Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

How to Get a HELOC in Ontario: The Complete 2026 Homeowner Guide

- Home

- How to Get a HELOC in Ontario: The Complete 2026 Homeowner Guide

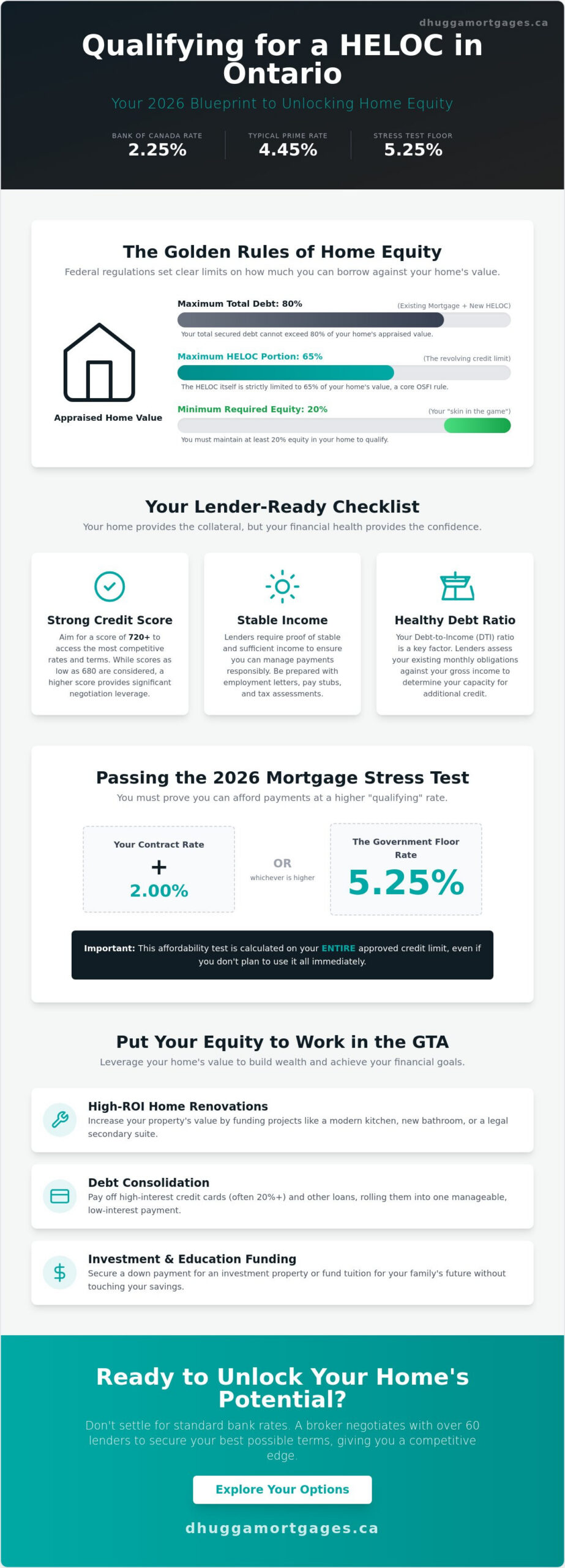

Your home is likely your biggest investment, but it’s probably just sitting there. Why pay 20% on credit cards when your walls are full of cash? In 2026, the rules have changed. Between the Bank of Canada’s 2.25% policy rate and new OSFI limits, knowing how to get a HELOC in Ontario requires a fresh strategy. You need a path that bypasses the confusion of hidden fees and the 5.25% stress test. It’s about moving fast and securing your financial edge.

We know the struggle. High rates and stringent 65% loan-to-value caps make traditional banks feel like a maze. You want flexible cash without the complexity of a second mortgage. You deserve a streamlined process that respects your time. This guide delivers the exact blueprint you need. You’ll learn how to navigate the 4.45% prime rate environment and secure the best terms in the GTA. No more waiting. No more confusion.

We are breaking down the exact qualification steps. We’ll cover credit score minimums, income verification, and the latest 2026 regulations. It is time to stop guessing and start accessing your equity. Let’s get to work.

Key Takeaways

- Master the “65% Rule” and learn why your total debt cannot exceed 80% of your home’s appraised value in 2026.

- Discover the exact steps of how to get a HELOC in Ontario by streamlining your documentation for a faster approval process.

- Compare the flexibility of interest-only payments against traditional refinancing to find the most cost-effective equity strategy.

- Leverage the advantage of a broker to negotiate lower margins across 60+ lenders and secure a competitive edge over big bank rates.

What is a HELOC and How Does it Work in Ontario?

A HELOC isn’t a traditional lump-sum loan. It’s a reusable financial tool. Think of it like a high-limit credit card, but with a much lower interest rate because it’s backed by your home. This is a Home Equity Line of Credit (HELOC). It’s revolving credit. You borrow what you need, pay it back, and then use it again. There’s no need to reapply every time you need cash. This flexibility is a game-changer for homeowners who want to stay liquid. Understanding these mechanics is the first step in learning how to get a HELOC in Ontario effectively.

The “interest-only” payment model is a major draw for Ontario borrowers in 2026. You aren’t forced to pay down the principal every month. You only pay interest on the exact amount you’ve withdrawn. If you haven’t touched the money, you don’t owe a cent. This allows you to manage your monthly cash flow with precision. In an environment where the Bank of Canada policy rate sits at 2.25%, keeping your monthly obligations low is a strategic move. You keep control of your capital. You decide when to pay down the balance.

Security is the engine behind the low rates. Your home acts as collateral. This reduces the lender’s risk significantly compared to an unsecured personal loan or a credit card. Because the risk is lower, the savings are passed to you. It’s a professional way to leverage your hard-earned equity. You’ve spent years paying down your mortgage. Now, it’s time to make that equity work for you. Stop letting your wealth sit idle in your walls.

Standalone HELOC vs. Combined Mortgage Products

You have two primary options. A standalone HELOC is designed for homeowners who’ve already paid off their mortgage entirely. It’s a clean, senior line of credit. The second option is the re-advanceable mortgage, often called a combined plan. As you pay down your mortgage principal, your available credit limit in the HELOC portion automatically grows. This is the standard choice for residents in Brampton and Mississauga. It ensures you always have access to a growing pool of emergency or investment capital without needing to ask for permission again. It’s about maintaining a constant financial edge.

Common Uses for Home Equity in the GTA

How are savvy homeowners in the GTA using their equity right now? Many prioritize high-ROI home renovations. In the Toronto market, adding a legal secondary suite or a modern kitchen can drastically increase your property value. Others focus on debt consolidation. They roll high-interest credit card debt into one manageable payment. This is a fast way to improve your credit score while saving thousands in interest. You can also fund tuition for family members or secure a down payment for a second investment property. The goal is simple: use your equity to build more wealth. Knowing how to get a HELOC in Ontario gives you the keys to these opportunities.

Qualifying for a HELOC: Ontario Requirements in 2026

Securing a line of credit requires more than just owning a home. You need enough “skin in the game” to satisfy federal regulations. In Ontario, you must have at least 20% equity in your property. This means your combined mortgage balance and your new credit line cannot exceed 80% of the home’s appraised value. However, there is a specific nuance you must understand. While the total debt cap is 80%, the revolving HELOC portion itself is strictly limited to 65% of the home’s value. This “65% Rule” is a core part of the Financial Consumer Agency of Canada guidelines. It ensures homeowners maintain a safety net even if market prices fluctuate.

Your house provides the collateral, but your financial health provides the confidence. Lenders in 2026 prioritize a stable income and a healthy debt-to-income ratio. To secure the most competitive rates, aim for a credit score of 720 or higher. While some institutions consider scores as low as 680, a higher score gives you more leverage during negotiations. Lenders want to see that your monthly obligations don’t overwhelm your gross income. It’s about proving you can manage a revolving balance responsibly. If you want to know how to get a HELOC in Ontario with the best possible terms, your credit profile is your strongest asset.

The Stress Test and Your Borrowing Power

The Canadian mortgage stress test applies to HELOCs just like it does to standard mortgages. You must prove you can afford payments at a qualifying rate. This is usually your contract rate plus 2%, or a floor rate of 5.25%, whichever is higher. Even if you only plan to use a fraction of your limit, the bank calculates your eligibility based on the full amount being drawn. To pass this test easily, minimize your other monthly debts. Pay off small car loans or high-interest retail cards before you apply. This improves your debt service ratios and boosts your total borrowing power. If you are unsure about your numbers, reach out to us for a quick assessment of your current standing.

Documentation Checklist for Ontario Homeowners

Speed is a priority at Dhugga Mortgages. We move faster when your paperwork is ready. To learn how to get a HELOC in Ontario without the usual bank delays, gather these items first:

- Proof of Income: Your most recent pay stubs and the last two years of your T4s and Notices of Assessment (NOAs).

- Mortgage Details: Your current mortgage statement showing your remaining balance and term.

- Property Proof: Your most recent property tax bill and proof of home insurance.

For self-employed individuals in the GTA, requirements are more specific. You’ll need your T1 Generals and business financial statements for the last two years. Having these documents organized allows us to skip the back-and-forth and get your approval finalized immediately. We value your time and focus on a proactive, streamlined experience.

HELOC vs. Refinancing: Choosing the Right Equity Strategy

Deciding between a credit line and a full mortgage refinance is a strategic choice. It isn’t just about the lowest rate. It’s about how you plan to use the money. A HELOC is a “pay-as-you-go” model. Refinancing is a “lump-sum” injection. Both options involve setup costs. You’ll likely pay for a professional appraisal and legal fees to register the charge on your property title. However, the biggest cost often isn’t the setup. It’s the penalty. If you break a fixed-rate mortgage early to refinance, you could face massive prepayment charges. A HELOC avoids this entirely. It sits behind your existing mortgage. You keep your current low rate and add the flexible line on top. This is a vital factor when researching how to get a HELOC in Ontario without wasting capital on bank fees.

Interest rate structures also differ significantly. HELOCs are almost always variable. They move with the lender’s prime rate, which sits at 4.45% in May 2026. Refinancing allows you to lock in a fixed rate for the entire amount. This provides predictable monthly payments for years. For a neutral breakdown of these products, consult the Financial Consumer Agency of Canada’s guide to borrowing against home equity. At Dhugga Mortgages, we help you weigh these costs against your long-term goals. We don’t just provide a product; we provide a plan that protects your wealth.

When a HELOC is the Superior Choice

A HELOC wins if your project has a moving target. Think of a phased home renovation where costs fluctuate over several months. You only pay interest on what you’ve actually spent. It’s also the perfect emergency fund. It costs you nothing to keep the balance at zero, but the money is there the moment you need it. If you currently hold a first mortgage with a rate significantly lower than 2026 market averages, a HELOC is your best bet. It lets you access cash without touching your primary low-interest debt. Knowing how to get a HELOC in Ontario ensures you don’t sacrifice a great existing rate for a little extra liquidity.

When Refinancing Makes More Sense

Refinancing is better for predictable, one-time expenses. If you need a large, specific amount of cash upfront, a fixed-rate refinance offers total peace of mind. It is also the right move if you want to extend your amortization. This can lower your total monthly obligations by spreading the debt over a longer period. If this sounds like your situation, check out our mortgage refinancing Ontario guide. We explain exactly how to restructure your debt for maximum monthly cash flow. Sometimes a full refinance is the smarter play for your long-term financial health.

Step-by-Step: How to Get a HELOC in Ontario

Unlocking your equity is a methodical process. It requires speed and precision. Follow these five steps to master how to get a HELOC in Ontario without the typical bank runaround. First, consult with a broker. We analyze your current mortgage and property value to realize your maximum borrowing potential. Second, complete the application. You’ve already gathered your NOAs and pay stubs from our earlier checklist. Now, we submit them for a proactive review. Third, undergo a professional property appraisal. This is the pivot point. It confirms your home’s current market value in the 2026 climate. Fourth, the lender reviews the file. They issue a conditional approval for your credit limit based on your debt-to-income ratios. Finally, you meet with a lawyer. They register the charge on your title and you sign the final documents. You’re ready to access your cash.

The Appraisal Process in the GTA

The GTA market is unique. Appraisals in Brampton, Mississauga, or Toronto move faster and often involve higher valuations than rural Ontario. Local appraisers look at recent comparable sales within a very tight radius. To ensure the highest valuation, prepare your home like you’re selling it. Clean the gutters. Touch up the paint. Ensure all systems are functional. Don’t overlook the exterior. Curb appeal matters to appraisers just as much as it does to buyers. A well-maintained lawn and a clean entryway suggest the home has been cared for. This can influence the final number in your favour. At Dhugga Mortgages, we work with a network of approved local appraisers. They understand the nuances of Caledon, Mississauga, and downtown Toronto. They know the true worth of your neighbourhood.

Closing Costs and Hidden Fees

Expect some one-time setup costs. These typically include appraisal fees, legal fees, and title search fees. Legal processing isn’t just about signing papers. Your lawyer must perform a title search to ensure no existing liens interfere with the new credit line. They then register the HELOC as a charge against your property. While these are out-of-pocket expenses, they are a strategic investment. You’re paying once for years of flexible, low-interest credit access. The entire timeline from your first call to funds being available usually takes two to four weeks. We push for the faster end of that range. If you’re ready to start the clock, book your consultation today. We’ll handle the heavy lifting while you focus on your financial goals.

The Dhugga Advantage: Why Use a Broker for Your Ontario HELOC?

Learning how to get a HELOC in Ontario is only half the battle. Securing the right margin is where the real work begins. Big banks are rigid. They have one set of rules and one specific product. If you don’t fit their narrow criteria, they say no. That isn’t how we operate at Dhugga Mortgages. We’re proactive. We take charge of the process. We negotiate with a network of over 60 lenders across Canada. This includes major banks, credit unions, and alternative lenders that you can’t access on your own. We don’t just find you a rate; we find you an edge. Our goal is to secure a lower margin over the 4.45% prime rate, saving you thousands over the life of your credit line.

Speed is our standard. While big banks can take weeks to move a file through their bureaucracy, we focus on immediate action. We understand the local markets in Brampton, Mississauga, and Caledon because we live and work here. We know how property values are shifting in 2026. This local expertise allows us to package your application in a way that lenders trust. We aren’t just a service provider. We’re your long-term partner. We look at your total financial health to ensure your equity strategy builds real wealth. We handle the complex paperwork and the lender negotiations so you can stay focused on your goals.

Beyond the Big Banks

Bank loan officers are employees of the bank. Their loyalty is to the institution, not to you. They can only offer you the rigid products sitting on their shelf. If you’re self-employed or have a non-traditional income, a standard bank often won’t even look at your file. We specialize in these complex cases. We know which lenders have the appetite for unique financial profiles in the GTA. We cut through the red tape. We find the solutions that others miss. Having a seasoned expert handle your documentation ensures your application is professional and bulletproof from day one. It’s about removing complexity and delivering results.

Ready to Unlock Your Home Equity?

You’ve done the research. You know the requirements. Now, it’s time to act. When you’re ready to figure out how to get a HELOC in Ontario with the best possible terms, don’t settle for the first offer from your branch manager. Take advantage of the current 2026 market rates while they’re stable. We offer a free, no-obligation consultation to map out your borrowing potential. It’s fast. It’s easy. It’s the smartest move you can make for your financial future. Contact Dhugga Mortgages to start your HELOC application today! Let’s get your equity working for you right now.

Take Command of Your Home Equity Today

Your home equity is a powerful strategic asset. Navigating the 2026 regulations like the 65% loan-to-value cap and the 5.25% stress test requires a professional plan. You now have the blueprint for how to get a HELOC in Ontario with total confidence. Whether you’re consolidating high-interest debt or funding a major GTA renovation, the right credit structure is essential for your financial health. Speed and precision are the keys to unlocking your property’s true potential.

Don’t leave your wealth to chance. We provide access to 60+ lenders and serve as your dedicated GTA local market experts. Our 98% approval rate history shows that we deliver results where traditional banks often fall short. We remove the friction. We handle the paperwork. We secure the competitive edge you deserve. It’s time to stop waiting and start acting on your goals. Your equity is ready when you are.

Realize your equity potential-Book your free HELOC consultation now!

Frequently Asked Questions

What is the current HELOC interest rate in Ontario for 2026?

Most major lenders offer HELOC rates starting at Prime plus a small margin, currently resulting in rates between 4.95% and 5.95% as of May 2026. Your specific rate depends on your credit profile and the total equity you hold. Because these are variable rates, your monthly interest costs will fluctuate whenever the Bank of Canada adjusts its policy rate from the current 2.25% level.

Can I get a HELOC if I have a second mortgage or a private loan?

Yes, but it is more complex because the HELOC lender usually requires a high-priority position on your property title. If you already have a second mortgage or a private loan, you might need to consolidate those debts into a new product. We specialize in these scenarios. We can help you restructure your debt to find a more cost-effective solution that fits your long-term goals.

How much equity do I need to qualify for a HELOC in Brampton?

You need a minimum of 20% equity in your home to qualify for a credit line in the GTA. This means your total debt, including your existing mortgage and the new credit line, cannot exceed 80% of your home’s current market value. In high-value markets like Brampton, a professional appraisal is essential to confirm exactly how much equity you can leverage under the latest 2026 OSFI rules.

Do I have to pay off my entire mortgage before getting a HELOC?

No, you do not need to pay off your mortgage to access a line of credit. Most Ontario homeowners use a re-advanceable mortgage. This combines a standard mortgage with a HELOC. As you pay down your principal balance each month, your available credit limit automatically increases. This provides ongoing access to cash without needing to refinance your entire property or break your current mortgage term.

Are HELOC interest payments tax-deductible in Canada?

Interest is only tax-deductible if the borrowed funds are used to earn investment income, such as purchasing a rental property or stocks. If you use the money for personal expenses like home renovations or debt consolidation, the interest is not deductible. You should consult with a Canadian tax professional to ensure you are following the latest CRA guidelines for your specific investment strategy.

What happens to my HELOC if the value of my Ontario home drops?

Lenders have the right to reduce your credit limit if a new appraisal shows a significant drop in your home’s market value. While this is rare in stable GTA neighbourhoods, it is a risk of using a house-backed product. If your limit is lowered, you won’t be forced to pay it back immediately. However, you may lose access to any undrawn funds until the market recovers and your equity increases.

How long does it take to get approved for a HELOC with a broker?

You can typically expect a full approval within two to four weeks when working with a proactive broker. This timeline includes the initial application, the professional property appraisal, and the legal registration of the charge on your title. Having your documentation ready is the fastest way to learn how to get a HELOC in Ontario and secure your funds without unnecessary bank delays.

Can I use a HELOC to buy a second investment property in the GTA?

Yes, using home equity for a down payment on an investment property is a common strategy for building wealth in Ontario. However, new 2026 OSFI rules prevent you from using the same income to qualify for multiple properties. Each property must now meet its own debt-service ratio requirements. We can help you navigate these stricter lending guidelines to ensure your investment plan remains viable and profitable.