Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Bad Credit Debt Consolidation Mortgage: Myth-Busting Your Way to Financial Freedom

- Home

- Bad Credit Debt Consolidation Mortgage: Myth-Busting Your Way to Financial Freedom

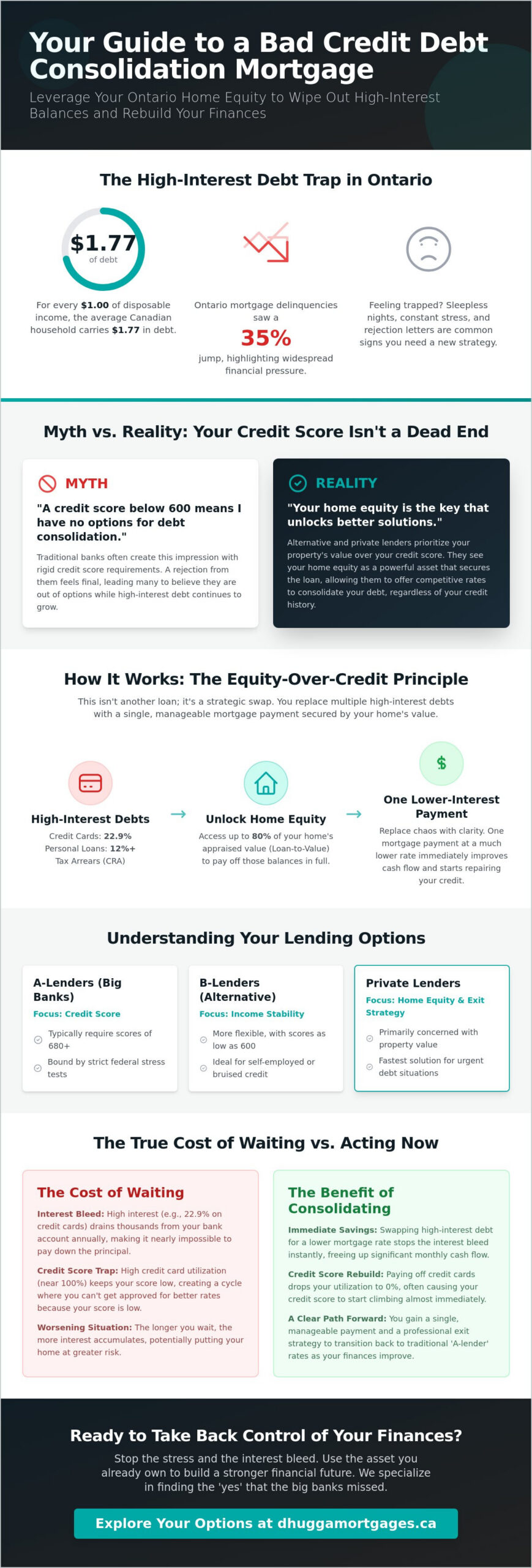

Did you know that for every dollar of disposable income in Canada, the average household now carries C$1.77 in debt? In Ontario, where mortgage delinquencies jumped 35% in late 2025, many are turning to a bad credit debt consolidation mortgage to find relief. You’ve likely felt that pressure. Sleepless nights. Constant stress. The stack of rejection letters from big banks suggests you’re out of options. You’re worried about losing your home while high-interest debt bleeds your bank account dry every month.

It’s time to stop the cycle. You don’t need a perfect credit score to take back control. We help you leverage your Ontario home equity to wipe out high-interest balances once and for all. This is about finding a proactive path forward even when traditional lenders say no. Your home is your greatest asset. Make it work for you. Fast results. No more complexity.

We’re going to bust the myths surrounding alternative lending and show you how to stop the interest bleed immediately. You’ll discover a clear strategy to secure one manageable monthly payment. Learn how to stop the fear and start a proven path to rebuilding your credit score today. Let’s get your financial freedom back on track.

Key Takeaways

- Realize that a credit score below 600 isn’t a dead end for a bad credit debt consolidation mortgage when you have home equity.

- Shift your focus from credit scores to equity to unlock more competitive rates from B-lenders and private sources.

- Compare the high cost of 22.9% credit card interest to much lower mortgage rates to stop the monthly interest bleed immediately.

- Follow a five-step plan to total your debts and get an accurate valuation of your Ontario property.

- Establish a professional exit strategy to transition back to traditional bank rates as your financial health improves.

Myth vs. Reality: Can You Get a Debt Consolidation Mortgage with Bad Credit?

A bad credit debt consolidation mortgage isn’t just another loan. It’s a strategic refinance designed to reset your financial clock. Many Ontario homeowners believe that if their credit score drops below 600, their chances of debt relief disappear. That is simply a myth. While traditional banks operate on rigid “hard floors” for credit scores, alternative lenders in the GTA prioritize the value of your property over a number on a screen. This shift from unsecured debt to equity-backed consolidation is the key to breaking free from high-interest cycles. To understand the basics, you might ask, what is debt consolidation? At its core, it’s about combining multiple high-interest liabilities into a single, lower-interest mortgage payment that is secured by your home.

The ‘Bank Says No’ Myth

Big banks are built for “A-lender” clients with pristine credit histories. When they send a rejection letter, it isn’t a judgment of your financial worth. It’s a sign of a product mismatch. Banks prioritize credit scores because they are risk-averse and bound by strict federal stress tests. In the Brampton and Toronto markets, private and alternative lenders see things differently. They focus on your home equity. If you have enough equity in your property, you have options. Rejection from a bank is often just the beginning of a more flexible path through alternative lending. We specialize in finding the “yes” that the big banks missed.

Understanding the Credit Score Barrier

In Canada, Equifax and TransUnion calculate your score based on several factors. Credit utilization is a heavy hitter. Many people have “bad credit” simply because their credit cards are maxed out. This creates a trap. You can’t lower your utilization because the interest is too high, and your score stays low because utilization is high. A bad credit debt consolidation mortgage fixes this instantly. By paying off those cards with your home equity, your utilization drops from near 100% down to zero. Your score often begins to climb almost immediately. It’s a proactive way to fix your credit while saving thousands on interest payments. You stop being a victim of the credit score system and start using your home to repair it.

- A-Lenders: Focus on credit scores (typically 680+).

- B-Lenders: Focus on income stability and scores as low as 600.

- Private Lenders: Focus almost entirely on home equity and your exit strategy.

You don’t need to wait for your score to improve before you seek help. In fact, waiting often makes the situation worse as interest accumulates. Use the equity you’ve built in your home to clear the slate today. It’s a faster, more efficient way to reach financial freedom.

How Bad Credit Debt Consolidation Mortgages Actually Work

A bad credit debt consolidation mortgage works by turning your home’s value into liquid cash. It isn’t a complex mystery. It’s a simple swap. You take the high-interest debt that’s crushing your monthly cash flow and roll it into a new or second mortgage. While your credit card might charge 22.9%, a mortgage-based solution typically sits much lower. This process relies on the “Equity over Credit” principle. Alternative lenders care less about your past mistakes and more about the security of your property. They look at the asset first and the person second.

In Ontario, homeowners can generally access up to 80% of their home’s appraised value through mortgage refinancing. This is known as the Loan-to-Value (LTV) ratio. If your home is worth C$800,000, an 80% LTV allows for a total mortgage of C$640,000. If your existing mortgage is C$500,000, you have C$140,000 available to wipe out other debts. This includes everything from high-interest credit cards and personal loans to more serious liabilities like CRA tax debt. Following government advice on debt consolidation often highlights using home equity as a powerful way to reduce total interest costs. You can explore your specific debt consolidation possibilities to see how much equity you can unlock today.

Equity is Your Secret Weapon

Equity is the difference between what your home is worth and what you owe on it. With the average Ontario home price reaching C$811,868 in March 2026, many residents are sitting on a goldmine without realizing it. Lenders view your home as a tangible safety net. Even if your credit score is in the 500s, the property itself provides the security needed to approve the deal. It’s a strategic move. You use the asset you’ve worked hard for to solve the debt problems that are holding you back. It’s about leveraging your house to save your future.

The Role of Private Lenders in Ontario

Private lenders are the fast-moving facilitators of the GTA mortgage market. In cities like Brampton and Mississauga, speed is everything. Private mortgages act as a short-term bridge, usually for one to three years. These lenders don’t get bogged down in the same red tape as big banks. They look at the property’s location and its likelihood of selling. If the equity is there, the deal moves forward. This gives you the immediate cash needed to stop the interest bleed. It’s a proactive tool for those who need to act now. Once your high-interest debts are cleared, your credit starts to recover, allowing you to eventually move back to a traditional bank.

The True Cost of Waiting vs. Consolidating Now

Every day you delay a bad credit debt consolidation mortgage, you lose money to high-interest penalties. Staying in the status quo is the most expensive financial choice you can make. Credit cards at 22.9% aren’t just debt. They’re a silent tax on your future. A mortgage-based solution might carry a rate between 9% and 12%, but that represents a massive victory for your monthly budget. It stops the interest bleed. It gives you the room to breathe that you’ve been missing. Don’t let the fear of a higher mortgage rate keep you trapped in a much worse credit card cycle.

High-Interest Debt: The GTA Wealth Killer

Consider a typical scenario for a family in Toronto or Brampton. You owe C$50,000 across multiple credit cards. If you only pay the minimums, it could take over 20 years to clear the balance. Most of your hard-earned money disappears into interest payments. By rolling that balance into a five-year mortgage plan, you could save over C$1,500 every month in cash flow. This is life-changing money. It’s the difference between struggling to buy groceries and actually building equity. The mental health impact of this pressure is real. Constant stress ruins sleep and strains family life. Reclaiming that C$1,500 monthly is the first step toward financial peace.

Calculating the Break-Even Point

Some homeowners hesitate because of setup costs. You’ll encounter appraisal fees, legal expenses, and lender fees. These are standard in the industry. The key is to look at the big picture. Calculate your interest savings over the next 12 months. Compare that to the one-time setup costs. In the Ontario market, the interest savings usually outweigh the fees within the first few months. The break-even point is the specific date when your accumulated interest savings finally eclipse the total costs of your mortgage refinance. Every month you wait after that point is money straight out of your pocket. Stop paying the banks and start paying yourself.

There is also an opportunity cost to waiting. Rebuilding a credit score takes time. If you wait another year to consolidate, you’re delaying your return to “A-lender” bank rates by that same year. Act now to start the clock on your recovery. The faster you consolidate, the faster you can move back to traditional low-rate financing. It’s a proactive move for a better future. Get the facts. Do the math. Take the lead.

5 Steps to Securing Your Consolidation Mortgage in Ontario

Securing a bad credit debt consolidation mortgage requires a different playbook than a standard bank application. You aren’t just applying for a loan; you’re presenting a business case for your financial recovery. Follow these five steps to ensure success.

- Step 1: Get a realistic home valuation. Don’t rely on online estimates. They are often inflated. Get a professional opinion to know exactly how much equity you can actually access.

- Step 2: Total every single debt. Be transparent. Include credit cards, CRA tax arrears, and even private family loans. Hidden debts always surface during the legal process.

- Step 3: Partner with a specialized broker. Avoid generalists who only deal with big banks. You need a guide who understands the B-lender and private market in the GTA.

- Step 4: Prepare your story. Lenders are human. They want to know why your credit dipped. Was it a job loss? A medical emergency? A clear explanation builds trust.

- Step 5: Execute and close accounts. Once the funds are released, use them immediately to clear your balances. Close high-interest accounts to prevent the cycle from starting again.

Preparing Your Documentation

Speed is your best friend in the mortgage process. Have your documents ready before you even call. You’ll need your most recent mortgage statement and property tax bill. Notice of Assessments (NOAs) from the CRA are critical. Lenders use these to verify you don’t have outstanding tax liabilities. Even if you are self-employed, showing a stable income source through bank statements helps secure better rates. Organization removes friction and leads to faster approvals. We take the lead on this process to ensure nothing is missed.

Navigating the Appraisal Process

The appraisal is the most important document in a bad credit debt consolidation mortgage deal. Since the lender is prioritizing equity over credit, the property value is the foundation of the entire agreement. Lenders always choose the appraiser to ensure an unbiased valuation. For homeowners in Mississauga and Brampton, simple steps can maximize your home’s value. Clean up the yard. Fix minor interior repairs. Ensure the home is tidy for the inspection. These small efforts improve “curb appeal” and can lead to a higher valuation, which means more cash available for your debt consolidation.

Ready to see how much equity you can leverage? Apply for your debt consolidation mortgage today and get a proactive plan for your financial future. We act fast so you can stop worrying and start rebuilding.

The Dhugga Advantage: Your Path to Financial Recovery

Choosing a bad credit debt consolidation mortgage is a strategic business decision. It requires more than just a lender. It requires a partner who understands the high-velocity GTA real estate market. We act as your proactive guide throughout the Brampton and Toronto corridors. Our focus isn’t just on getting you the funds today. We prioritize your exit strategy. A private or B-lender mortgage is a bridge. We ensure you have a clear, documented path to move back to an A-lender at traditional bank rates as soon as your credit recovers. This long-term vision sets us apart from passive advisors.

Local expertise matters in the Ontario market. Property values in the GTA fluctuate quickly. We stay ahead of these trends to ensure your home equity is leveraged to its full potential. We don’t just look at numbers. We look at the advantage you gain by clearing the slate. Our process is built for speed and reliability. We remove the complexity so you can focus on your future.

Custom Strategies for Brampton and Mississauga Homeowners

Brampton and Mississauga have unique property dynamics. Multi-generational home financing is a common local reality that national banks often struggle to process. We understand the true value of your neighbourhood. Our deep roots in the community allow us to present your property’s value accurately to our broad lender network. We access private capital and alternative sources that many other brokerages simply cannot reach. This local edge ensures you get the most equity possible from your home. We realize that every property has a story, and we know how to tell it to the right lenders.

Beyond the Closing: Rebuilding Your Credit

The mortgage closing is just the start of your recovery. Once your high-interest cards are cleared, your monthly cash flow improves instantly. Use that extra capital to build a robust emergency fund. This prevents you from relying on credit cards when unexpected expenses arise. As your score improves, you’ll be in a position to help others too. Many of our clients eventually use their improved financial standing to support family members. You can explore our First Time Home Buyer Mortgage Ontario guide to see how the next generation can start their journey on the right foot.

Don’t let debt define your future. We provide the speed, reliability, and local expertise you need to succeed with a bad credit debt consolidation mortgage. Contact us today for a no-obligation debt assessment. Let’s build your path to financial freedom together. The time to act is now. We are ready to take charge of your recovery.

Take Charge of Your Financial Future Today

High-interest debt doesn’t have to be a life sentence. You’ve seen how a bad credit debt consolidation mortgage leverages your home equity to stop the interest bleed. It’s about moving from stress to stability. We’re specialists in GTA private lending. We provide access to over 50 lenders, including flexible B-lenders. Whether you’re self-employed or a newcomer to Canada, we offer the expert guidance needed to navigate this process. You’ve learned the steps. You’ve seen the math. Now, it’s time to act.

Don’t let rejection letters from big banks stop you. Your home is a powerful tool for recovery. We find the “yes” that others miss. Start your journey toward one manageable payment and a better credit score now. Fast results. No more complexity. Take the lead on your recovery today. We act as your proactive partner to ensure your success.

Get your free debt consolidation assessment from Dhugga Mortgages today.

Your path to financial freedom is clear. We’re ready to help you take the first step. Let’s get started.

Frequently Asked Questions

Can I get a debt consolidation mortgage with a 500 credit score in Ontario?

Yes, you can qualify with a 500 score by working with private lenders who prioritize your home’s equity over your credit history. While big banks require scores of 680 or higher, private lenders in the GTA focus on the property’s value and your exit strategy. This makes a bad credit debt consolidation mortgage accessible even if you’ve been rejected elsewhere. We specialize in finding these equity-based solutions for Ontario homeowners.

Is it better to use a second mortgage or refinance my first for debt consolidation?

The right choice depends on your current first mortgage interest rate and potential prepayment penalties. If your first mortgage has a very low rate, a second mortgage might be cheaper than breaking the original contract. However, refinancing the first mortgage often results in a lower overall interest rate for the combined debt. We calculate the total cost of both options to ensure you get the best monthly savings.

What are the typical interest rates for bad credit mortgages in 2026?

Interest rates for bad credit first mortgages in Ontario typically range from 9% to 12% in 2026. Second mortgages often carry higher rates, generally between 11% and 15%. Private lenders may offer rates starting at 5.49% for those with better scores, but those with scores near 600 should expect rates closer to 11.5%. These rates are still significantly lower than the 22.9% typically found on credit cards.

Will my credit score go up after I consolidate my debts into a mortgage?

Yes, your credit score typically increases because you are drastically lowering your credit utilization ratio. By paying off maxed-out credit cards with a bad credit debt consolidation mortgage, you move debt from revolving accounts to an installment account. This shift is one of the fastest ways to repair a bruised credit profile in the Canadian system. Most clients see a positive impact on their score within a few months.

What happens if I’m self-employed and have bad credit?

Self-employed borrowers can still qualify by providing alternative documentation like six months of business bank statements. While banks demand perfect Notice of Assessments (NOAs), alternative lenders in Ontario are more flexible with how you prove your ability to pay. We understand the unique challenges of GTA business owners. We present your business income in the best possible light to secure a fast approval.

Are there upfront fees for bad credit debt consolidation mortgages?

You should expect standard industry fees, including lender fees of 0.5% to 2% and appraisal costs. These fees are usually deducted from the mortgage proceeds at closing rather than paid out of pocket. This means you don’t need a large cash reserve to start the process. We provide a transparent breakdown of all costs upfront so there are no surprises at the lawyer’s office.

How much equity do I need to qualify for a private debt consolidation loan?

Most lenders allow you to borrow up to 75% or 80% of your home’s appraised value. For example, if your home is worth C$800,000, you can generally access up to C$640,000 in total mortgage debt. The “equity gap” between your current mortgage and this limit is what you use to consolidate your other debts. This equity is your most powerful tool for achieving financial freedom.

Can I consolidate CRA tax debt into my mortgage?

Yes, consolidating CRA tax debt is a common and effective use for home equity. CRA debt is particularly dangerous because the government has strong collection powers, including the ability to register liens against your property. Clearing this debt through a mortgage refinance stops the aggressive interest and protects your home’s title. It’s a proactive way to resolve government liabilities quickly and move forward.