Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Self-Employed Mortgage Canada: The 2026 Strategic Guide for Business Owners

- Home

- Self-Employed Mortgage Canada: The 2026 Strategic Guide for Business Owners

Why does your bank claim you can’t afford a home when your business is thriving? It’s a common frustration. You’ve built a successful company. You’ve optimized your taxes. Now, those same write-offs are slashing your borrowing power. Securing a self-employed mortgage Canada shouldn’t feel like a penalty for your success. You deserve a lender that understands the reality of entrepreneurship beyond a single tax line. We know the anxiety that comes with income fluctuations and overwhelming documentation requirements.

You can master these complexities and secure the most competitive rates in today’s market. This guide provides the strategic edge you need. We’ll show you how to build a Business Narrative that lenders actually respect. You’ll discover how to access stated income programs and navigate the 2026 OSFI changes with confidence. We’ll break down exactly how to leverage the current 2.25% Bank of Canada policy rate to get you into that GTA home. It’s time to stop the paperwork anxiety and start making moves. Learn how to turn your professional success into personal property today.

Key Takeaways

- Understand how lenders use the 2-year average and 15% top-up to calculate your true borrowing power.

- Compare traditional A-lenders with flexible B-lenders to find the right balance between rates and documentation.

- Prepare your Business Narrative with a complete checklist of tax and corporate documents to avoid application delays.

- Navigate the 2026 market to secure a self-employed mortgage Canada with the most competitive rates available today.

- Leverage local expertise to handle unique appraisal values across the GTA and access specialized lending pools.

Why Getting a Mortgage While Self-Employed in Canada Feels Different in 2026

Banks love T4 slips. They want predictable, steady income that fits into a neat little box. If you’re an entrepreneur, you don’t fit that mold. This is the “T4 Bias.” A traditional mortgage loan application is built for employees, not employers. In 2026, this gap has widened. Lenders are more cautious than ever. They see your fluctuating revenue as a risk rather than a success story. You need a strategy that translates your business success into lender-friendly data.

The economic climate in June 2026 adds another layer of complexity. With the Bank of Canada policy rate at 2.25% and unemployment at 6.8%, lenders have shifted their focus. They no longer care about your peak revenue. They want to see resilience. Your business structure dictates your path. Sole proprietors often find their personal and business finances lumped together. Incorporated owners face a different challenge. You must prove that the money left in the company is accessible for your mortgage payments. A self-employed mortgage Canada requires more than just a good credit score; it requires a narrative of stability.

The Conflict Between Tax Savings and Borrowing Power

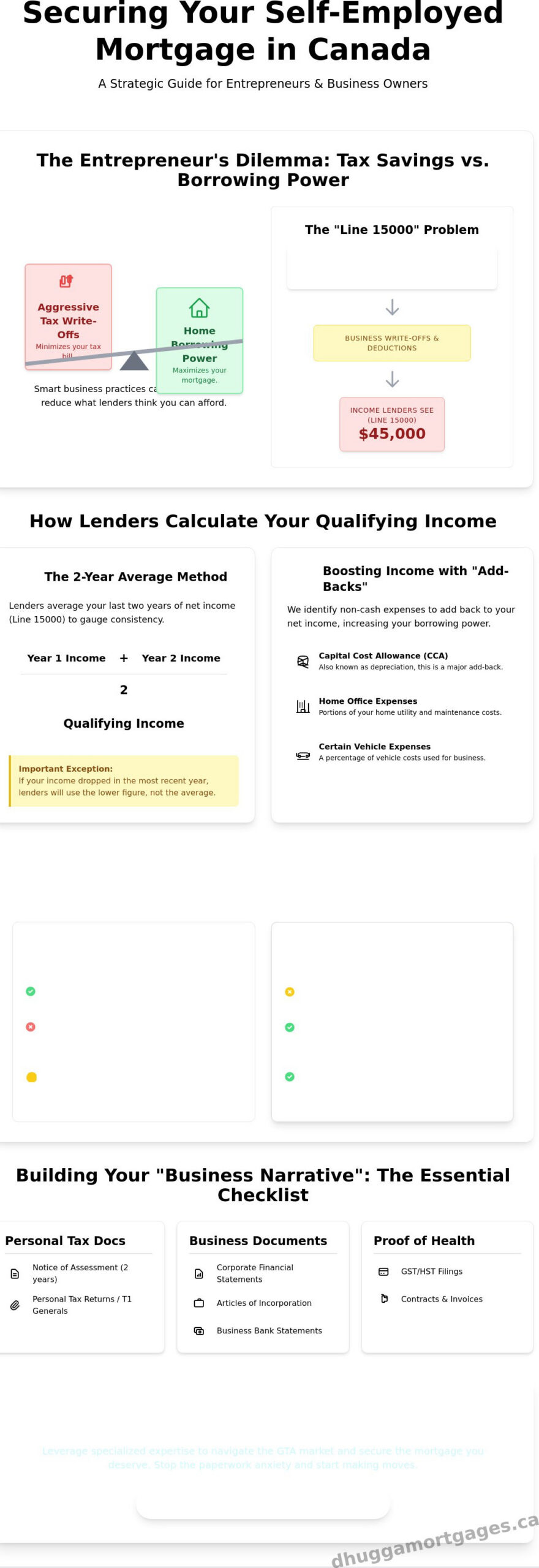

You work hard to minimize your tax bill. Aggressive write-offs are a sign of a smart business owner. However, these deductions lower your reported income on Line 15000 of your Notice of Assessment. This creates the “Line 15000 problem.” Lenders use this number to calculate your debt-to-income ratio. If your NOA shows $45,000 but your business actually earned $160,000, your borrowing power is slashed. Balancing fiscal responsibility with your homeownership goals in the GTA requires a proactive approach. You shouldn’t have to choose between a lower tax bill and a new home.

The 2026 Regulatory Landscape for Entrepreneurs

Regulations from the Office of the Superintendent of Financial Institutions (OSFI) have evolved. Since January 2026, rules for investment properties have tightened, requiring each property to qualify on its own cash flow. This shift has influenced how lenders view all non-traditional borrowers. The stress test remains a high hurdle. Lenders now demand a two-year track record of consistent earnings. They prioritize businesses that show steady growth over those with one-off spikes in revenue. To secure a self-employed mortgage Canada, you must demonstrate that your business can withstand market shifts. We focus on showing lenders the strength of your business, not just your tax returns.

- Sole Proprietors: Lenders look at net professional income plus certain add-backs like depreciation.

- Incorporated Owners: Lenders look at salary, dividends, and sometimes the corporate retained earnings.

- The 2-Year Rule: Most lenders require at least 24 months of self-employed history to consider the income.

How Canadian Lenders Calculate Your Qualifying Income

Lenders don’t just look at your gross revenue. They look at your net income after expenses. This creates a hurdle for entrepreneurs who prioritize tax efficiency. To qualify for a mortgage, you need to show consistency and reliability. If you’re seeking a self-employed mortgage Canada, you must understand the specific math formulas underwriters use to judge your file. They want to see that your business is a stable source of funds, not a temporary spike in cash flow.

The 2-Year Average Method Explained

Lenders typically take your net income from the last two years and average them to find a qualifying number. It’s a straightforward calculation. Take your net income from your two most recent Notices of Assessment, add them together, and divide by two. The Two-Year Average is the gold standard for income verification. However, there’s a critical exception. If your income dropped significantly in the most recent year, lenders won’t use an average. They’ll likely use the lower, more recent figure. This protects the lender from businesses that might be in a downward trend.

Utilizing Business “Add-Backs” to Boost Affordability

Smart tax planning often hurts mortgage applications. We solve this by identifying “add-backs.” These are expenses that reduced your taxable income but didn’t actually cost you cash that year. Capital Cost Allowance (CCA), or depreciation, is the most common example. Lenders often allow us to add this amount back to your net income. We also look at home office deductions and certain vehicle expenses. If you’re incorporated, we can sometimes leverage your corporate retained earnings. This is the profit your business kept rather than paying out as a salary or dividend. It’s a powerful way to show you have the funds to cover your payments.

Some lenders offer a 15% top-up for self-employed borrowers. They take the income on Line 15000 of your tax return and automatically add 15% to account for standard business deductions. This is a fast way to increase your borrowing power without needing complex audits. For realtors and sales professionals, we focus on Gross Commission Income (GCI). We can often use a higher percentage of your total commissions before you paid for marketing or office fees. If your tax returns don’t reflect your true earning power, reach out to our team to explore alternative income verification paths that fit your specific business structure.

You have two primary paths to approval: Stated Income and Proven Income. Proven income relies strictly on your tax documents and NOAs. It gets you the lowest rates but requires a higher reported income. Stated income is different. It’s based on your bank statements and the “reasonableness” of your earnings for your industry. While these programs often require a larger down payment, they provide the flexibility many business owners need in a complex market. Working with the best mortgage broker for self-employed professionals ensures you’re matched with the right program for your specific income structure.

Comparing Your Financing Paths: Traditional Banks vs. Alternative Lenders

One “no” from a big bank doesn’t end your homeownership journey. You have choices. Securing a self-employed mortgage Canada involves picking the right lender category for your specific financial profile. Not everyone fits the same mold. We categorize lenders into three main buckets: A-lenders, B-lenders, and private options. Each has a specific purpose in your long-term strategy. Your goal is to find the lowest cost of borrowing that accepts your current income structure.

A-lenders are the big banks you see on every corner in Toronto or Mississauga. They offer the most competitive rates, like the current 4.04% five-year fixed options. But they want perfection. They demand clear, consistent income and high credit scores. If your business is young or your write-offs are high, they might decline you. B-lenders, or trust companies, offer a middle ground. They accept higher debt ratios and are more flexible with how they verify your earnings. Private lenders are different. They focus almost entirely on your property’s equity. They provide short-term bridges when you need to move fast or fix your credit before moving to a traditional lender.

The A-Lender “Box” for Entrepreneurs

Qualifying at a Tier-1 bank requires a flawless application. You need a credit score of at least 680. You also need standard proof of employment for self-employed status, typically two years of clean Notices of Assessment. If you have less than a 20% down payment, you must qualify for mortgage default insurance from providers like CMHC or Sagen. Keep in mind that CMHC insurance is not available for homes costing $1,000,000 or more. This is a major hurdle in the GTA market where average prices often exceed this limit.

The B-Lender Advantage for Stated Income

B-lenders look at the “reasonability” of your income. They ask a simple question: Does it make sense that a consultant in Brampton earns this much? They use six to twelve months of bank statements to verify cash flow instead of just tax returns. You’ll pay a slightly higher rate and a one-time lender fee, usually 1% of the loan amount. It’s a strategic investment. This path lets you buy the home you want now while your business grows. Most of our clients use a B-lender for two to three years. Once their tax returns show higher income, we move them back to an A-lender for a lower rate. It’s a proactive transition that saves you money over the life of your mortgage.

Choosing your path is a strategic decision. If you have a 20% down payment and a clean credit history, a B-lender provides the “stated income” flexibility you need to bypass the T4 bias. If you’re a first-time buyer with 5% down, you must fit the A-lender box. We analyze your file to see where you land. Don’t guess. Get a professional opinion on which lender will value your business correctly. A self-employed mortgage Canada requires this level of precision. We focus on your current needs while planning for your future refinancing.

The Ultimate Self-Employed Mortgage Documentation Checklist

Success in a self-employed mortgage Canada application depends on your organization. You aren’t just a number. You’re a business owner. Lenders need a clear, unobstructed view of your financial health. Start building your digital folder now. Don’t wait for the perfect house to appear. Having your documents ready allows us to move with the speed the GTA market demands. It turns a complex process into a streamlined approval.

Your baseline requirements include your personal tax documents. Gather your Notices of Assessment (NOAs) and T1 Generals for the last two years. Most importantly, provide proof that your taxes are paid in full. No lender wants to be second in line behind the CRA. You also need your business essentials. This includes your Articles of Incorporation or your Business License. Don’t forget your GST/HST returns for the last four quarters. These documents verify your active status and recent cash flow.

To truly stand out, you need a “Proof of Stability” folder. This is where you separate yourself from the average applicant. Include your year-to-date (YTD) profit and loss statements. Add copies of active contracts, major invoices, and even client testimonials. These documents prove your revenue isn’t a fluke. They show your business has legs. Underwriters value this transparency. It gives them the confidence to approve your file when the tax returns alone don’t tell the whole story.

Preparing Your “Paper Trail” Six Months in Advance

Start your preparation early. You must clear any outstanding CRA tax arrears before you even think about applying. Lenders won’t touch a file if the government is owed money. Organize your bank statements to show consistent business revenue. Avoid large, unexplained cash deposits that could trigger red flags. For a deeper dive into the timing, check out the 2026 Ontario Roadmap for self-employed mortgages. Clean records lead to faster approvals and better rates.

Crafting Your Business Narrative

An underwriter’s job is to find reasons to say “no.” Your job is to give them reasons to say “yes.” A well-written business description bridges the gap. Explain that one-time equipment purchase that lowered your profit last year. Detail why your revenue dipped during a planned transition. Your business license is the cornerstone of your application because it validates your professional history and legal standing in Ontario. If you have questions about your specific documents, contact our expert brokers to review your folder before you submit. We’ll ensure your narrative is bulletproof.

Securing Your GTA Home: Why a Specialized Broker is Your Strategic Edge

Don’t let one bank’s rigid policy stop your momentum. When you walk into a traditional branch, you’re limited to their specific “box.” If you don’t fit, you’re out. We change the game. A specialized broker provides access to over 50 lenders across the country. This includes major banks, credit unions, and trust companies. Securing a self-employed mortgage Canada requires this level of variety. We don’t just find a lender; we find the lender that values your specific business structure.

Local expertise is your biggest advantage in the GTA. Property values in Brampton, Mississauga, and Toronto move fast. Appraisals can be a major hurdle for entrepreneurs. We know which lenders are comfortable with high-density Toronto condos versus detached homes in Brampton. We handle the heavy lifting. You focus on growing your revenue. We manage the documentation, the lender negotiations, and the fine print. It’s a streamlined process designed for busy professionals who value their time.

- Diverse Lender Access: We compare 50+ options to find your perfect match.

- GTA Market Knowledge: We navigate the specific appraisal challenges of Southern Ontario.

- Paperwork Management: Our team handles the documentation grind so you don’t have to.

- Tailored Solutions: We align your corporate structure with the right lending policy.

Why One “No” From a Bank Isn’t the End

A rejection isn’t a dead end. It’s often just a sign that you’re at the wrong bank. We specialize in repositioning applications that were previously declined. We know which lenders are “open for business” in the GTA this month. Their appetites for risk change constantly. Sometimes, the best path forward involves private mortgage options in Ontario. These short-term solutions act as a bridge. They allow you to secure the property now while we work on your long-term bank eligibility. We turn “no” into a strategic “not yet” by providing a clear path to “yes.”

Your Next Steps to Homeownership

Start with a pre-approval that carries weight. For a self-employed buyer, a generic online certificate isn’t enough. You need a deep-dive review of your corporate financials. We look at your retained earnings, your add-backs, and your business narrative before you ever make an offer. This prevents surprises during the closing period. It gives you the confidence to bid in a competitive market. You’ve worked hard to build your business. Now, let your business work for you. Book your self-employed mortgage strategy session with Dhugga Mortgages today. Let’s build your path to a self-employed mortgage Canada and get you into your new home faster.

Take Control of Your Homeownership Strategy

You’ve built a business that thrives. Now it’s time to ensure your financing reflects that success. We’ve explored how to navigate the 2026 market by leveraging add-backs and choosing the right lender path. Whether you fit the A-lender box or need the flexibility of a B-lender, a strategic approach is essential. A self-employed mortgage Canada doesn’t have to be a source of stress. It’s a tool for your personal growth and long-term stability.

Dhugga Mortgages provides the edge you need. We offer specialized expertise in GTA business-owner financing and a proven track record with complex corporate structures. Our team provides access to over 50 institutional and private lenders to find your perfect match. Don’t let paperwork or income fluctuations hold you back. We’re ready to act immediately to secure your future and simplify the process. Your professional success deserves a home that matches your ambition.

Get Started on Your Self-Employed Mortgage Approval Now. Your next move starts with a single conversation. Let’s turn your professional hard work into your new front door. We’re here to lead the way.

Frequently Asked Questions

Can I get a mortgage if I have been self-employed for less than two years?

Yes, you can qualify with less than two years of history, though your options change. Most traditional banks require a 24-month track record. However, CMHC provides flexibility for those with a strong history in the same industry. Alternative lenders often accept 12 to 18 months of business operations if your revenue is stable. Expect to provide more robust documentation of your previous career success to prove your earning potential.

Do I need a larger down payment as a self-employed borrower in Canada?

Not necessarily. If you use “Proven Income” with full tax documentation, you can access the standard 5% down payment for homes under $500,000. For homes above that price, it’s 5% on the first $500,000 and 10% on the remainder. If you choose a “Stated Income” path or a B-lender, expect a minimum requirement of 10% to 20%. This larger equity stake offsets the lender’s risk when traditional income proof is unavailable.

What is a “Stated Income” mortgage and does it still exist in 2026?

Stated income mortgages are very much alive in 2026 through alternative and private lenders. These programs allow you to declare a reasonable income based on your industry and bank statements. They don’t rely strictly on your tax returns. This is a vital tool for a self-employed mortgage Canada when tax write-offs reduce your borrowing power. These programs usually require a 20% down payment and a clean credit history to qualify.

How does being incorporated affect my mortgage application differently than a sole proprietorship?

Incorporated business owners have more flexibility in how they prove their income. You can use a combination of salary, dividends, and sometimes the retained earnings left within the corporation. Sole proprietors are generally limited to the net income shown on their T1 General tax forms. Lenders view corporations as more stable entities, which can lead to higher borrowing limits if your corporate financials are strong and consistent over two years.

Can I use my business bank statements to prove my income?

Yes, your business bank statements are a primary tool for alternative lenders. They typically review 6 to 12 months of deposits to verify your actual cash flow. This is the core of the “stated income” approach mentioned earlier. While big banks might ignore these statements in favour of tax returns, specialized lenders use them to confirm your business’s health. Keep your business and personal accounts strictly separate to make this verification process faster.

What credit score do I need for a self-employed mortgage in Ontario?

Aim for a credit score of 680 or higher to access the best rates at traditional banks. Securing a self-employed mortgage Canada in Ontario requires a solid credit profile to offset the perceived risk of fluctuating income. If your score is between 600 and 670, you’ll likely work with B-lenders who specialize in non-traditional files. For scores below 600, private lenders become the primary option. In these cases, the equity in your home matters more than the score.

Are mortgage rates higher for self-employed individuals?

You won’t pay higher rates if you qualify at a traditional bank with full income verification. You’ll access the same competitive market rates as a T4 employee. However, if you require the flexibility of a B-lender or a stated income program, expect rates to be slightly higher. These lenders also charge a one-time fee, usually 1% of the mortgage amount. It’s a strategic trade-off for easier qualification and significantly higher borrowing power.