Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Using a HELOC for Renovations in Ontario: The 2026 Homeowner’s Guide

- Home

- Using a HELOC for Renovations in Ontario: The 2026 Homeowner’s Guide

Why pay land transfer taxes and moving fees when you can “buy” a brand new home exactly where you already live? With Toronto house prices averaging $1.12 million, upgrading your current space is the strategic play for 2026. You likely feel the pressure of $160 per hour labour costs and shifting interest rates. It’s a lot to manage. using HELOC for renovations Ontario gives you the edge you need. It offers lower rates than personal loans and the flexibility to pay contractors in stages.

You want a streamlined way to boost your property value without the complexity of a total refinance. We agree that navigating the 65% LTV regulations and the stress test can feel daunting. This guide simplifies the process. You’ll learn how to leverage your equity efficiently while capitalizing on the new 2026 HST rebates. We are breaking down the current 4.95% rate landscape and the best ways to fund your project. Let’s get your renovation started on solid financial ground.

Key Takeaways

- Access a revolving line of credit to fund your project in stages. This flexibility ensures you only pay interest on the funds you actually use for your renovation.

- Save on massive Land Transfer Taxes and moving fees by upgrading your current space. using HELOC for renovations Ontario is a cost-effective alternative to buying in a high-priced market.

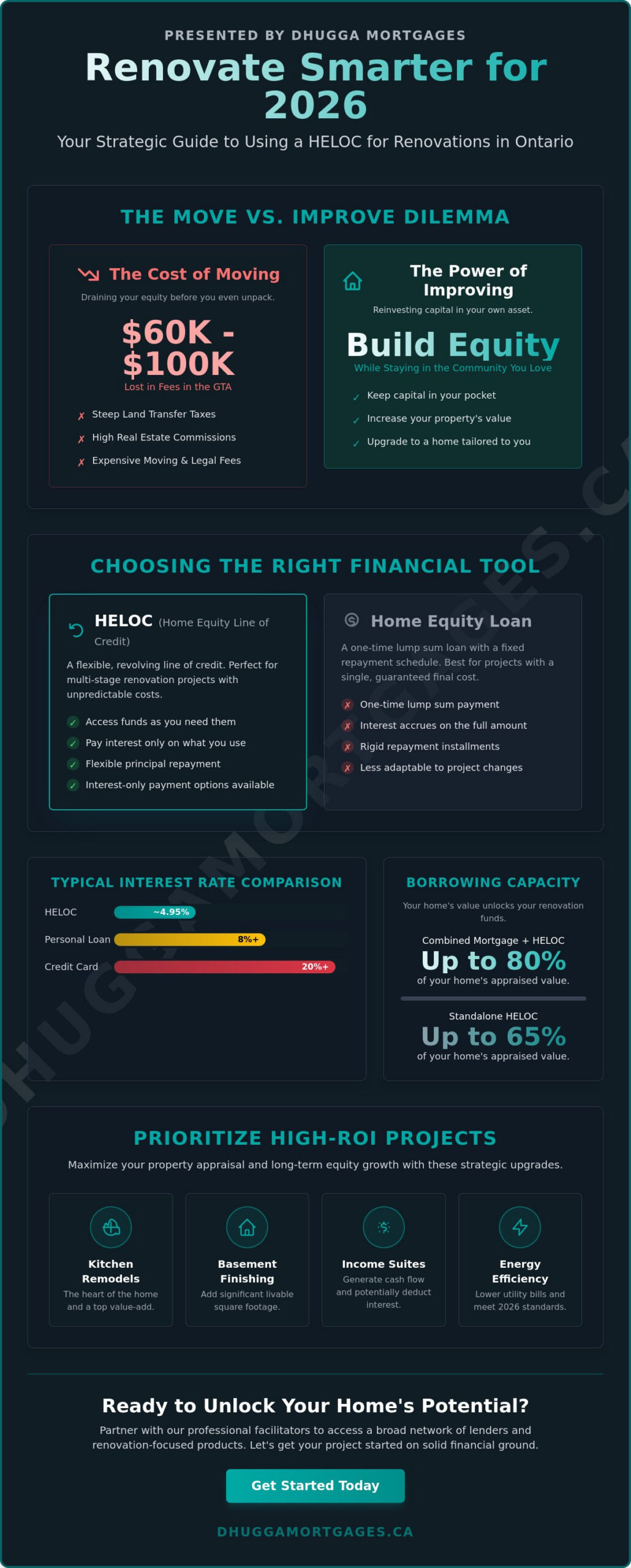

- Prioritize high-ROI projects like kitchen remodels and basement finishing. These strategic upgrades maximize your property appraisal and long-term equity growth.

- Prepare for the 2026 stress test by organizing your financial documents early. Knowing your equity limits and income requirements speeds up the path to approval.

- Partner with professional facilitators to access a broad network of lenders. Modern, renovation-focused products offer the competitive edge you need for large-scale home improvements.

What is a HELOC and how does it work for Ontario renovations?

A Home Equity Line of Credit (HELOC) is a revolving loan secured by your property. Think of it as a flexible credit limit that lives within your home’s value. You can find a technical breakdown of What is a HELOC through standard resources, but for a renovation, it functions like a high-limit, low-interest credit card. You don’t take the money all at once. You access it as needed. using HELOC for renovations Ontario allows you to tap into your equity without the rigid structure of a traditional loan. It’s about control and speed.

Borrowing for a multi-stage project requires a tool that matches the workflow. You withdraw funds to pay the plumber today. You wait three weeks for the flooring to arrive. Then, you withdraw more to pay the installer. You only pay interest on the funds you actually use. This is a massive advantage over lump-sum loans where interest accumulates on the full amount from day one. If you have a $100,000 limit but only use $20,000 for a kitchen refresh, you only carry the cost of that $20,000. Principal repayment is equally flexible. Pay it down whenever you have extra cash. There are no harsh penalties for being proactive with your debt.

HELOC vs. Home Equity Loan: Which fits your project?

Standard home equity loans provide a one-time lump sum with fixed installments. This works if your contractor provides a guaranteed, all-in quote that won’t budge. However, the 2026 construction landscape in Ontario is defined by unpredictable material costs and labour shifts. HELOCs are superior for this environment. They offer revolving access that adapts to your project’s changing needs. You can choose interest-only payment options during the construction phase. This keeps your monthly overhead low while your house is a construction zone. Standard amortized installments can strain your cash flow when you’re already dealing with renovation stress.

Ontario LTV limits and borrowing capacity

Lending regulations in Ontario are specific about how much you can access. Federally regulated lenders cap the standalone HELOC portion at 65% of your home’s appraised value. If you want to maximize your borrowing power, your combined mortgage and HELOC limits can reach up to 80% of the total value. Equity is the difference between your home’s current market value and your remaining mortgage balance. If your Toronto home is valued at $1.1 million and your mortgage is $600,000, you have significant room to grow. using HELOC for renovations Ontario is the most efficient way to put that dormant value to work immediately. It turns your bricks and mortar into a liquid asset for home improvement.

Why using a HELOC for renovations is a smart 2026 strategy

Moving is expensive. In Ontario, the friction costs of selling and buying can drain your equity before you even unpack a box. Between real estate commissions and the steep Land Transfer Tax, a GTA homeowner could easily lose $60,000 to $100,000 just by switching addresses. using HELOC for renovations Ontario keeps that capital in your pocket. You reinvest in your own asset rather than paying for the privilege of moving. It’s a strategic move for the 2026 market where inventory remains tight and prices in cities like Toronto average over $1.1 million.

Interest rates are the next big factor. Unsecured personal loans and credit cards are high-cost traps. With the Bank of Canada holding benchmark rates steady at 2.25%, HELOCs are currently available around 4.95%. This is significantly lower than most other forms of credit. You gain access to cheap capital secured by your home’s value. Following Canadian government guidelines on HELOCs helps you manage this debt responsibly while maximizing your home’s potential. It’s about using the right tool for the job.

Modernization is no longer optional. Homes must meet 2026 energy efficiency standards to maintain their value. Upgrading to heat pumps or high-performance insulation lowers your monthly utility bills immediately. There is also a tax advantage to consider. If your renovation includes an income-generating suite, the interest on your HELOC might be tax-deductible. This turns a renovation project into a legitimate investment vehicle. You build equity while creating a new stream of monthly cash flow.

The ‘Move vs. Improve’ dilemma in the GTA

Staying in your established Brampton or Mississauga neighbourhood has its perks. You know the schools. You have the shortest commute. A HELOC allows you to customize your home to fit your family’s changing needs without the stress of a bidding war. Why compete for a new house when you can build your dream kitchen exactly where you are? You realize the full potential of your property while avoiding the uncertainty of the current housing market. It is the fastest path to the home you actually want.

Flexible funding for unpredictable contractor timelines

Renovations rarely follow a perfect schedule. Permits get stuck at City Hall. Materials get backordered. The “draw” system of a HELOC is designed for this reality. You only withdraw funds when a milestone is reached. This prevents you from paying interest on a massive lump sum while you wait for a plumber to show up. You also maintain a vital cash reserve. Having immediate access to credit ensures you can handle those inevitable “behind the drywall” surprises without halting production. If you want to explore your borrowing power, reach out to a professional to review your equity options.

High-ROI renovations: Where to spend your equity in Ontario

Not all renovations are created equal. In the cooling 2026 Ontario market, buyers are more discerning. They value efficiency and functionality over pure aesthetics. using HELOC for renovations Ontario allows you to target high-impact areas without draining your cash reserves. You need to focus on upgrades that move the needle during a property appraisal. This means prioritizing structural integrity, energy performance, and usable square footage. Speed and precision in your spending will define your project’s success.

Energy-efficient upgrades are the new gold standard for ROI. With the Home Renovation Savings Program (HRSP) offering up to $10,000 for electrically heated homes, the incentive to modernize is massive. Buyers in 2026 look for heat pumps and high-performance insulation to offset rising utility costs. Smart home integrations also attract tech-savvy GTA buyers. Automated lighting, climate control, and security systems are no longer luxury add-ons. They are expected. The Financial Consumer Agency of Canada explains a HELOC as a revolving credit source, making it the perfect tool to fund these phased, high-tech installations as your budget allows.

Legal basement suites and rental potential

Secondary suites are the ultimate “mortgage helper” in high-demand cities like Toronto and Brampton. Demand for rental housing remains at record highs. A legal basement apartment can pay for its own financing while significantly boosting your home’s market value. Finishing a basement in Toronto typically costs between $55 and $75 per square foot. For an average-sized basement, this translates to an investment of $35,000 to $70,000. You must navigate Ontario’s building codes and municipal bylaws to ensure the unit is legal. A non-compliant suite won’t offer the same appraisal boost or legal protection.

Kitchens and bathrooms: The classic value-add

Kitchens and bathrooms remain the top influencers for property value. A basic kitchen renovation in Toronto starts between $15,000 and $25,000. For mid-range projects, expect to spend up to $50,000. Smart spending here focuses on functional layout improvements rather than just high-end finishes. Open-concept designs and increased storage provide better long-term value than trendy tiles. Bathroom upgrades follow a similar logic. A standard refresh costs between $8,000 and $15,000. These rooms are the “heart of the home.” Modernizing them ensures your property stays competitive in a crowded Mississauga or Caledon listing environment.

Step-by-step: How to secure your HELOC for renovations

Securing your funding starts with a clear understanding of your numbers. First, determine your current home equity through a professional market analysis. Since equity is the difference between your home’s market value and your mortgage balance, an accurate valuation is critical. Next, organize your financial paper trail. Lenders in 2026 require up to date proof of income, recent T4s, and your current mortgage statements. Having these ready speeds up the approval process significantly. using HELOC for renovations Ontario is most effective when you have a finalized renovation budget. Know your costs before you apply so you can request the correct credit limit.

Consulting with an expert broker is your biggest advantage. A broker compares HELOC products across multiple Ontario lenders to find the best fit for your specific project. Once you select a lender, you will complete the application and a formal appraisal process. This appraisal confirms the 65% LTV limit for the revolving portion of your credit. After approval, your revolving credit line is unlocked. You gain the freedom to draw funds as your contractors hit their milestones. It is a high-velocity path to starting your project.

Qualifying in 2026: What Ontario lenders look for

The “Stress Test” is the primary gatekeeper for your credit limit. To qualify in 2026, you must prove you can handle payments at your contract rate plus 2 per cent, or a floor rate of approximately 5.25 per cent. Lenders also scrutinize your Debt-to-Income (DTI) ratio more than ever. A credit score in the high 700s ensures you access the most competitive rates, currently starting around Prime + 0.50 per cent. Different lenders have varying appetites for renovation-specific products. Some may be more flexible if the project significantly increases the home’s value.

Managing your renovation budget through your HELOC

Discipline is essential once the funds are available. Set up a separate account to track every renovation-related transaction. This makes it easier to monitor interest costs and simplifies tax time if you are building an income-generating suite. Use electronic alerts to keep a close eye on your credit limit throughout the construction phases. Create a repayment plan that goes beyond interest-only payments. While the flexibility is helpful, paying down the principal early saves you thousands in the long run. If you are ready to see what you qualify for, secure your renovation financing now.

- Obtain a professional appraisal to confirm your borrowing capacity.

- Gather T4s and mortgage statements to prove financial stability.

- Work with a broker to access a wider range of Ontario lenders.

- Finalize your contractor quotes to set an accurate credit limit.

The Dhugga Advantage: Fast, professional HELOC solutions

Dhugga Mortgages delivers results. We specialize in high-velocity approvals for Ontario homeowners. You don’t have time to wait for big bank bureaucracy when your contractor is ready to start. using HELOC for renovations Ontario should be a fast, streamlined process. We offer access to a broad network of lenders. This includes niche providers with flexible, renovation-focused products. We know the local market from Brampton to Toronto. Our team provides proactive guidance at every step.

Unlocking equity requires a strategic approach. Sometimes, a standalone line of credit is the perfect fit. In other cases, we simplify the complexity of mortgage refinancing Ontario to maximize your borrowing power. We analyze your current debt structure and your renovation goals. We find the path that puts the most capital in your hands. It’s about efficiency. It’s about the edge you gain with expert advice.

Why choose a broker over a big bank?

Big banks have rigid rules. They often miss the nuance of your specific situation. We provide personalized service that realizes your unique financial goals. If you are a self-employed homeowner, you know the frustration of traditional lending. We access niche lenders that offer better terms for entrepreneurs and those with non-traditional income. We compare multiple products simultaneously. This ensures you gain a competitive advantage. You get the best terms without the legwork.

Start your renovation journey today

Don’t let your project stall. Get the funding you need with total confidence. Our results-oriented team is ready to take charge now. We streamline your application to move at the speed of your renovation. We are high-energy partners in your success. For older homeowners looking to stay in their homes, we explore every avenue. A reverse mortgage Canada could be the strategic tool you need for a retirement-friendly upgrade. using HELOC for renovations Ontario is just one way we help you build a better home. Contact us now to unlock your home’s potential.

Take Control of Your Home’s Value Today

Your property is your most powerful financial asset. using HELOC for renovations Ontario is the smartest way to upgrade your lifestyle without the friction of a high-cost move. You now understand how to target high-ROI projects like legal basement suites and energy-efficient kitchens. You know how to navigate the 2026 stress test. Stop planning. Start building. We remove the complexity from the lending process so you can focus on your vision.

Dhugga Mortgages is your seasoned expert brokerage for Brampton and the entire GTA. We provide immediate access to over 50 Canadian lenders. Our approval process is fast-paced and results-oriented. We value your time above all else. We are the high-energy partners you need to stay ahead in a cooling market. Don’t let your equity sit idle while material costs shift. Secure your competitive edge with a team that delivers speed and reliability.

Unlock your home equity for renovations with Dhugga Mortgages today!

Your dream renovation is within reach. Let’s make it happen now.

Frequently Asked Questions

Can I use a HELOC for any type of home renovation in Ontario?

Yes, you can use a HELOC for any renovation project, from cosmetic kitchen refreshes to major structural additions. Lenders don’t typically restrict how you use the funds as long as you stay within your credit limit. This flexibility is a primary reason for using HELOC for renovations Ontario. You can fund everything from a $15,000 bathroom update to a $200,000 whole-home transformation.

How much of my home’s equity can I actually borrow for a renovation?

You can borrow up to 65% of your home’s appraised value through the revolving portion of a HELOC. If you combine this with a traditional mortgage, your total loan-to-value ratio cannot exceed 80%. For a property valued at $1.1 million, your total borrowing capacity would be $880,000. These limits are strictly regulated to ensure you maintain a 20% equity cushion in your home.

Will using a HELOC for renovations affect my current mortgage rate?

No, a standalone HELOC will not change the interest rate or terms of your existing mortgage. It acts as a separate credit facility that sits alongside your current home loan. This allows you to keep a low fixed rate on your primary mortgage while accessing equity at current market rates. It’s an efficient way to get capital without breaking your existing mortgage contract.

What happens if interest rates rise while I’m using my HELOC?

Your monthly interest payments will increase because HELOCs are variable-rate products tied to the Prime rate. With the Prime rate currently at 4.45% in May 2026, most homeowners are seeing HELOC rates around 4.95%. If the Bank of Canada raises its benchmark rate, your borrowing costs will move upward immediately. We recommend budgeting for a 2% rate increase to ensure your renovation stays affordable.

Is a HELOC better than a second mortgage for home improvements?

A HELOC is generally superior for renovations because you only pay interest on the money you actually spend. using HELOC for renovations Ontario allows you to draw funds in stages to match contractor milestones. A second mortgage provides a lump sum of cash all at once, meaning you pay interest on the full amount from day one. The revolving nature of a HELOC offers better cash flow management.

How long does it take to get approved for a HELOC in Ontario?

Approval typically takes between seven and twenty-one days depending on the lender’s current volume. The speed of the process relies on how quickly you provide income verification and when the property appraisal can be scheduled. Our team focuses on high-velocity approvals to ensure your project isn’t delayed by paperwork. Having your T4s and mortgage statements ready before you apply will save you several days.

Can I pay off my HELOC early without a penalty?

Yes, you can pay down the principal on your HELOC at any time without incurring any prepayment penalties. Unlike many fixed-rate mortgages, HELOCs are open-ended credit lines. You can make interest-only payments during the renovation and then clear the full balance as soon as you have the funds. This makes it a perfect short-term tool for homeowners who plan to pay off the debt quickly.

Do I need a professional appraisal to get a renovation HELOC?

Yes, a professional appraisal is a mandatory step for most HELOC applications in Ontario. Lenders need a certified valuation to confirm your home’s current market value and calculate your borrowing limit. This process ensures that the 65% LTV limit is based on real-time market data. An appraiser will visit your home to inspect its condition and compare it to recent sales in your neighbourhood.