Jaspreet Dhugga – Mortgage Broker Brampton, GTA And Ontario

Reverse Mortgage vs Downsizing: Which Strategy Wins for Ontario Retirees in 2026?

- Home

- Reverse Mortgage vs Downsizing: Which Strategy Wins for Ontario Retirees in 2026?

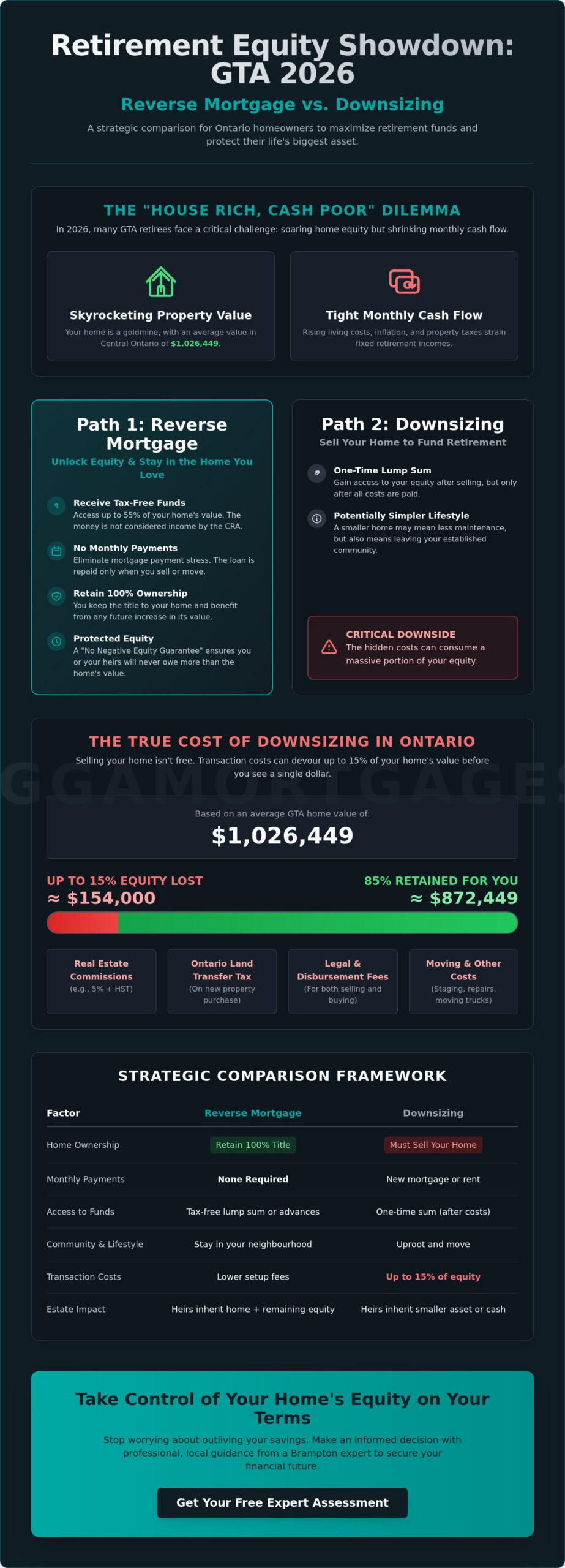

Did you know that downsizing your GTA home could swallow up to 15% of your equity in transaction costs alone? Between real estate commissions, legal fees, and Ontario land transfer taxes, the debate of reverse mortgage vs downsizing often comes down to protecting your bottom line. It’s a heavy price to pay for a lifestyle change. You’ve spent decades building a life in your community. It’s where your memories live. The thought of leaving just to fund your retirement feels like a forced choice rather than a strategic move. You deserve better options.

This guide compares the financial reality of these two paths to show you how to maximize your retirement equity in 2026. We’ll break down the hidden costs of moving and explore how a reverse mortgage keeps you in the home you love. Stop worrying about outliving your savings. Start looking at your home as the powerful asset it is. We’ll help you decide which path secures your future and protects your peace of mind. It’s time to take control of your home’s value on your own terms.

Key Takeaways

- Identify the “house rich, cash poor” reality in the GTA and why 2026 living costs demand a proactive equity strategy.

- Explore the benefits of staying in your community, including accessing tax-free funds while retaining full title to your home.

- Calculate the true impact of Ontario’s land transfer taxes and real estate commissions on your net downsizing proceeds.

- Compare a reverse mortgage vs downsizing using a strategic framework that prioritizes your long-term monthly cash flow.

- Learn how professional local guidance from a Brampton expert simplifies complex financial decisions for a faster, more reliable retirement plan.

Retiring in the GTA: The Home Equity Dilemma

Living in Brampton or Mississauga in 2026 means sitting on a goldmine you can’t easily spend. Many retirees in Peel Region find themselves “house rich and cash poor.” Your property value has likely soared over the last decade. Yet, your monthly bank balance feels thin. It’s a common frustration. You have hundreds of thousands of dollars in equity, but you’re still watching every penny at the grocery store. Traditional retirement savings often fall short of 2026 living costs. Inflation has pushed the price of everything higher, from property taxes to basic utilities. This creates a high-pressure environment for anyone on a fixed income.

The family home carries immense emotional weight. It’s where you raised your children and built your community ties. Moving isn’t just a financial transaction; it’s a major life upheaval. This is why the reverse mortgage vs downsizing debate is so critical for Ontario seniors. You have two primary paths. You can sell the asset to unlock cash and move elsewhere. Or, you can find a strategic way to tap into that wealth while staying exactly where you are. Both choices have long-term impacts on your estate and your daily comfort.

The Current GTA Real Estate Landscape

Property values in Central Ontario averaged $1,026,449 as of March 2026. While that’s a significant figure, the cost of maintaining those homes has also climbed. Inflation hits fixed-income retirees the hardest in the GTA. Some homeowners choose to wait for a better market, but “waiting it out” often costs more than you realize. Maintenance, insurance, and taxes don’t stop. These carrying costs eat into your future gains every single month. You need a proactive strategy to handle these rising expenses before they become a crisis. Staying informed about your options, including understanding What is a reverse mortgage?, is the best way to protect your financial health.

Defining Your Retirement Goals

Ask yourself what matters most for your next chapter. Do you want to stay near your local doctors, friends, and grandkids? Or are you ready for a fresh start in a smaller space? Consider your legacy. Many GTA seniors report that providing financial support to family members is impacting their own retirement. You must decide between a one-time lump sum from a sale or a steady improvement in your monthly cash flow. Your goals should drive your financing choice. Don’t let the market dictate your lifestyle. Take control of your equity to fund the retirement you actually want.

The Reverse Mortgage Advantage: Staying in the Home You Love

A reverse mortgage is a specialized loan designed for Canadian homeowners aged 55 and older. The biggest draw? You don’t make monthly mortgage payments. Instead, the loan is repaid when you move out or sell the property. This allows you to tap into your equity without the stress of a new monthly bill. Most importantly, you retain 100% ownership and title of your Ontario home. You remain the owner. You benefit from any future appreciation in the GTA market. It’s a powerful tool for those weighing the pros and cons of a reverse mortgage vs downsizing.

Current 2026 lending criteria from major providers like HomeEquity Bank remain straightforward. The property must be your primary residence. You can typically access up to 55% of your home’s appraised value, though the specific amount depends on your age. Older borrowers generally qualify for higher percentages. The funds you receive are entirely tax-free. Since the money is a loan and not income, the CRA doesn’t take a cut. This means your payments from Canadian retirement income sources like OAS or GIS remain untouched. You get the cash you need without triggering a tax bill.

How Reverse Mortgages Work in Ontario

Safety is built into the Canadian system. All major lenders provide a “No Negative Equity” guarantee. This ensures you or your heirs will never owe more than the fair market value of the home when it’s sold. You can choose how to receive your funds. Some prefer a single lump sum. Others opt for planned monthly advances to supplement their pension. Unlike traditional financing, your credit score and income matter less than your home’s appraised value. It’s about the asset, not your paycheque. This makes the process fast and accessible for retirees who might not qualify for a standard loan. If you want to see how much equity you can unlock, exploring Reverse Mortgages with a local expert is a great first step.

Addressing the Interest Rate Question

Interest rates for reverse mortgages are higher than traditional five-year fixed rates. As of May 2026, they typically sit about 2.5% higher than standard mortgages. Interest compounds over time, meaning the loan balance grows. However, this growth is often manageable. In high-demand markets like Brampton and Mississauga, consistent property value growth often offsets the cost of the interest over the long term. You aren’t paying the interest out of pocket today. You’re using your home’s future value to fund your current lifestyle. It’s a strategic trade-off that keeps you in your community while providing immediate financial relief.

The True Cost of Downsizing in Ontario: More Than Just Moving Boxes

Selling your long-term home in Brampton or Mississauga isn’t as simple as swapping a large house for a smaller condo. It’s a complex financial exit. In the GTA, the “invisible” costs of moving can consume up to 15% of your home’s total value. This is a massive factor in the reverse mortgage vs downsizing debate. You’ve worked hard for your equity. Don’t let it vanish in a single transaction. Many retirees find that a cheaper home doesn’t actually mean more money in their pocket after the dust settles. You need to look at the net proceeds, not just the sale price.

The psychological impact is equally heavy. Leaving a family residence where you’ve built decades of memories is an emotional upheaval. Beyond the feelings, there’s a practical inventory crisis. Finding a “right-sized” home in 2026 is a struggle. You’re competing with first-time buyers for limited bungalows and townhouses. This competition drives prices up. Often, you’re paying a premium for less square footage. It’s a high-stakes game. Before making a move, consult the Government of Canada guide to reverse mortgages to understand why staying put might be the smarter financial play.

The Financial Leakage of Selling

Real estate commissions in the GTA typically hover around 5%. On a C$1,026,449 property, that’s over C$51,000 plus HST. That’s equity you’ll never get back. Then comes the tax bill. If you’re buying in Toronto, you pay both the Provincial and Municipal Land Transfer Taxes. This double tax is a significant drain on your proceeds. Legal fees, professional home staging, and 2026 moving rates add thousands more. For a C$500,000 purchase in Ontario, the land transfer tax alone is C$6,475. These costs add up fast. They eat into the “nest egg” you were planning to live on.

Lifestyle Compromises and New Expenses

Moving often brings new, recurring costs. Condo fees can be unpredictable and often rise faster than inflation. You might trade a lawn to mow for a monthly fee that rivals your old maintenance budget. There’s also the “social tax.” Losing proximity to your lifelong friends, family, and trusted doctors has a real impact on your quality of life. Many seniors realize too late that their new space needs immediate work. Renovating a smaller home to suit your accessibility needs in 2026 can easily cost C$30,000 or more. You aren’t just moving boxes; you’re restructuring your entire financial and social life. Make sure the math actually works in your favour.

Reverse Mortgage vs Downsizing: A Strategic Comparison Framework

Choosing between a reverse mortgage vs downsizing requires a cold look at your balance sheet and your lifestyle. Downsizing is a permanent exit. You immediately lose 10% to 15% of your equity to GTA real estate commissions, legal fees, and Ontario land transfer taxes. A reverse mortgage has significantly lower entry costs. It prioritizes your home’s appraised value over your monthly income. This is a massive advantage in 2026. Many retirees find they can’t pass the current “stress test” for a traditional HELOC. A reverse mortgage bypasses those income hurdles entirely. It provides a fast, reliable way to access cash without a forced move.

The “Bridge Strategy” is a sophisticated move many GTA seniors now use. If the 2026 real estate market feels volatile, you don’t have to sell at a disadvantage. Use a reverse mortgage to fund your lifestyle for the next three to five years. This buys you time. You can wait for property values to climb or for interest rates to settle before making a final move. It puts you in the driver’s seat. You aren’t just reacting to the market. You’re timing your exit for maximum profit. Consider the inheritance impact too. Leaving your heirs a high-value detached home with a loan is often better than leaving a smaller condo in a less desirable area.

When a Reverse Mortgage Wins

This path is ideal if you have strong community ties. If your doctors, friends, and grandkids are nearby, staying put is priceless. It’s also the best choice for homeowners who want to “age in place” but lack the high monthly income required for standard bank loans. In many Brampton and Mississauga neighbourhoods, home appreciation continues to be strong. This growth can often offset a large portion of the compounding interest over time. You keep your asset, you keep your community, and you gain financial freedom. Ready to see how much you can unlock? Contact Dhugga Mortgages today for a professional equity review.

When Downsizing Wins

Downsizing makes sense when the physical house becomes a burden. If you can no longer manage the stairs or the C$20,000 roof replacement, it’s time to go. It’s also a winning strategy if you’re moving to a significantly lower-cost region outside the GTA. Selling a C$1.2 million home in Peel and buying a C$600,000 bungalow in a smaller Ontario town creates a massive cash cushion. This maximizes the absolute dollar value of your estate. If you’re ready for a total lifestyle reset and want to eliminate all housing debt, moving is the most direct route to that goal.

Navigating Your Retirement Financing with Dhugga Mortgages

Big banks often treat retirees like a checkbox. They focus on rigid income requirements that don’t reflect your actual wealth. At Dhugga Mortgages, we take a different approach. We’re local Brampton experts. We understand the specific nuances of the Peel Region market. Whether you’re weighing a reverse mortgage vs downsizing, you need a partner who values your time. Our process is built for speed. We remove the friction from retirement financing. You get clear answers and immediate action. It’s about realizing the full potential of your home equity without the usual bank delays. We prioritize your goals. We value your time. We deliver results.

Banks move slowly. They focus on what you don’t have. We focus on what you do. Your home is your greatest asset. We help you use it. Choosing between a reverse mortgage and moving is a major life decision. You shouldn’t make it alone. We provide the strategic edge you need to win in the 2026 GTA market. Professional. Efficient. Results-oriented. That’s the Dhugga Mortgages standard. We don’t just offer Reverse Mortgages; we offer a path to a better lifestyle. We act as your high-energy, proactive partner. We take charge of the process so you don’t have to. Our team knows every street in Peel Region. We are the bold, action-oriented guide you’ve been looking for.

Expert Guidance for Ontario Seniors

Reverse mortgage applications can be complex. We simplify them. Our team handles the heavy lifting. We have access to a broad lender network. This means we find the most competitive 2026 rates for your specific situation. Our local expertise spans Brampton, Mississauga, and Toronto. We know the local property values. We know the neighbourhood trends. This deep community knowledge ensures you get the maximum value from your equity. It’s professional guidance that puts you first. We bridge the gap between financial complexity and your peace of mind. Our approach is direct. We deliver results quickly. You deserve a streamlined experience that respects your legacy.

Take Charge of Your Future Today

Don’t wait for a financial crunch. Proactive planning is the key to a stress-free retirement. Get a clear, declarative breakdown of your potential proceeds today. We provide the facts you need to make an informed choice. No jargon. No hidden fees. Just expert advice from a trusted neighbour. Take the first step toward securing your GTA legacy. We’re ready to act immediately. Your time is valuable. We won’t waste it. Stop guessing about your financial future. Book your free equity consultation with Dhugga Mortgages today. Your future self will thank you for acting now. Let’s unlock your home’s value together. It’s time to enjoy the retirement you worked so hard to build.

Take Charge of Your GTA Retirement Today

Your home is your most powerful financial engine. It shouldn’t be a source of stress. The choice between a reverse mortgage vs downsizing comes down to control. Moving costs in Ontario can strip away up to 15% of your hard-earned equity through commissions and land transfer taxes. Staying put allows you to retain 100% ownership while accessing tax-free cash. You’ve built a life in your community. You deserve to stay there on your own terms. Don’t wait for the market to decide for you. Acting now preserves your legacy and your lifestyle.

Expert guidance is essential for a fast, reliable outcome. Jaspreet Dhugga specializes in Ontario reverse mortgages. We provide direct access to top-tier Canadian lenders. We cut through the red tape. We deliver competitive 2026 rates with total transparency. Our team is proactive and results-oriented. We value your time above all else. Secure your retirement with a personalized equity plan from Dhugga Mortgages. Let’s unlock the wealth you’ve built over decades. You’ve earned a comfortable, worry-free future in the home you love.

Frequently Asked Questions

Can I owe more than my house is worth with a reverse mortgage in Canada?

No. Canadian reverse mortgages include a No Negative Equity Guarantee. This ensures that you or your heirs will never owe more than the fair market value of the home at the time of sale. As long as you maintain the property, pay your taxes, and keep your insurance up to date, your estate is protected. This is a critical safety feature for GTA homeowners who want to stay in their community without financial risk.

What is the minimum age for a reverse mortgage in Ontario?

The minimum age for all registered homeowners is 55. The specific amount of equity you can access depends on the age of the youngest homeowner. Generally, older borrowers qualify for a higher percentage of their home’s value. In the 2026 market, an 80-year-old might access up to 55% of their equity, while a 55-year-old would qualify for a smaller portion to account for a longer loan term.

How does downsizing affect my OAS or GIS government benefits?

Downsizing can trigger a clawback of your Guaranteed Income Supplement (GIS) or Old Age Security (OAS) if you invest the proceeds from your home sale. The interest or capital gains earned on that lump sum count as income. In the reverse mortgage vs downsizing comparison, a reverse mortgage is often more tax-efficient. Since the funds from a reverse mortgage are a loan and not income, they don’t impact your government benefit eligibility.

Do I have to pay taxes on the money I get from a reverse mortgage?

No. The funds you receive from a reverse mortgage are 100% tax-free. Because the money is considered a loan and not earned income, the CRA does not take a cut. You can use the cash for any purpose, such as home renovations, medical expenses, or helping family members. It provides a way to access your wealth without moving you into a higher tax bracket or creating a new tax liability.

What happens to the reverse mortgage after I pass away or move out?

The loan becomes due when the last registered homeowner passes away or moves out of the property permanently. Your estate typically has a set window, often 180 days, to settle the balance. Most families choose to sell the home to pay off the loan and interest. Any remaining equity belongs entirely to you or your heirs. This ensures a smooth transition of assets while providing you with cash during your lifetime.

Can I still leave my home to my children if I have a reverse mortgage?

Yes. You retain full ownership and title of your home throughout the life of the loan. When the time comes to settle the estate, your children can choose to pay off the mortgage balance to keep the house or sell the property and keep the remaining equity. Because GTA property values have historically shown strong growth, many families find there is still significant equity left over for an inheritance.

How much does it cost to set up a reverse mortgage in the GTA?

Setup costs typically include a home appraisal, independent legal advice, and administrative fees. These costs ensure the property value is accurate and that you fully understand your obligations. While there are upfront expenses, they are often significantly lower than the combined cost of real estate commissions and land transfer taxes involved in a move. Many homeowners choose to pay these fees directly from the loan proceeds to avoid out-of-pocket costs.

Is it better to get a HELOC or a reverse mortgage for retirement income?

It depends on your monthly cash flow and credit profile. A HELOC requires you to make monthly interest payments and pass a rigorous income “stress test.” If your income is fixed, qualifying can be difficult. A reverse mortgage requires no monthly payments and focuses on your home’s value rather than your credit score. For many retirees, the reverse mortgage provides more immediate financial relief and better protection against rising interest rates.