Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

New to Canada Mortgage Program: Your 2026 Guide to Homeownership

- Home

- New to Canada Mortgage Program: Your 2026 Guide to Homeownership

What if the big bank that rejected your mortgage application didn’t actually have the final word? Most newcomers feel trapped in a cycle of high GTA rents simply because they lack a Canadian credit history. It is frustrating to realize your international success does not always translate at the local branch. The new to Canada mortgage program changes this narrative by recognizing your global stability. You do not have to wait years to build a local score from scratch to find your place in the market.

We agree that your path to a home should not be blocked by residency status or a thin credit file. This guide shows you exactly how to secure a mortgage with 5% to 10% down even while on a work permit. You will learn which documents are mandatory for a 2026 application, how to access competitive interest rates currently near 3.94%, and how to use new government rebates to your advantage. It is time to stop paying your landlord’s mortgage and start building your own equity. Let’s get you moving.

Key Takeaways

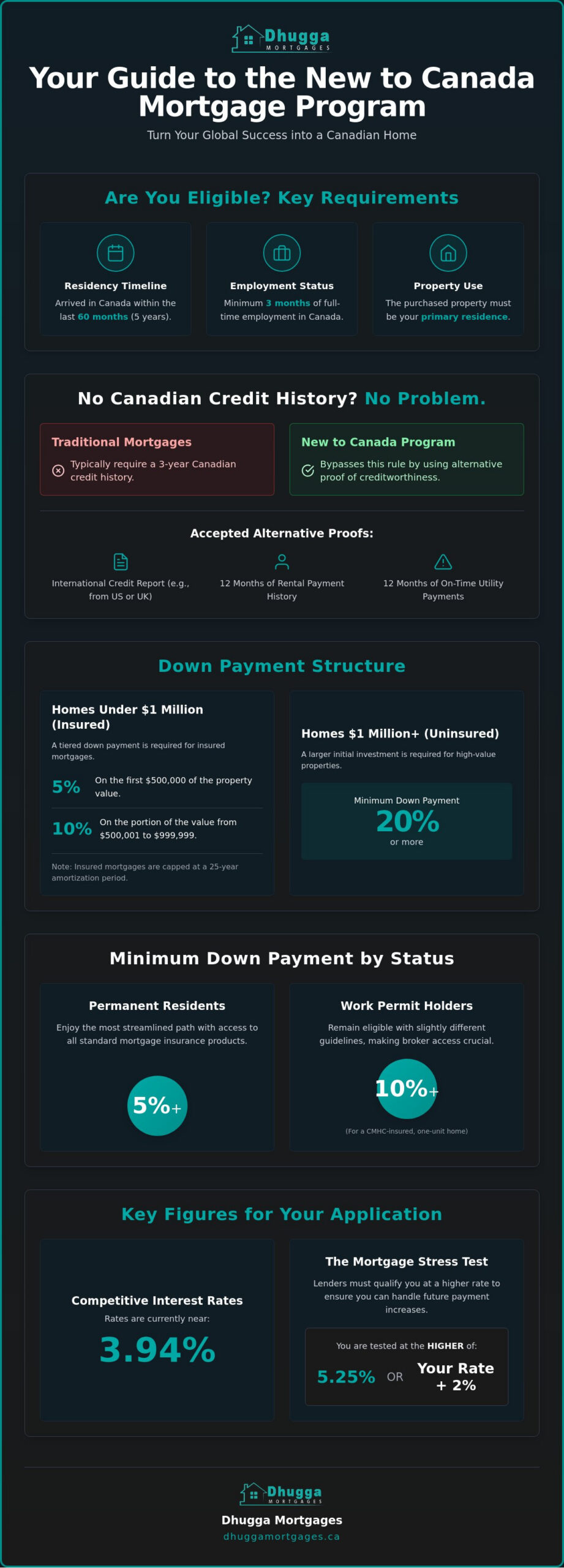

- Bypass standard three-year Canadian credit history requirements if you have been in the country for less than 60 months.

- Learn how to structure your down payment with as little as 5% down on the first $500,000 of your home’s value.

- Identify the specific documents required for the new to Canada mortgage program to ensure a fast and successful approval.

- Discover how a specialized broker provides access to over 50 lenders, including those with flexible policies for work permit holders.

What is the New to Canada Mortgage Program?

The new to Canada mortgage program is a specialized lending framework. It’s built specifically for residents who have lived in the country for less than five years. Most traditional mortgage products require a three-year Canadian credit history. This program throws that requirement out the window. It allows you to bypass local credit gaps by using alternative data. Your international stability finally counts for something here.

These mortgages are typically backed by default insurance. Providers like the Canada Mortgage and Housing Corporation (CMHC), Sagen, and Canada Guaranty provide the safety net lenders need. This backing allows you to secure a home with as little as a 5% down payment. It’s a high-impact solution for families ready to stop renting and start building equity. It’s fast. It’s accessible. It’s designed for your success.

Why This Program Exists for Newcomers

Canada relies on the economic contributions of skilled immigrants. You bring talent and professional expertise to high-growth areas like the GTA. This program acknowledges that value immediately. It solves the frustrating credit “Catch-22.” You often need a local credit score to buy a home, but building that score takes years of living here. By recognizing foreign credit or alternative payment proofs, this initiative accelerates your path to homeownership. It’s about turning newcomers into permanent neighbours in Brampton, Mississauga, and beyond. We make the transition from tenant to owner seamless.

The Difference Between Insured and Uninsured Newcomer Loans

Understanding your loan type is essential for your 2026 strategy. Insured mortgages are for homes valued under $1 million. They allow for the lowest down payments. You’ll pay an insurance premium, but you gain entry to the market with less capital. These loans are capped at a 25-year amortization period. Uninsured loans require a down payment of 20% or more. These are mandatory for properties over the $1 million mark. They offer more flexibility on property types and longer amortizations but demand a larger initial investment.

Your qualification also depends on the current mortgage stress test. As of July 16, 2026, lenders test your finances at the higher of 5.25% or your contract rate plus 2%. This ensures you can handle your payments even if rates shift. We compare multiple newcomer programs at once to find the one that fits your specific financial profile. Don’t let bank rejection stop you. There’s a path forward. We find it together. Move fast. Get approved. Start your Canadian dream today.

Eligibility Requirements for Newcomers in 2026

Qualification for the new to Canada mortgage program starts with your arrival date. You must have immigrated or relocated to Canada within the last 60 months. This five-year window is your opportunity to leverage specialized lending rules before you are classified as a domestic borrower. Lenders also require a minimum of three months of full-time employment within Canada. If you were transferred by your current employer from an international office, you may be exempt from this three-month waiting period. This allows you to start your home search almost immediately after landing.

Your intent matters as much as your status. The property you buy must be your primary residence. This program is designed to help families settle into the community, so investment properties or rentals do not qualify for these specific low-down-payment terms. Whether you are looking in Brampton, Mississauga, or Caledon, the home must be owner-occupied. This focus on stability is why lenders are willing to offer competitive rates even without a lengthy Canadian history.

Permanent Residents vs. Work Permit Holders

Permanent Residents (PR) generally enjoy the most streamlined path. You have access to all standard mortgage insurance products with down payments starting at just 5%. Work permit holders have a slightly different path but remain eligible. Under current 2026 guidelines, non-permanent residents can secure CMHC-insured financing with a 10% down payment for a one-unit home. Some lenders have stricter internal policies for work permits, which is why comparing multiple options is vital. We help you identify which lenders prioritize your specific residency status to avoid unnecessary rejections.

Establishing Creditworthiness Without a Canadian Score

A lack of a local credit score is not a dealbreaker. We bridge this gap using alternative proof of financial responsibility. If you moved from a country with a compatible credit system, such as the US or the UK, we can often pull an international credit report to satisfy lender requirements. For those without an international report, we look at your local payment history over the last 12 months. This includes:

- Rental History: Confirmed timely payments to a landlord for at least one year.

- Utility Payments: Documented proof of on-time payments for hydro, water, or heating.

- Service Plans: Consistent payments for mobile phone plans or internet services.

- Insurance: Regular premiums paid for auto or life insurance policies.

Providing this documentation proves you are a reliable borrower. If you are unsure if your documents meet the 2026 criteria, speak with our team to review your eligibility today. We specialize in organizing these alternative credit packages to ensure your application is move-in ready.

Down Payment and Property Value Limits in Ontario

The new to Canada mortgage program requires a strategic approach to your savings. In 2026, the minimum down payment follows a tiered structure. You need 5% on the first $500,000 of the purchase price. For any amount above that, a 10% down payment is mandatory. For example, on a $700,000 home, you would need $25,000 for the first portion and $20,000 for the remaining $200,000. That is a total of $45,000. This tiered system keeps entry-level homes accessible for newcomers while ensuring financial stability as prices climb.

Keep the $1,000,000 cap in mind. For insured newcomer mortgages, the property value must stay below this million-dollar threshold. If the purchase price exceeds $1,000,000, you will likely need a full 20% down payment. This makes the math critical when browsing listings in the GTA. Your down payment funds must come from your own resources, such as savings or an RRSP, or be provided as a non-repayable gift from an immediate family member. Lenders require a 90-day history of these funds to prevent fraud and confirm your financial readiness.

The Reality of the GTA Housing Market

Brampton and Mississauga often push the $1,000,000 limit. Finding a detached home under this cap is becoming harder, but townhomes and condos remain excellent entry points for the new to Canada mortgage program. Caledon offers more space but sometimes higher price points that may trigger the 20% down payment rule. If you are looking for ways to bridge the gap, our First-Time Home Buyer Mortgage Ontario guide provides details on specific grants and tax credits. We help you navigate these regional price differences to find a home that fits both your lifestyle and your budget.

Closing Costs: The Hidden 1.5% to 4%

Closing costs are the hidden hurdle that many newcomers overlook. You must budget an additional 1.5% to 4% of the purchase price in liquid cash. This covers legal fees, home inspections, and Land Transfer Taxes. If you buy within the City of Toronto, be prepared to pay both provincial and municipal land transfer taxes. Outside of Toronto, in areas like Peel Region, you only pay the provincial portion. Lenders often require proof of “working capital” before final approval. This is usually 1.5% of the home price held in a Canadian bank account. It proves you can handle the transaction costs without exhausting your entire savings. We calculate these totals for you early in the process so you can bid with confidence.

Step-by-Step: How to Secure Your Newcomer Mortgage

Securing a home in the GTA requires speed and precision. You don’t have time for bank delays or vague answers. The new to Canada mortgage program works best when you follow a proven, high-velocity sequence. We take charge of the process to ensure your transition from landing to homeownership is seamless. Follow these five steps to get your keys faster.

- Step 1: Consult a Specialized Broker. Don’t start at a local branch. We assess your eligibility across 50+ lenders to find the one with the most flexible newcomer policies.

- Step 2: Build Your Document Package. Collect your PR card, employment letter, and bank statements immediately. Having these ready prevents last-minute stress.

- Step 3: Get Pre-Approved. Lock in your rate. As of July 2026, the lowest 5-year fixed insured rates are near 3.94%. Knowing your budget stops you from falling in love with a home you can’t afford.

- Step 4: Target the Right Neighbourhoods. Shop with confidence in Brampton, Mississauga, or Caledon. Your pre-approval makes your offer stand out to sellers.

- Step 5: Finalize and Close. Once your offer is accepted, we move rapidly to finalize the underwriting. We handle the heavy lifting with the lender.

Essential Document Checklist for 2026

Lenders in 2026 are focused on stability. You must prove your income with recent pay stubs and T4s if you’ve been here long enough to receive them. For your down payment, provide 90 days of bank statement history. This proves the funds are yours and not a high-interest loan. If your Canadian credit is still growing, a letter of reference from a recognized financial institution in your home country is a powerful tool. It bridges the gap and builds trust with Canadian underwriters. Accuracy is non-negotiable here.

Avoiding Common Newcomer Application Mistakes

Don’t jeopardize your approval in the final weeks. Avoid making large purchases on credit, such as a new car or expensive furniture, before your mortgage closes. These new debts change your debt-to-income ratio and can trigger an immediate rejection. Also, ensure you have completed your employment probation period. Most lenders require you to be “permanent” staff before they release funds. For more strategic advice on timing your purchase, review our new to Canada mortgage program guide. Ready to start? Get your custom mortgage plan today and secure your spot in the Canadian market.

Why Dhugga Mortgages is Your Best Partner in the GTA

We don’t just process applications. We advocate for your future in Canada. The new to Canada mortgage program is complex, but our team makes it simple. We understand the specific hurdles of the Brampton and Mississauga markets. We know which lenders value your international experience and which ones will reject you for a thin credit file. Our local expertise ensures you aren’t just another number in a bank queue. You are a future homeowner. We treat you that way.

Speed is our priority. You need answers now, not in three weeks. Our efficiency-first approach means we spot potential issues before they become rejections. We have direct experience with complex cases. This includes self-employed newcomers and those navigating the market on work permits. We take charge of the process. We deliver results. You get peace of mind.

- Local Expertise: Deep roots in Brampton, Mississauga, and Caledon.

- Lender Access: Direct connections to over 50 “A” and alternative lenders.

- Specialized Support: Expert handling of PR and work permit applications.

- Proven Track Record: A history of successful approvals for GTA families.

Beyond the Big Banks

Big banks have rigid boxes. If you don’t fit their standard criteria, they say no. We look beyond those limits. By comparing over 50 lenders, we often find more competitive rates and flexible terms that the big banks won’t disclose. We specialize in finding products for those who don’t fit the typical borrower profile. If traditional routes are blocked, we explore alternative paths through Private Mortgage Lenders Ontario. This ensures every newcomer has a viable path to homeownership. We find the edge you need to win in 2026.

Start Your Canadian Journey Today

We invite you to book a professional consultation at our Brampton or Toronto offices to secure your financial future. Our team has helped thousands of families settle in Ontario with confidence and speed. We know the neighbourhoods. We know the rules. We know how to get you approved. Don’t leave your first home to chance. Use our online pre-approval tool to see what you qualify for today. Let’s get you moving.

Claim Your Place in the Canadian Market

Your future in Ontario starts with a solid foundation. Homeownership is no longer a distant goal for newcomers. By leveraging the new to Canada mortgage program, you can bypass traditional credit hurdles and secure a home with as little as 5% down. Whether you hold a work permit or permanent residency, the path to building equity in the GTA is clear and accessible. You have the talent and the vision; now you just need the right financial strategy.

We offer the localized expertise you need in Brampton and Mississauga. Our team provides expert guidance for PR and work permit holders to ensure every application is move-in ready. With access to over 50 Canadian lenders, we find the competitive rates and flexible terms that big banks often overlook. We handle the complexity so you can focus on your move. Speed, accuracy, and reliability are our core standards.

Don’t let another year of high rent pass you by. Take the proactive step toward your Canadian dream today. Secure your New to Canada mortgage pre-approval today with Dhugga Mortgages. We are ready to help you settle into your new home with confidence.

Frequently Asked Questions

How long do I have to be in Canada before I can apply for a mortgage?

You can apply for a mortgage after completing just three months of full-time employment in Canada. This is the minimum requirement for most lenders to verify income stability. If you were transferred to a Canadian branch by your current international employer, you might even qualify to apply immediately upon arrival without the three-month wait.

Can I get a mortgage with a work permit in 2026?

Yes, work permit holders are fully eligible to buy a home with as little as a 10% down payment. You must have a valid permit and a stable job offer or history in Canada. While some big banks are restrictive, the new to Canada mortgage program includes several lenders that specifically cater to non-permanent residents seeking a primary residence.

Is a 35% down payment always required for newcomers?

No, the idea that newcomers must provide a 35% down payment is a common misconception. If you have a stable income and can prove your creditworthiness through alternative documents, you can buy with as little as 5% to 10% down. The 35% requirement usually only applies to those who cannot verify their income or provide any international credit history.

What happens if I don’t have a Canadian credit score yet?

Lenders will use alternative credit data to approve your application if your Canadian score is still developing. We help you organize a 12-month history of timely rent payments, utility bills, or mobile phone plan payments to prove your reliability. We can also pull international credit reports from countries like the US or UK to satisfy lender requirements quickly.

Can I use a gift from family back home as my down payment?

Yes, you can use non-repayable gifted funds from immediate family members for your down payment. You need a signed gift letter and proof that the money has been transferred into your Canadian bank account. Most lenders want to see these funds in your account at least 15 days before your closing date to ensure a smooth transaction.

Are interest rates higher for the New to Canada mortgage program?

No, newcomer mortgage rates are generally identical to standard market rates. As of July 2026, the lowest 5-year fixed insured rates are approximately 3.94%. You don’t pay a premium for being new to the country. As long as you meet the program’s eligibility criteria, you have access to the same competitive rates as any other Canadian borrower.

Do I need to be a Permanent Resident to buy a house in Ontario?

You do not need Permanent Resident status to purchase a home. Work permit holders can buy property in Ontario as long as it is for their primary residence and not an investment. It’s important to consult with us early to understand how your specific residency status affects your down payment requirements and any potential tax implications in the GTA.

What is the maximum home price for a newcomer mortgage?

The maximum purchase price for an insured newcomer mortgage is $999,999. If the home costs $1,000,000 or more, it is classified as an uninsured mortgage and requires a minimum 20% down payment. This limit is a vital consideration for buyers in Brampton and Mississauga where property values often approach or exceed the million-dollar mark.