Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Reverse Mortgage Canada: The Ultimate 2026 Guide for Ontario Homeowners

- Home

- Reverse Mortgage Canada: The Ultimate 2026 Guide for Ontario Homeowners

What if the smartest way to fund your retirement in Ontario isn’t by selling your home, but by staying exactly where you are? Many homeowners feel trapped by rising living costs and the fear of being forced to downsize away from the neighbours they love. You’ve worked hard to build equity. You shouldn’t have to leave your community just to access your wealth. A reverse mortgage Canada strategy offers a strategic way to unlock that value without the stress of monthly payments or moving trucks.

We know the anxiety that comes with fluctuating interest rates and the worry about your estate’s future. You deserve clear, expert guidance from a local broker who understands the Ontario market. This guide shows you how to secure tax-free cash for renovations or daily expenses while maintaining full ownership. We’ll explore the 2026 landscape, explain the No Negative Equity Guarantee, and show you exactly how to stay in the home you love indefinitely. It’s time to stop worrying about your bank balance and start enjoying the retirement you earned. Let’s get started.

Key Takeaways

- Access tax-free cash from your home equity without ever making a monthly principal or interest payment.

- Understand how your age and property type determine how much you can borrow with a reverse mortgage Canada.

- Evaluate the long-term benefits of staying in your home versus the hidden costs and emotional impact of downsizing.

- Follow a streamlined application roadmap including mandatory independent legal advice to protect your estate and interests.

- Leverage local Ontario expertise to compare top-tier lenders and secure the most competitive equity-release terms available.

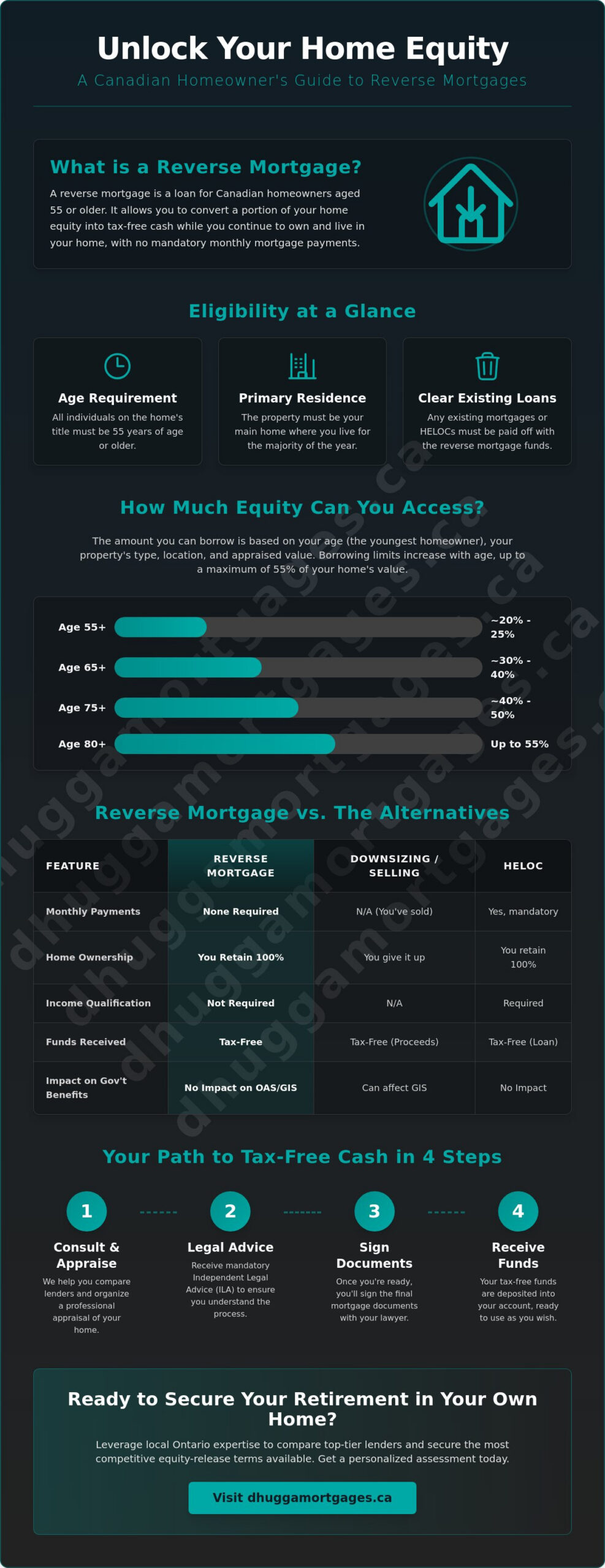

What is a Reverse Mortgage in Canada? (2026 Update)

A reverse mortgage is a powerful financial tool designed specifically for Canadian homeowners aged 55 and older. It’s a non-recourse loan that allows you to convert a portion of your home equity into cash without the burden of monthly principal or interest payments. Unlike a traditional sale, you retain 100% ownership. You stay on the title. You keep control of your property. You decide how to use the funds. Whether it’s covering daily living costs or funding a major home renovation, the money is yours to manage as you see fit.

When exploring What is a Reverse Mortgage?, it’s vital to understand the “equity release” concept. In Canada, these funds are entirely tax-free. They don’t count as taxable income. This means they won’t trigger the clawbacks often seen with RRSP withdrawals or impact your Old Age Security (OAS) benefits. Using a reverse mortgage Canada strategy is a highly efficient way to supplement your retirement income while keeping your primary asset intact.

How Reverse Mortgages Differ from Traditional Mortgages

Traditional mortgages require you to prove high income and maintain a strong credit score to qualify for monthly payments. Reverse mortgages flip this script. Approval is based primarily on your age, your home’s location, and its appraised value. You don’t make monthly payments. Instead, the interest is added to the loan balance over time. A major safety feature is the “non-recourse” guarantee. This ensures you or your heirs will never owe more than the fair market value of the home when it’s sold. It’s built-in protection for your estate. Most borrowers find the lack of income verification a massive relief during retirement.

The 2026 Regulatory Landscape in Ontario

The Canadian market is strictly regulated by the Office of the Superintendent of Financial Institutions (OSFI). These guidelines are more conservative and secure than the US “HECM” model. They ensure lenders maintain high capital buffers and protect seniors from predatory practices. In 2026, the housing markets in Brampton and Mississauga remain remarkably stable. This local strength provides a solid foundation for equity growth, even as you access funds. You get the peace of mind that comes with a regulated, predictable financial product. By choosing a reverse mortgage Canada solution, you’re opting for a transparent process designed to keep you in your home longer.

Eligibility and Mechanics: How Much Can You Borrow?

To qualify for a reverse mortgage Canada plan, every person listed on your home’s title must be at least 55 years old. This is a non-negotiable threshold. If one spouse is younger, they must be removed from the title or you must wait until they reach the age requirement. Additionally, the property must serve as your primary residence. Lenders require you to live in the home for the majority of the year. This ensures the loan remains a residential product rather than an investment or commercial vehicle. You must also pay off any existing traditional mortgages or HELOCs using the proceeds of the reverse mortgage. This leaves you with no monthly mortgage payments.

The maximum amount you can borrow is capped at 55% of your home’s appraised value. However, don’t expect the maximum immediately at age 55. Borrowing limits are scaled based on the age of the youngest homeowner. A 55-year-old might only access 20% to 25% of their equity. An 80-year-old borrower will qualify for significantly higher percentages, often reaching that 55% limit. This conservative approach, as outlined in the Government of Canada’s guide to reverse mortgages, is designed to protect your equity from being eroded too quickly by compounding interest. It ensures that even after years of interest accrual, there’s typically a significant portion of value left for your estate.

Property Appraisal Nuances in the GTA

In high-demand markets like Toronto and Mississauga, appraisal values are the backbone of your loan. In 2026, lenders aren’t just looking at your neighbourhood’s average sale price. They’re looking at the specific condition of your property. Recent renovations in Brampton or Mississauga can drastically increase your accessible cash. However, local market volatility is always factored into lender calculations. Lenders may apply “haircuts” or more conservative valuations in areas experiencing rapid price shifts to ensure the loan remains secure. Keeping your home well-maintained is the best way to maximize your borrowing power.

Calculating Your Potential Payout

You can choose between a single lump-sum payment or a series of planned advances. Planned advances are often more cost-effective for daily living expenses. You only accrue interest on the funds you’ve actually received, not the total amount you’re approved for. Over a 10-to-20-year horizon, this strategy can save your estate tens of thousands of dollars. It’s a strategic way to manage your wealth while staying in control. Before committing to a payout structure, using a reverse mortgage calculator Ontario homeowners rely on can help you estimate exactly how much tax-free cash your property could unlock. If you’re ready to see how these numbers look for your specific property, you can explore your reverse mortgage options with a local expert who understands the Ontario market.

Reverse Mortgage vs. Alternatives: Making the Right Move

Choosing the right path for your equity requires looking at the big picture. Many retirees weigh a reverse mortgage Canada plan against other common equity-release tools. It’s not just about the interest rate. It’s about long-term stability and protecting your cash flow. Unlike selling assets or withdrawing from an RRSP, these loan proceeds are tax-free. They won’t claw back your Old Age Security (OAS) or Guaranteed Income Supplement (GIS). This is a massive strategic advantage for Ontario seniors on a fixed budget who need to maintain their government benefits. Before making a final decision, reviewing the full reverse mortgage pros and cons Canada homeowners are weighing in 2026 can help you determine whether this strategy truly aligns with your retirement goals.

Private second mortgages are another route. They offer speed but carry high interest rates and very short terms. They’re effectively 12-month bridges. They aren’t built for a 20-year retirement. If you need a permanent solution that doesn’t require constant renewals, the reverse mortgage is the more secure choice for your peace of mind. For homeowners who don’t yet qualify for a reverse mortgage or need a short-term bridge, understanding how private mortgage lenders Ontario operate can help you evaluate all available options before committing to a long-term strategy.

The HELOC Trap for Seniors

A Home Equity Line of Credit (HELOC) looks attractive because of lower initial rates. But it’s a “callable” loan. The bank can demand full repayment or freeze your limit at any time. Interest-only payments can spike if prime rates rise, putting your retirement budget at risk. Most retirees in 2026 find income qualification for a HELOC nearly impossible once they’ve stopped working. Banks want to see a steady paycheque from an employer. A reverse mortgage removes this hurdle. It eliminates monthly debt obligations entirely. You get the psychological freedom of knowing no bill is coming on the first of the month. For a deeper dive into these mechanics, the Federal government provides a resource on Understanding Reverse Mortgages.

Downsizing Costs in Ontario You Might Not Expect

Moving seems like an easy fix. The reality is expensive. In Toronto, you’ll pay a double Land Transfer Tax. In Brampton or Mississauga, the provincial tax still eats a huge chunk of your equity. Add in real estate commissions, which often sit at 5%, and legal fees. You could lose 10% of your home’s value before you even unlock a cent. Then there’s the “lifestyle tax.” Leaving your neighbourhood means losing your support network, your favourite shops, and your local doctors. Staying put with a reverse mortgage Canada strategy preserves your social capital. It allows you to age in place without the financial friction of a move. You keep your home. You keep your community. You keep your cash.

The Application Process: From Appraisal to Tax-Free Cash

Accessing your home equity shouldn’t be a mystery. The process for a reverse mortgage Canada plan is structured to be transparent, secure, and surprisingly fast. It begins with a strategic consultation with a specialized mortgage broker. We don’t just look at one lender. We compare options from HomeEquity Bank, Equitable Bank, and Bloom Finance to find the specific fit for your goals. Once we identify the right product, we submit your application. This starts a sequence of protective steps designed to ensure you’re making an informed decision for your future.

After the initial application, the process moves through four critical stages. First, you’ll receive an information package to review. Second, a professional property appraisal is conducted by a lender-approved expert to confirm your home’s current market value. Third, the file goes to underwriting for final approval. Finally, the funds are released. If you have an existing mortgage or HELOC, those are paid off first. The remaining tax-free cash is then deposited directly into your account. It’s a streamlined transition from being “house-rich” to having the liquidity you need. If you’re ready to start, you can apply for a reverse mortgage today to lock in your appraisal.

Why Independent Legal Advice (ILA) is Critical

In Canada, Independent Legal Advice is a mandatory requirement for every reverse mortgage. You’ll meet with a lawyer of your choosing to review the loan contract in detail. This step is vital. It ensures you fully understand your obligations and the “No Negative Equity Guarantee.” The lawyer’s role is to protect you from any external pressure and confirm that you’re entering the agreement voluntarily. In Ontario, you should expect total setup costs of approximately $3,000. This amount typically covers the appraisal, lender fees, and your legal advice. These costs are usually deducted from the loan proceeds, so you don’t need to pay them out of pocket.

Timeline: How Fast Can You Access Funds?

Speed is a priority, but accuracy is essential. In the 2026 GTA market, the average timeline from consultation to funding is three to six weeks. High demand in Toronto and Mississauga can sometimes lead to appraisal backlogs, which is the most common cause of delay. Title issues or unresolved liens can also slow things down. A specialized broker streamlines the document collection process by acting as the central hub between you, the lender, and the appraiser. We handle the friction so you can focus on your retirement plans. By staying proactive and having your property tax statements and insurance papers ready, we can often push toward the faster end of that window.

Why Work with Dhugga Mortgages for Your Reverse Mortgage?

Choosing the right path for your home equity shouldn’t feel like a sales pitch. When you work with Dhugga Mortgages, you gain a proactive advocate who shops the entire market on your behalf. Most banks only offer their own proprietary products. We provide direct access to Canada’s top providers, including HomeEquity Bank, Equitable Bank, and Bloom Finance. This competition works in your favour. We compare terms, interest rates, and unique product features to ensure you get the best possible fit for your specific retirement goals. Jaspreet Dhugga leads with a no-pressure, educational approach. We want you to feel confident. We want you to be informed. We don’t believe in rushing a decision this important.

Our relationship doesn’t end when the loan is funded. We provide ongoing support to help you manage your advances and understand how your equity evolves over time. Whether you need to adjust your payout schedule or have questions about your annual statement, we’re just a phone call away. This level of service is why Ontario homeowners trust us to handle their reverse mortgage Canada strategy. We’re your long-term partners in retirement stability. We handle the complexity so you can focus on enjoying your home.

Local GTA Market Knowledge

Understanding the micro-trends in Caledon, Brampton, or the Toronto core is essential for a successful application. A generic appraisal can often undervalue the unique features of your specific neighbourhood. We use our deep local insights to help maximize your appraisal value from the start. We know which renovations add the actual equity lenders look for in the current Ontario market. Our commitment to the local senior community means we treat every client like a neighbour. We understand the value of your street because we live and work in these communities too. This local edge ensures you get the most out of your property.

Strategic Estate Planning

A reverse mortgage Canada solution is often a family decision. We frequently facilitate meetings with your children or financial planners to ensure everyone is aligned. Our goal is to structure the loan to preserve as much inheritance as possible while meeting your immediate cash flow needs. We look at the long-term impact on your estate and provide the clear data your family needs to feel secure. Transparency is our priority. If you’re ready to explore how this fits into your overall plan, Book a free, confidential consultation with Dhugga Mortgages. We’ll give you the clarity you need to move forward with total peace of mind.

Take Control of Your Home Equity Today

Your home is likely your most valuable asset. In the 2026 Ontario market, it’s time to make that asset work for you. We’ve explored how a reverse mortgage Canada plan provides tax-free liquidity without the stress of monthly payments or the upheaval of moving. You keep your title. You keep your community. You keep your peace of mind. By working with a local expert, you ensure your appraisal reflects the true value of your GTA property while accessing the most competitive terms from top-tier lenders.

Dhugga Mortgages is here to streamline the entire process. We offer specialized senior financing and deep roots in the Brampton and Mississauga real estate markets. We don’t just find a loan; we build a strategy that protects your estate and your future. Don’t wait for rising costs to dictate your retirement. Secure your retirement today with a free reverse mortgage assessment. Your home has taken care of you for years. Now, let it provide the retirement you deserve.

Frequently Asked Questions

Can the bank take my home if the balance exceeds the value?

No. Every reverse mortgage Canada product includes a No Negative Equity Guarantee. You or your estate will never owe more than the fair market value of the home when it’s sold. Even if the housing market dips or the loan balance grows, the bank cannot come after your other assets or your heirs. This protection is a core regulatory requirement that ensures your estate is never left with debt.

Do I have to pay taxes on the money I receive from a reverse mortgage?

No. The funds you receive are considered a loan and are not taxable as income. You can use the cash for living expenses, renovations, or debt consolidation without increasing your tax bill. This makes it a highly efficient tool compared to withdrawing funds from a taxable RRSP or RRIF. You get the full value of your equity without the Canada Revenue Agency taking a cut.

Will a reverse mortgage affect my Old Age Security (OAS) or GIS payments?

No. Since the proceeds are not considered income, they don’t trigger clawbacks for OAS or the Guaranteed Income Supplement (GIS). You can access your home equity while maintaining your full government benefits. It’s a strategic way to increase your monthly cash flow without losing the support you’ve earned. Your benefits remain secure while your liquidity increases.

Can I still leave my home to my children in my will?

Yes. You retain 100% ownership and title of the property throughout the life of the loan. When you pass away, your heirs have the option to pay off the loan balance and keep the home or sell it. They’ll receive the remaining equity after the loan is settled. Most Ontario estates still have significant equity left for beneficiaries due to long-term property appreciation.

What happens if one spouse passes away or moves into long-term care?

Nothing changes as long as one spouse remains in the home as their primary residence. The loan doesn’t become due until the last registered owner either passes away or moves out permanently. This provides essential stability for the surviving spouse. They can continue to live in the home without worrying about repayment or being forced to move away from their community.

Are reverse mortgage interest rates higher than regular mortgages?

Yes. Rates for a reverse mortgage Canada are typically 1.5% to 2.5% higher than conventional mortgage rates. This reflects the fact that you aren’t making monthly payments and the lender is taking on more risk. However, you’re paying for the flexibility of eliminated monthly obligations and guaranteed occupancy. We help you compare rates from lenders like HomeEquity Bank and Equitable Bank to find the most competitive option. To get a clearer picture of how these rates affect your total borrowing costs over time, try our reverse mortgage calculator Ontario residents use to model their 2026 equity access scenarios.

Can I pay off the reverse mortgage early if I decide to sell?

Yes. You can pay off the balance at any time, usually when you sell the home or move. Most lenders allow for early repayment, though prepayment charges may apply if you settle the loan within the first few years. These charges typically decrease the longer you hold the loan. We’ll review the specific schedule in your contract to ensure you understand any potential costs before you sign.

Is a reverse mortgage available for condos in Toronto and Mississauga?

Yes. Condos are eligible as long as they’re your primary residence and meet the lender’s minimum appraised value. In 2026, many GTA condos qualify easily due to strong property values. Some lenders may have specific requirements regarding the condo corporation’s reserve fund or the building’s maintenance status. We’ll verify your specific building’s eligibility during our initial consultation to ensure a smooth approval process.