manufacturing plant in Vaughan.

Commercial vs Residential: The Interest Rate Gap

Commercial loans carry a premium. You will usually see rates 0.5 percent to 2 percent higher than residential mortgages. Lenders view commercial assets as higher risk. Business income can fluctuate, and large-scale properties are often harder to liquidate than a single-family home. This gap is simply the price of doing business. You can bridge this divide with smart equity management. Many investors use mortgage refinancing in Ontario to tap into residential equity. This allows you to deploy lower-cost capital into your commercial ventures. It’s a proactive way to lower your overall cost of borrowing and boost your cash flow immediately.

How Lenders Determine Your Rate in the GTA

Commercial lending is a sophisticated risk assessment. When you evaluate commercial mortgage rates Toronto lenders provide, you aren’t just looking at a number. You’re looking at how a lender perceives your property’s stability. While residential mortgages rely on personal income, commercial financing focuses on the asset’s performance. The most critical metric is the Debt Service Coverage Ratio (DSCR). Lenders also weigh the Loan-to-Value (LTV) ratio. Conventional non-residential properties typically cap at 70 percent LTV; multi-family assets can reach 75 percent. These standards fluctuate based on broader economic trends. You can track these shifts through Statistics Canada mortgage rate data to see how current benchmarks compare to historical norms.

Borrower experience is the final piece of the puzzle. Lenders want to see a proven track record in property management or business operations. If you’re a seasoned investor with a strong balance sheet, you’ll likely secure ‘A’ rates. First-time commercial buyers might face slightly higher spreads until they prove their reliability. Location within the GTA also plays a massive role. Properties in Toronto’s financial core generally secure better terms than those on the periphery. Core assets hold their value better during market shifts, which reduces the lender’s risk profile.

Mastering the Debt Service Coverage Ratio (DSCR)

Lenders use DSCR to ensure the property generates enough cash to cover its debt. The formula is straightforward: Net Operating Income divided by total debt service. In Toronto, a ratio between 1.2x and 1.35x is the sweet spot. If your property hits this range, you’re positioned for the most competitive rates. To maximize this ratio, organize your financials to show every dollar of income clearly. Minimize unnecessary expenses on your tax returns to boost your bottom line before applying. This simple preparation can significantly lower your interest costs over the life of the loan.

Property Type and Its Direct Impact on Spreads

The asset class determines the floor for your interest rate. Some properties are simply safer bets for banks. Consider these current trends in the Toronto market:

- Industrial and Multi-family: These command the lowest rates due to extreme demand and low vacancy rates across the GTA.

- Special-purpose Real Estate: Hotels, gas stations, and car washes often cost more to finance because they are harder to repurpose.

- Mixed-use Properties: These offer a middle ground, often combining residential stability with retail income potential.

Navigating these categories requires a proactive strategy. If you want to understand how your specific property class impacts your commercial mortgage rates Toronto profile, speaking with a GTA specialist is the fastest way to get a clear answer and move your project forward.

CMHC-Insured vs. Conventional Commercial Financing

Choosing the right financing structure is a strategic decision that directly impacts your long-term cash flow. When you hunt for the best commercial mortgage rates Toronto has available, you will eventually face the choice between CMHC-insured and conventional loans. CMHC-insured mortgages offer the lowest possible interest rates because the government backs the loan. In 2026, the MLI Select program remains the gold standard for multi-family investors. It rewards you for committing to affordability and energy efficiency. These perks come with a trade-off in speed. If you need to close a deal in weeks rather than months, conventional financing is the winner. You can analyze the current spread between these products by reviewing the CMLS Financial Commercial Mortgage Commentary, which details how bond yields influence these specific lending tiers.

There are times when neither path fits a tight deadline. If you are racing to secure a distressed asset or a quick-flip opportunity, private mortgage lenders in Ontario provide the necessary bridge financing. These lenders focus on the asset’s value rather than the bureaucratic requirements of institutional banks. They provide the liquidity you need to seize an opportunity today while you arrange long-term financing for tomorrow. It is about maintaining momentum in a fast-paced market.

The Perks of CMHC Insurance for Multi-Family Assets

CMHC insurance is a game-changer for multi-unit residential properties. It allows for amortization periods of up to 40 years, which significantly lowers your monthly debt service. Because the lender’s risk is mitigated, you can secure a loan-to-value (LTV) ratio as high as 85 percent. This reduces your required down payment for Toronto apartments, allowing you to scale your portfolio faster. The trade-off involves higher upfront application fees and processing times that can stretch several months. You must plan your acquisition timeline with these delays in mind to avoid missing closing dates.

Conventional Financing: Speed and Flexibility

Conventional loans are the preferred choice for retail, office, or industrial acquisitions where speed is paramount. These loans offer greater flexibility and fewer ‘strings attached’ regarding how you manage the property. You won’t have to meet specific affordability quotas or energy audits to qualify. If you are short on liquid capital for a commercial down payment, you can use a debt consolidation mortgage in Canada to unlock equity from other assets. This strategy turns your existing residential equity into a powerful tool for commercial expansion. It allows you to move quickly when the right property hits the market.

Strategic Steps to Secure the Lowest Rate Possible

Don’t wait for a lender to dictate your terms. You need a proactive strategy to win in this market. Securing the best commercial mortgage rates Toronto has to offer requires you to create competition for your business. Most investors make the mistake of approaching a single big bank and accepting the first offer. This is a passive move that costs money. Instead, you should position your property as a low-risk, high-reward asset. A multi-lender strategy forces institutions to tighten their spreads to earn your business. It’s about leverage.

Your goal is to make the approval process as frictionless as possible. Lenders in the GTA are currently processing high volumes of applications. They favour files that are complete, organized, and easy to underwrite. If a lender has to hunt for your documentation, they’ll likely increase the risk premium or simply move to the next file. Speed and clarity are your best allies. By presenting a polished package, you demonstrate the professional management that banks crave. It shows you’re ready to close.

Preparing Your Commercial Loan Package

Lenders hate surprises. You must provide a clear financial picture from the start. Gather three years of audited financial statements and current, verified rent rolls. For multi-family or retail assets, the rent roll is the heartbeat of the deal. It proves the cash flow discussed in earlier sections. You also need an up-to-date Phase 1 Environmental Site Assessment (ESA). In Toronto’s industrial and urban zones, an outdated ESA is a deal-killer. Finally, keep your business plan staccato. It should be punchy, direct, and focused on the bottom line. Tell the lender exactly how you’ll maintain the Debt Service Coverage Ratio (DSCR) over the term.

The Broker Advantage in the 2026 Rate Market

A broker is your high-speed facilitator in a complex landscape. We access wholesale rates that aren’t advertised to the general public. This gives you an immediate edge. We also specialize in navigating complex files, particularly for self-employed professionals in Canada who may not fit the rigid boxes of traditional banks. While a bank-direct application might stall in a corporate queue, a broker-facilitated deal moves with urgency. We know which lenders are currently aggressive on specific asset classes, saving you weeks of wasted effort. If you’re ready to see what your property can actually secure, connect with our team for a fast rate analysis and start your application today.

Dhugga Mortgages: Your Toronto Commercial Facilitator

Dhugga Mortgages is your high-speed facilitator in a complex market. We are an independently owned Mortgage Alliance franchise led by Jaspreet Dhugga. Our team specializes in the GTA. Toronto, Brampton, Mississauga, and Caledon are our backyard. We know which lenders are hungry for industrial deals in Peel and which ones prefer retail in the Core. This local knowledge is your secret weapon. We don’t just submit files. We advocate for your success. Our team works with a broad lender network of over 100 institutional and private options. We’ve built a reputation on reliability and speed. You need a partner who values your time as much as you do. We are that partner. We provide the professional edge you need to win.

Securing the best commercial mortgage rates Toronto offers requires a proactive approach. We take charge of the process from the first call. Our goal is to instill confidence through every stage of your application. We remove the complexity. We provide peace of mind. You won’t find passive advisors here. You’ll find a bold, action-oriented guide ready to streamline your financing. We handle the heavy lifting so you can focus on building your business or expanding your portfolio. It is about momentum. It is about results.

Custom Solutions for Complex Commercial Files

Complex situations are where we shine. Many traditional banks turn away self-employed or newcomer applicants because they don’t fit a standard box. We don’t. Our expertise in helping newcomers to Canada navigate the lending market is unmatched. We understand that your financial history might be global, not just local. For value-add or construction projects, we deploy tailored private lending options. These provide the bridge you need to realize your property’s full potential. It’s about ROI. It’s about results. We remove the barriers to entry that stall other investors. Our solutions are as modern and timelier than the competition.

Start Your Toronto Commercial Application Now

The 2026 market is stable but competitive. Don’t let opportunity slip away while you wait for a bank callback. Our process is streamlined. It’s built for the modern investor. We provide clear, digestible updates at every stage. No jargon. No confusion. Just a clear path to closing. To get started, simply reach out for a fast rate analysis. We’ll review your property’s income potential and your financial goals immediately. Lock in your strategy now. Call our office or book an online consultation. We are ready to take charge of your file. Secure your competitive Toronto commercial rate with Dhugga Mortgages today!

Take Control of Your 2026 Financing Strategy

Success in the Toronto market requires more than just watching the numbers. You need to master your property’s cash flow and pick the right lending vehicle for your specific goals. Whether you choose the long-term savings of CMHC or the rapid speed of conventional debt, your strategy must be proactive. We’ve shown you how commercial mortgage rates Toronto lenders offer are determined by your Debt Service Coverage Ratio and asset type. Now it’s time to put that knowledge into action and secure your next investment.

Dhugga Mortgages is an independently owned and operated Mortgage Alliance franchise. We bring deep expertise to the Toronto, Brampton, and Mississauga markets. Our team provides immediate access to both private and institutional lender networks. We remove the complexity so you can move fast and secure your edge in a competitive landscape. Stop waiting for the big banks to call you back. Take charge of your business investment today. Get a proactive commercial rate quote from Dhugga Mortgages today! You have the strategy. Now you need the partner to execute it. We look forward to building your success in the GTA.

Frequently Asked Questions

What is a typical commercial mortgage rate in Toronto for 2026?

Conventional commercial mortgage rates Toronto investors encounter in July 2026 typically range from 5.52 percent to 8.81 percent. These rates depend heavily on the property type and your specific credit profile. CMHC-insured options offer lower rates, usually calculated as a premium of 0.4 percent to 2 percent over the Canadian Mortgage Bond yield. The Bank of Canada policy rate currently holds steady at 2.25 percent, providing a stable foundation for variable-rate products.

How much down payment is required for a commercial property in the GTA?

Most conventional commercial deals in the GTA require a down payment of 25 percent to 30 percent. Lenders typically cap their Loan-to-Value ratio at 70 percent for office or retail spaces and 75 percent for multi-family buildings. If you qualify for CMHC insurance, you can secure up to 85 percent financing. This reduces your upfront capital requirement to just 15 percent, allowing you to scale your portfolio faster.

Can I get a commercial mortgage if I am self-employed with limited income proof?

Yes, you can. Commercial lending focuses primarily on the property’s ability to generate income rather than your personal tax returns. Lenders look at the Debt Service Coverage Ratio to ensure the asset pays for itself. We specialize in helping self-employed professionals present their files effectively to both institutional and private lenders. We prioritize the strength of the asset to bypass traditional income hurdles.

What is the difference between a fixed and variable commercial rate?

A fixed rate provides total payment certainty for the duration of your term, usually ranging from three to ten years. It protects you from market volatility. A variable rate fluctuates based on the prime rate, which is currently 4.45 percent. While variable options can offer lower initial costs, they carry the risk of increasing if the Bank of Canada adjusts its policy. Your choice depends on your specific risk tolerance and cash flow needs.

How long does it take to close a commercial mortgage in Toronto?

Closing typically takes between 45 and 90 days in the Toronto market. Conventional loans through alternative or private lenders generally move much faster than institutional bank files. CMHC-insured mortgages often take the longest due to the rigorous government audit process. You can speed up your timeline by having your Phase 1 Environmental Site Assessment and three years of financial statements ready before you apply.

What are the common fees associated with commercial lending in Ontario?

You should budget for several standard costs beyond your interest rate. These include property appraisal fees, environmental report costs (Phase 1 ESA), and legal fees for both your counsel and the lender’s counsel. Most commercial deals also involve lender or broker processing fees, which are typically a percentage of the total loan amount. These costs vary based on the complexity and size of your specific transaction.

Does Dhugga Mortgages handle private commercial lending for bad credit?

We do. Our private mortgage solutions focus on the equity in your property and the asset’s overall value rather than just your credit score. This is an ideal path for investors looking to bridge a gap or revitalize a distressed property. We use our broad network of private lenders to find flexible terms that traditional banks won’t offer. Our goal is to provide the liquidity you need to move forward immediately.

Are commercial mortgage rates in Mississauga different from Toronto?

The base commercial mortgage rates Toronto and Mississauga lenders offer are generally identical. However, lender spreads can tighten in Mississauga for specific assets like high-demand industrial warehouses. These micro-market dynamics mean a property in a prime Mississauga hub might secure slightly better terms than a similar asset in a less active zone. We use our local expertise across the entire GTA to find these specific competitive advantages for your file.