Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Home Equity Loan Toronto: The 2026 Guide to Unlocking Your Property Value

- Home

- Home Equity Loan Toronto: The 2026 Guide to Unlocking Your Property Value

The big banks favour their own rigid rules, but your property is a high-performance financial tool that should be working for you right now. In a city where the cost of living keeps climbing, securing a home equity loan Toronto homeowners can rely on is the fastest way to regain control of your cash flow. You’ve done the hard work of building value in the GTA. It’s time to use it.

We recognize the frustration of passing strict stress tests while juggling high-interest credit cards. It’s a common Toronto story. This guide provides the expert local guidance you need to consolidate debt, renovate your space, or finally buy that second investment property. We’ll show you the most efficient path to liquidity without the usual bank delays.

We’re breaking down the 2026 lending environment, including the OSFI mandated 65% LTV cap on revolving credit and the latest Bank of Canada rate impacts. You’ll get a clear, direct look at the numbers and the strategy required to win in today’s market. Let’s get to work.

Key Takeaways

- Understand how record property growth in the GTA translates into immediate borrowing power under the latest 2026 regulations.

- Compare the pros and cons of a HELOC versus a second mortgage to determine which structure protects your cash flow best.

- Review the essential “Big Three” criteria lenders use to approve a home equity loan Toronto homeowners need for renovations or investments.

- Follow a clear, step-by-step roadmap to gather your documentation and secure a fast approval through our extensive lender network.

- Learn how to navigate the 80% LTV rule and the new OSFI guidelines to maximize your accessible capital while minimizing interest costs.

Understanding the Home Equity Loan in Toronto: 2026 Edition

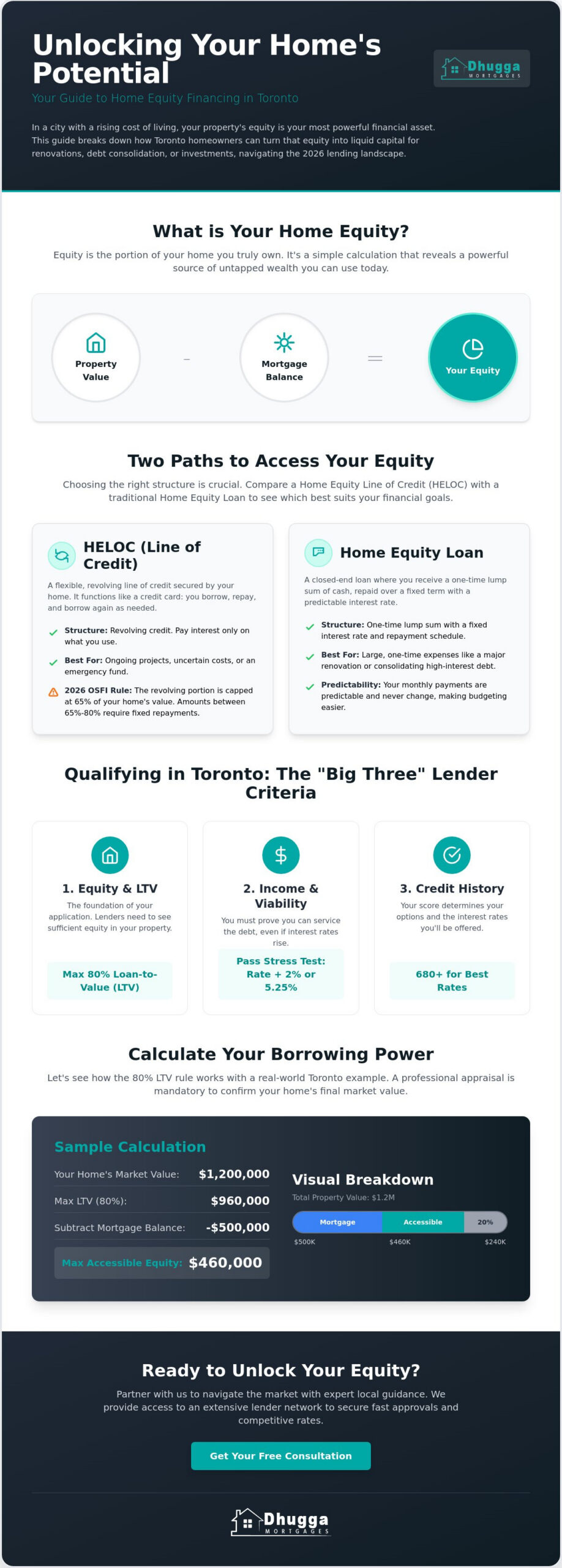

Your home is more than a place to live. In the GTA, it’s your most powerful financial asset. Equity is the simple math of your success. Take your property’s current market value and subtract your remaining mortgage balance. That number is your equity. It represents the portion of the home you truly own. For most people, it’s a massive source of untapped wealth. We help you access it without the red tape.

Toronto homeowners have seen record equity growth lately. High demand and limited supply have pushed valuations higher across the city. This has created a unique situation. Many families are now house rich but cash poor. You might live in a million-dollar home but feel the squeeze of the rising cost of living. A Home equity loan solves this. It turns your bricks and mortar into liquid capital you can use today. No more waiting for a sale to see the benefit of your investment.

The Difference Between a HELOC and a Home Equity Loan

Structure matters. A home equity loan is a closed-end product. You receive a one-time lump sum of cash. It’s predictable. You get a fixed interest rate and a set repayment schedule. This is the perfect choice for one-time costs like a major basement renovation or consolidating a specific block of high-interest debt. You know exactly what your payment is every month.

A HELOC is different. It’s a revolving line of credit. It works like a giant credit card secured by your house. You only pay interest on what you use. In the 2026 lending environment, OSFI regulations are strict. The revolving portion of a HELOC is capped at 65% of your home’s value. Anything between 65% and 80% must follow an amortizing payment schedule. We’ll help you decide which path fits your cash flow goals.

Why Toronto Real Estate Values Matter for Your Loan

Your neighbourhood drives your borrowing power. An appraisal for a detached home in Etobicoke looks very different than a condo evaluation in Scarborough. Lenders look at local trends and recent sales on your specific street. They want to see stability and demand. Property type is a major factor too. Detached houses often provide more leverage than older condos with high maintenance fees. In the Toronto market, Loan-to-Value (LTV) represents the percentage of your home’s appraised value that a lender is willing to finance, typically capped at 80% for combined mortgage and equity products. We’ll help you maximize that percentage to get the most out of your home equity loan Toronto investment.

Qualifying for Equity Financing: What Toronto Lenders Look For

Approval isn’t a mystery. It’s a calculation. Lenders in the GTA focus on the “Big Three” criteria: equity, income, and credit history. While your property value is the foundation, your ability to carry the debt is what closes the deal. In 2026, the mortgage stress test remains a significant hurdle. You must prove you can handle payments at your contract rate plus 2% or a floor rate of 5.25%, whichever is higher. This ensures you’re protected if rates shift, but it also means your debt-to-income ratio must be airtight.

Property condition is often overlooked. A home in a prime Liberty Village or High Park location is great, but major structural issues can stall a home equity loan Toronto application. Lenders want to know the asset is marketable. An appraisal isn’t just about the number. It’s about the safety and viability of the collateral. Borrowing against home equity requires a clear understanding of these regulatory and physical standards before you apply. We ensure your file is presented in the best possible light to avoid unnecessary rejections.

LTV Ratios and Borrowing Limits

Math defines your limit. In Ontario, the standard Loan-to-Value (LTV) limit is 80%. To find your borrowable amount, multiply your home’s current market value by 0.8 and subtract your existing mortgage balance. For example, on a $1.2 million home with a $500,000 mortgage, your maximum equity access is $460,000. Big banks are strict about this ceiling. However, private lenders in Toronto often offer more flexibility, sometimes allowing for higher LTV ratios if the property is in a high-demand neighbourhood. A professional appraisal is mandatory to lock in these figures. It provides the objective data lenders need to move fast.

Credit Score and Income Nuances

Your credit score tells a story. A score of 680 or higher usually unlocks the most competitive rates from major banks. If your score is closer to 600, B-lenders become the strategic choice. They offer lower barriers to entry while still providing professional terms. Income is the other half of the equation. Traditional T4 employees have it easiest, but Toronto is a city of entrepreneurs. We specialize in self-employed mortgage Canada solutions that use bank statements or stated income to prove affordability. Non-traditional income streams like rental suites or dividends are also valid if documented correctly. If you’re unsure where you stand, reach out for a quick equity review to see your options.

HELOC vs. Second Mortgage: Which is Right for You?

Choosing the wrong structure costs money. A HELOC and a second mortgage serve different purposes. One is a flexible tool. The other is a strategic strike. For a home equity loan Toronto homeowners must weigh immediate needs against long-term costs. Setup fees for HELOCs are typically lower. However, the interest rate is variable. It fluctuates with the prime rate. A second mortgage usually carries a higher interest rate but offers the security of a fixed term. Over a five-year period, the total cost of borrowing depends on your discipline and market volatility. We help you run the numbers to find the most profitable path.

Risk management is critical. Banks have the power to freeze or reduce your HELOC limit. If Toronto property values experience a sudden dip, your safety net could vanish. This “callable” nature of revolving credit is a major disadvantage. A second mortgage is different. It’s a lump-sum contract. The funds are yours. It provides the certainty you need for urgent debt consolidation or major investments. Before you decide, it’s helpful to review What Is A Home Equity Loan? and how it compares to revolving credit lines. We’ll ensure you choose the product that keeps you in control.

The Strategic Use of a Second Mortgage

Protect your existing low rate. If your first mortgage is locked in at a historical low, don’t touch it. Refinancing triggers massive penalties. A second mortgage sits behind your current loan. It lets you access equity without losing your primary advantage. We often connect clients with private mortgage lenders Ontario wide to bypass bank delays. Speed is the priority here. While big banks take weeks to process paperwork, private funding can happen in a matter of days. It’s the most efficient path for time-sensitive opportunities and urgent cash needs.

HELOC: The Flexible Safety Net

Use credit as you need it. A HELOC is ideal for multi-stage renovations. Draw funds for the kitchen today. Use the rest for the landscaping next year. It’s a revolving door of capital. You can combine it with your existing mortgage for a “readvanceable” limit. This means as you pay down your principal, your credit limit grows. But stay disciplined. The temptation to spend can lead to a cycle of interest-only payments. Use it as a strategic tool, not a lifestyle subsidy. We’ll help you build a plan that balances flexibility with aggressive debt reduction and long-term wealth building.

The Step-by-Step Process to Secure Your Loan in Toronto

Efficiency is the foundation of our process. We don’t believe in long waits or unnecessary hurdles. Securing a home equity loan Toronto homeowners can use to their advantage begins with a direct strategy session. We’ll assess your current equity position and align it with your specific financial goals. Whether you’re looking to invest in a new venture or simplify your monthly obligations, we determine the most effective path forward in minutes. Our team takes charge of the logistics so you can focus on your next move.

Gathering Your Documentation

Speed depends on your preparation. We require a concise set of documents to move your file to the approval stage. You’ll need your most recent property tax bill, your current mortgage statement, and valid government ID. Income verification is also essential. T4 employees should have recent pay stubs ready, while business owners should organize their bank statements and T1 Generals. If your goal is a debt consolidation mortgage Canada homeowners frequently use for high-interest relief, gather your latest credit card and loan statements as well. Having this package ready ensures we can bypass typical bank delays and move straight to the underwriting phase. We value your time and aim for a “one-and-done” document collection process.

The Appraisal and Legal Closing

Your appraiser is the key to unlocking maximum capital. To ensure your Toronto property is valued correctly, take a proactive approach before they arrive. Clear any clutter. Ensure all rooms are accessible. Provide a written list of recent improvements like new roofing, HVAC updates, or kitchen refreshes. These details matter for the final valuation and help the appraiser justify a higher price point in your specific neighbourhood. Once the appraisal is in, we move to the legal review. A specialized lawyer will handle the registration of the loan and the distribution of funds. You’ll attend a brief meeting to sign the final documents. You should expect to cover standard legal fees, disbursements, and title insurance. The typical timeline from your initial application to cash-in-hand is usually between 10 and 14 business days. We manage every detail to keep this window as tight as possible, ensuring you get your funds exactly when you need them. Apply for your Toronto equity review today to get the process started.

Why Partner with Dhugga Mortgages for Toronto Equity

Experience matters in a market as fast-moving as the GTA. We don’t just process paperwork; we navigate the specific nuances of Toronto real estate for you. Whether it’s a semi-detached in Leslieville or a luxury build in Oakville, we understand how local demand affects your borrowing power. Securing a home equity loan Toronto homeowners can actually use requires more than a standard bank application. It requires a partner who knows the landscape and acts with speed. We bridge the gap between your property value and your financial goals.

Our results-oriented approach removes the friction from your financial planning. We prioritize transparency and direct communication. You won’t find passive advisors here. We are proactive guides who take charge of the process from the first consultation to the final funding. For self-employed individuals or those facing credit challenges, we build customized strategies that big banks simply can’t match. We look at the whole picture, not just a credit score. This flexibility is why we are a trusted name in GTA equity financing. We deliver the edge you need.

Beyond the Big Banks

Big banks are built for the average borrower, but Toronto is a city of unique financial stories. When your primary bank says “no” due to strict stress tests or non-traditional income, we find the “yes”. Our massive lender network includes private and alternative options that look beyond the rigid boxes of traditional institutions. We act as your action-oriented advocate. Our commitment is to remove complexity. We translate financial jargon into clear, actionable steps. You get the advantage of a seasoned guide who knows exactly which lender will value your specific situation. We make the impossible possible.

Your Next Steps to Financial Freedom

Your property is likely your largest investment. It’s time to make it work for you. A simple equity review can reveal thousands in accessible capital. This liquidity allows you to pay off high-interest debt, fund a major renovation, or secure your next investment property. Don’t let your wealth sit idle in your walls. A strategic move today can significantly lower your monthly payments and increase your long-term net worth. We provide the roadmap; you reap the rewards. Book a strategy session to realize your property’s true potential and regain control of your monthly cash flow. Get started with your Toronto home equity review today!

Take Command of Your Financial Future Today

Your property is your greatest strategic advantage in the GTA. Don’t let it sit idle while high interest rates eat into your cash flow. You now have the roadmap to navigate the 2026 OSFI rules and the technical knowledge to choose between a flexible HELOC and a stable second mortgage. It’s about making your wealth work as hard as you do. You’ve built the equity. Now it’s time to use it.

Securing a home equity loan Toronto homeowners can rely on requires more than just a standard application. It requires expert local knowledge of specific GTA neighbourhoods and immediate access to an extensive network of private and alternative lenders. We provide a highly efficient, results-oriented process that bypasses traditional bank delays. We remove the complexity so you can focus on your goals. Our team is ready to act now.

Stop managing debt and start building wealth. Take the first step toward a more liquid, flexible financial life. Unlock Your Toronto Home Equity Now. Your financial freedom is closer than you think. Let’s get to work.

Frequently Asked Questions

Is a home equity loan better than a personal loan in Toronto?

Yes, usually. A home equity loan Toronto homeowners choose is secured by property, which drastically lowers the interest rate compared to unsecured personal loans. You also gain access to much higher borrowing limits. Personal loans are faster to set up but often come with double-digit rates and shorter repayment windows. If you have significant equity, using your home as collateral is the more cost-effective move for long-term savings.

Can I get a home equity loan with a bad credit score in Ontario?

Yes, you can. We look beyond the credit score. While big banks require a score of 680 or higher, private and alternative lenders in Ontario prioritize the equity in your home. If your property has value and you have at least 20% equity, we can find a solution. These “B-side” loans help you consolidate debt and rebuild your credit over time. We focus on your property’s potential, not just your past.

How much does it cost to set up a home equity loan?

Expect to cover standard setup fees. Industry data from 2026 suggests borrowers should budget between $1,000 and $2,000 for appraisal fees, title searches, and legal registration. A professional appraisal usually costs $300 or more depending on the property type. These costs are often rolled into the loan itself so you don’t have to pay out of pocket. We ensure every cost is transparent and disclosed upfront with no hidden surprises.

What is the maximum LTV for a home equity loan in Toronto?

The maximum total Loan-to-Value (LTV) is 80%. This includes your existing mortgage and the new equity loan combined. Under 2026 OSFI regulations, the revolving portion of a HELOC is capped at 65% of your home’s value. Any amount between 65% and 80% must be on a fixed repayment schedule. We help you calculate your specific limit to ensure you maximize your borrowing power while staying within provincial guidelines.

Will a home equity loan affect my current mortgage rate?

No, it won’t. A home equity loan or a second mortgage is a separate agreement that sits behind your primary mortgage. Your original contract, interest rate, and term remain exactly as they are. This is a major advantage if you currently have a low-rate mortgage you don’t want to break. You get the cash you need without triggering the massive prepayments or penalties associated with a full mortgage refinance.

Can I use a home equity loan to buy another investment property?

Yes, this is a very common strategy for GTA investors. You can use a home equity loan Toronto homeowners leverage to cover the down payment and closing costs on a second property. It’s a fast way to grow your real estate portfolio without waiting years to save cash. Additionally, the interest on the equity loan may be tax-deductible if the funds are used specifically for investment purposes. Consult your tax professional for details.

How long does it take to get funds from a home equity loan?

The typical timeline is 10 to 14 business days. This includes the initial application, the professional appraisal, and the legal closing at a lawyer’s office. If you need funds faster, private lender options can often be funded in as little as 3 to 5 business days. We drive the process forward to eliminate bank delays. Our goal is to get the capital into your hands exactly when you need it most.

What happens if Toronto property values decrease after I take the loan?

Your loan terms stay the same. As long as you make your payments, the lender cannot demand full repayment just because market values dipped. However, a HELOC is a “callable” loan. This means if values drop significantly, a bank might reduce your credit limit or freeze the account to manage their risk. This is why a fixed home equity loan is often a safer, more predictable choice during periods of market volatility.